Cashing a payroll check without identification can be challenging, as most financial institutions require some form of ID to verify the account holder's identity. This is primarily to prevent fraud and ensure the security of the account. However, there may be certain circumstances or alternative methods available for cashing a check without traditional ID. For instance, some banks might accept alternative forms of identification or offer services that allow for check cashing without an account. Additionally, there are check cashing stores and online services that may provide options for cashing checks with minimal identification requirements. It's important to explore these options carefully and understand any associated fees or risks before proceeding.

| Characteristics | Values |

|---|---|

| Question | Can I cash a payroll check without ID? |

| Context | Financial transaction, banking, identification requirements |

| Key Terms | Payroll check, cashing, ID, identification, bank policies |

| Possible Answers | Yes, no, depends on bank policies, alternative methods available |

| Considerations | Legal requirements, bank regulations, fraud prevention, customer service |

| Alternatives | Direct deposit, electronic transfer, mobile banking, ATM deposit |

| Additional Info | Some banks may cash checks without ID for existing customers, varies by location and institution |

Explore related products

What You'll Learn

- Requirements for Cashing: Understand the necessary documentation and identification needed to cash a payroll check

- Alternative Options: Explore methods to cash a check without traditional ID, such as using a bank account

- Legal Considerations: Learn about the legal implications and regulations surrounding check cashing without identification

- Bank Policies: Discover the specific policies of different banks regarding check cashing for individuals without ID

- Safety Measures: Find out about the security measures in place to prevent fraudulent check cashing without proper identification

![]()

Requirements for Cashing: Understand the necessary documentation and identification needed to cash a payroll check

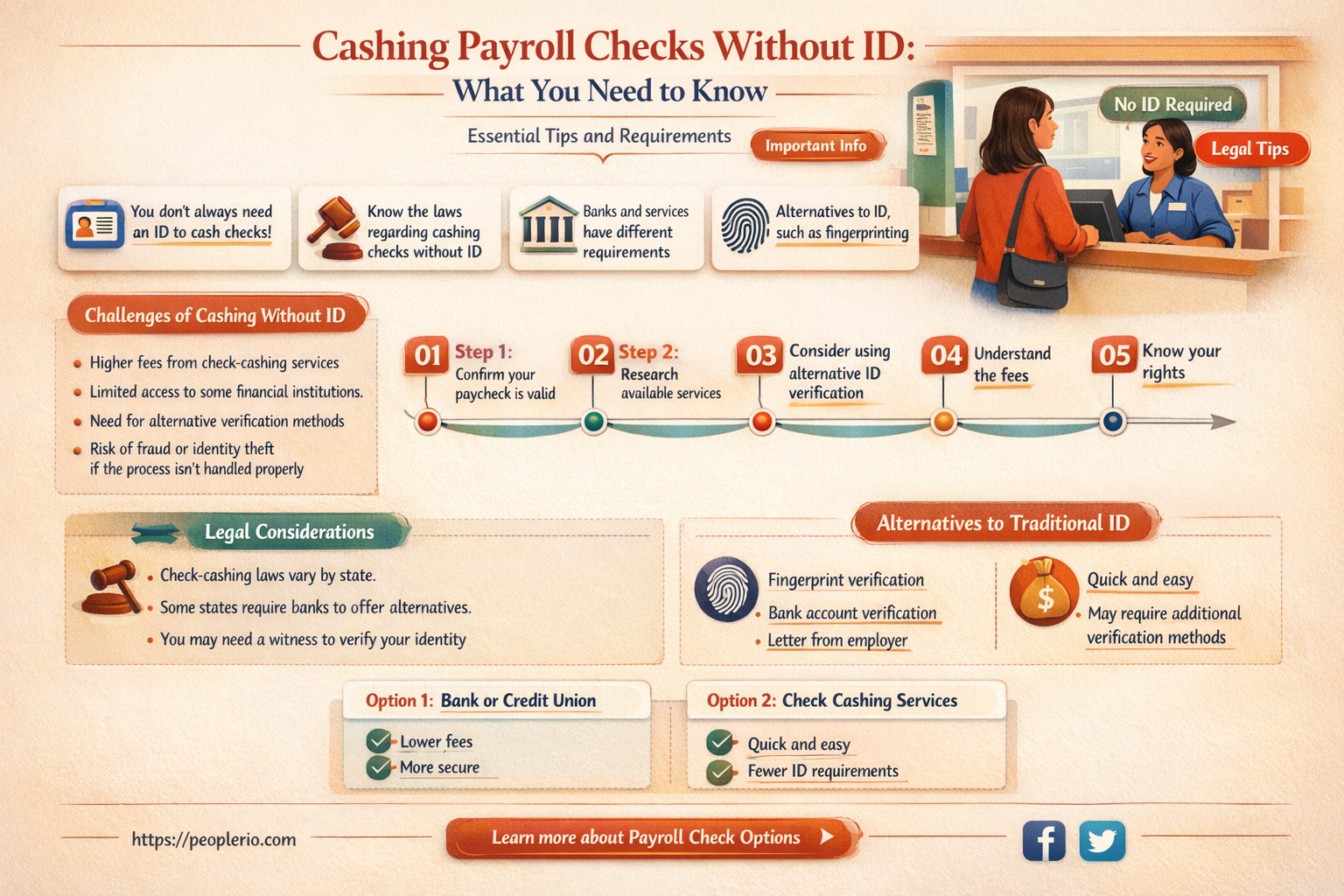

To cash a payroll check, you typically need to provide certain documentation and identification to verify your identity and ensure the check is legitimate. This process is in place to prevent fraud and protect both the issuer and the recipient of the check.

The most common form of identification required to cash a payroll check is a government-issued ID, such as a driver's license, state ID, or passport. This ID must be current and valid, with a clear photo that matches your appearance. Some financial institutions may also accept other forms of identification, such as a military ID or a tribal ID, but it's best to check with the specific bank or check cashing service to confirm their requirements.

In addition to identification, you may need to provide proof of address, such as a utility bill or a lease agreement, to further verify your identity. This is especially true if you're cashing a check at a bank where you don't have an account.

If you're unable to provide the necessary documentation and identification, you may still be able to cash your payroll check, but it could be more challenging. Some options include using a check cashing service that doesn't require ID, although these services often charge higher fees. Alternatively, you could try to cash the check at a bank where you have an established relationship, as they may be more lenient with their identification requirements.

It's important to note that the specific requirements for cashing a payroll check can vary depending on the issuer, the bank, and the check cashing service. Therefore, it's always a good idea to call ahead and confirm the necessary documentation and identification before attempting to cash your check.

Unlocking Payroll Funds: How Soon Can You Access Your Money?

You may want to see also

Explore related products

![]()

Alternative Options: Explore methods to cash a check without traditional ID, such as using a bank account

One alternative method to cash a check without traditional ID is by using a bank account. This approach can be particularly useful for individuals who may not have access to conventional identification documents but still need to access the funds from their payroll check. To utilize this method, you would need to have a bank account in your name. If you don’t already have one, you may be able to open an account with alternative forms of identification, such as a utility bill or a lease agreement, depending on the bank’s policies.

Once you have a bank account, you can deposit the check directly into your account. This can typically be done at a bank branch, through an ATM, or even via a mobile banking app if your bank offers this feature. After the check is deposited, the funds will be available in your account, usually within a few business days, depending on the bank’s processing times and the check’s clearing period.

Another advantage of using a bank account to cash a check is that it provides a secure and convenient way to manage your finances. You can easily track your transactions, pay bills, and transfer funds to other accounts as needed. Additionally, having a bank account can help you build financial credibility and may make it easier to obtain loans or credit cards in the future.

However, it’s important to note that some banks may have specific requirements or restrictions for cashing checks without traditional ID. For example, they may limit the amount of the check that can be deposited or require additional documentation to verify your identity. Therefore, it’s essential to check with your bank beforehand to understand their policies and procedures for cashing checks without ID.

In conclusion, using a bank account to cash a check without traditional ID can be a viable alternative for individuals who may not have access to conventional identification documents. This method provides a secure and convenient way to access the funds from your payroll check while also helping you manage your finances more effectively. However, it’s crucial to be aware of any specific requirements or restrictions that your bank may have in place for this type of transaction.

Exploring the Legality and Ethics of Businesses Cashing Employee Payroll Checks

You may want to see also

Explore related products

![]()

Legal Considerations: Learn about the legal implications and regulations surrounding check cashing without identification

Navigating the legal landscape of check cashing without identification can be complex. In the United States, for instance, the Bank Secrecy Act (BSA) and the USA PATRIOT Act impose stringent requirements on financial institutions to verify the identity of their customers. This is primarily to prevent money laundering and terrorist financing. As a result, most banks and check-cashing services will require some form of identification before cashing a check.

However, there are exceptions and variations to this rule. Some states have laws that allow for check cashing without identification under certain circumstances. For example, California's check cashing law permits the cashing of payroll checks without identification if the check is drawn on a federally insured bank and the amount does not exceed $250. It's crucial to note that these laws can change, and it's always best to consult with a legal professional or check the most current state regulations.

Furthermore, there are federal guidelines that can impact the ability to cash checks without identification. The Office of the Comptroller of the Currency (OCC) has issued guidelines that allow banks to offer check cashing services to individuals without requiring them to open an account, which can be beneficial for those without access to traditional banking services. However, these guidelines still emphasize the importance of identity verification to prevent fraud and other illegal activities.

In addition to federal and state laws, individual banks and check-cashing services may have their own policies and procedures regarding identification requirements. Some may offer alternative forms of verification, such as using biometric data or other non-traditional methods. It's important to check with the specific institution to understand their requirements.

Ultimately, while there are some scenarios where it may be possible to cash a payroll check without identification, it's generally more straightforward and safer to have proper identification. This not only helps to prevent fraud but also ensures that the individual has access to all the protections and services that come with having a verified account.

Can Handwritten Payroll Checks Be Tracked by the IRS?

You may want to see also

Explore related products

![]()

Bank Policies: Discover the specific policies of different banks regarding check cashing for individuals without ID

Bank policies regarding check cashing for individuals without ID can vary significantly. Some banks may require a government-issued ID, while others may accept alternative forms of identification such as a utility bill or a lease agreement. It's important to note that these policies are in place to prevent fraud and ensure the safety of both the bank and its customers.

For example, Bank of America requires a valid, government-issued ID to cash a check. This includes driver's licenses, state IDs, military IDs, and passports. However, they may make exceptions for certain situations, such as if the check is drawn from a Bank of America account and the customer is known to the bank.

On the other hand, Wells Fargo may accept alternative forms of identification, such as a utility bill or a lease agreement, if the customer is unable to provide a government-issued ID. However, they may limit the amount of the check that can be cashed in such cases.

It's also worth noting that some banks may have different policies for different types of checks. For instance, they may have stricter requirements for cashing a payroll check than for cashing a personal check. This is because payroll checks are often larger and may be more susceptible to fraud.

In conclusion, it's important to check with the specific bank where you plan to cash a check to understand their policies regarding identification. This will help you avoid any potential issues and ensure a smooth transaction.

Understanding Payroll Check Clearing Times: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Safety Measures: Find out about the security measures in place to prevent fraudulent check cashing without proper identification

Financial institutions have implemented several security measures to prevent fraudulent check cashing without proper identification. One such measure is the use of electronic verification systems that cross-reference the check details with the account holder's information in real-time. This system flags any discrepancies, such as an unauthorized signature or an attempt to cash a check from a closed account.

Another safety measure is the requirement for multiple forms of identification. Even if a check is legitimate, banks may ask for additional ID, such as a driver's license, passport, or state-issued ID card, to ensure the person presenting the check is the rightful owner. Some institutions may also require a secondary form of verification, like a fingerprint or a photo, to further confirm the individual's identity.

Furthermore, banks have trained their staff to recognize common signs of fraud, such as forged signatures, altered check amounts, or suspicious behavior from the person attempting to cash the check. Tellers are instructed to ask specific questions and observe the customer's reactions to detect any red flags that might indicate fraudulent activity.

In addition to these measures, financial institutions regularly update their security protocols to stay ahead of emerging fraud trends. They invest in advanced technologies, such as artificial intelligence and machine learning, to analyze patterns and identify potential threats before they can cause harm.

It's important to note that while these safety measures are in place, individuals should also take precautions to protect themselves from fraud. This includes keeping personal information secure, monitoring bank accounts regularly, and reporting any suspicious activity to the authorities.

In conclusion, the safety measures implemented by financial institutions play a crucial role in preventing fraudulent check cashing without proper identification. These measures, combined with individual vigilance, help to maintain the integrity of the financial system and protect consumers from potential losses.

Does Safeway Cash Payroll Checks? A Comprehensive Guide for Employees

You may want to see also

Frequently asked questions

Typically, you will need to provide identification to cash a payroll check. This is to verify your identity and ensure the check is being cashed by the correct person.

Common forms of ID accepted for cashing a payroll check include a driver's license, state ID card, passport, or military ID. The ID must be current and valid.

Some banks or check cashing services might have specific policies or exceptions, such as if you are a regular customer or if the check amount is below a certain threshold. However, these exceptions are not common and may vary by institution.

If you don't have ID, you may want to contact the issuer of the check to see if they can provide an alternative method of payment, such as direct deposit or a digital check. Alternatively, you could ask a trusted friend or family member with ID to cash the check for you, though this may involve additional steps or fees.