The question of whether payroll paid with a Paycheck Protection Program (PPP) loan can be deducted is a common one among business owners who have utilized this financial assistance during challenging economic times. The PPP, established as part of the CARES Act in response to the COVID-19 pandemic, provided loans to small businesses to help cover payroll and other eligible expenses. While the program offered a lifeline to many, it also raised questions about the tax implications of using these funds. Specifically, business owners have wondered if the payroll expenses covered by PPP loans are deductible on their tax returns, and if so, under what conditions. This inquiry is crucial for accurate tax planning and financial forecasting.

Explore related products

What You'll Learn

- PPP Loan Basics: Understanding the Paycheck Protection Program and its purpose for businesses

- Qualifying Expenses: Identifying which payroll costs are eligible for deduction under PPP guidelines

- Loan Forgiveness: Exploring the criteria for PPP loan forgiveness and its impact on tax deductions

- Tax Implications: Discussing how PPP loans affect business taxes and payroll deductions

- Recent Updates: Reviewing any recent changes or updates to PPP loan rules and regulations

![]()

PPP Loan Basics: Understanding the Paycheck Protection Program and its purpose for businesses

The Paycheck Protection Program (PPP) was established as part of the Coronavirus Aid, Relief, and Economic Security (CARES) Act in response to the COVID-19 pandemic. Its primary purpose is to provide financial assistance to eligible businesses to help them maintain their workforce and cover certain operational expenses during periods of economic uncertainty. The PPP offers loans that can be forgiven if the borrower meets specific criteria, such as using the funds for eligible expenses and retaining employees at their pre-pandemic salary levels.

One of the key aspects of the PPP is its focus on supporting small businesses and non-profit organizations. To be eligible for a PPP loan, a business must have fewer than 500 employees, although some exceptions apply for larger businesses in certain industries. The loan amount is typically based on the borrower's average monthly payroll costs, with a maximum loan amount of $10 million. The interest rate on PPP loans is relatively low, and the repayment term is typically two years.

The PPP loan funds can be used for a variety of eligible expenses, including payroll costs, rent, mortgage interest, and utilities. However, it is important to note that the funds cannot be used for certain purposes, such as paying off existing debt or purchasing new equipment. Borrowers must also ensure that they maintain accurate records of how the loan funds are used, as this information will be required to apply for loan forgiveness.

To apply for a PPP loan, businesses must submit an application through an approved lender. The application process typically requires documentation such as payroll records, tax returns, and proof of business ownership. Once approved, the loan funds are disbursed directly to the borrower, who can then use them for eligible expenses. It is crucial for borrowers to carefully review the loan terms and conditions, as well as the requirements for loan forgiveness, to ensure that they are able to fully benefit from the program.

In conclusion, the PPP is a valuable resource for businesses facing financial challenges due to the COVID-19 pandemic. By providing access to low-interest loans that can be forgiven under certain conditions, the program aims to help businesses retain their employees and continue operating during difficult times. However, it is essential for borrowers to understand the program's requirements and use the funds responsibly to maximize their chances of success.

Understanding Time Off Requests in US Payroll Timeclocks

You may want to see also

Explore related products

![]()

Qualifying Expenses: Identifying which payroll costs are eligible for deduction under PPP guidelines

To determine which payroll costs are eligible for deduction under PPP guidelines, it’s essential to understand the specific criteria set forth by the program. The Paycheck Protection Program (PPP) allows businesses to deduct certain payroll expenses when calculating the loan forgiveness amount. Eligible payroll costs include salaries, wages, and tips paid to employees, as well as certain benefits such as health insurance premiums and retirement contributions. However, it’s crucial to note that these expenses must be incurred during the covered period and paid with PPP loan funds to qualify for deduction.

One common misconception is that all payroll expenses are eligible for deduction. In reality, there are specific limitations and exclusions. For instance, payments made to independent contractors or sole proprietors are not considered eligible payroll costs. Additionally, any amounts paid to employees who earn more than $100,000 per year cannot be deducted. It’s also important to maintain accurate records and documentation to substantiate the payroll costs claimed for deduction.

When calculating eligible payroll costs, businesses should carefully review the PPP guidelines and consult with a qualified professional if needed. By understanding the criteria and limitations, businesses can ensure they are maximizing their loan forgiveness amount while remaining compliant with program requirements. Properly identifying and documenting eligible payroll costs is key to successfully navigating the PPP loan forgiveness process.

Maximize Your Health Savings: Payroll Contributions Explained

You may want to see also

Explore related products

![]()

Loan Forgiveness: Exploring the criteria for PPP loan forgiveness and its impact on tax deductions

To qualify for PPP loan forgiveness, businesses must meet specific criteria outlined by the Small Business Administration (SBA). One of the primary requirements is that the loan proceeds must be used for eligible expenses, such as payroll costs, rent, mortgage interest, or utilities. Additionally, the business must maintain its employee count and compensation levels during the covered period. The loan forgiveness amount is calculated based on the eligible expenses incurred during the specified timeframe, typically eight weeks after the loan disbursement.

The impact of PPP loan forgiveness on tax deductions is a critical aspect that businesses need to consider. Generally, the forgiven portion of the PPP loan is not considered taxable income, which means it does not increase the business's tax liability. However, the expenses paid with the forgiven loan proceeds, such as payroll costs, are not deductible for tax purposes. This is because the forgiven loan amount is essentially a form of tax-free income, and the IRS does not allow deductions for expenses paid with tax-free funds.

A common misconception is that the forgiven PPP loan amount can be used to offset other taxable income, thereby reducing the overall tax burden. However, this is not the case. The forgiven loan amount is treated as a separate entity and does not affect the taxability of other income or expenses. Businesses should consult with a tax professional to ensure they understand the specific implications of PPP loan forgiveness on their tax situation.

In summary, PPP loan forgiveness can provide significant financial relief to businesses that meet the eligibility criteria. However, it is essential to understand the tax implications of loan forgiveness to avoid any unexpected tax consequences. By carefully navigating the requirements and limitations of PPP loan forgiveness, businesses can maximize the benefits while minimizing potential tax issues.

Exploring EIDL: Can These Funds Cover Your Payroll Needs?

You may want to see also

Explore related products

![]()

Tax Implications: Discussing how PPP loans affect business taxes and payroll deductions

The Paycheck Protection Program (PPP) loans were a lifeline for many businesses during the COVID-19 pandemic, providing crucial funds to maintain operations and cover payroll costs. However, the tax implications of these loans can be complex and vary depending on several factors. One key aspect to consider is how PPP loans affect business taxes and payroll deductions.

Generally, PPP loans are considered taxable income for the business, but the interest on these loans is tax-deductible. This means that while the principal amount of the loan will increase the business's taxable income, the interest payments can be deducted as a business expense. It's important to note that the tax treatment of PPP loans may differ from other types of business loans, so it's crucial to consult with a tax professional to understand the specific implications for your business.

In terms of payroll deductions, PPP loans can be used to cover eligible payroll costs, such as salaries, wages, and certain benefits. These costs are typically subject to payroll taxes, including federal income tax withholding, Social Security tax, and Medicare tax. However, the tax treatment of payroll costs paid with PPP loan funds may be different from other payroll costs. For example, the IRS has issued guidance stating that payroll costs paid with PPP loan funds are not subject to federal income tax withholding, but they are still subject to Social Security tax and Medicare tax.

Businesses should also be aware of the potential for state tax implications when using PPP loan funds for payroll costs. Some states may have specific rules or regulations regarding the tax treatment of PPP loans, so it's important to check with your state's tax authority for guidance. Additionally, businesses should keep accurate records of how PPP loan funds are used, as this will be crucial for tax reporting and potential audits.

In conclusion, while PPP loans can provide essential support for businesses, it's important to understand the tax implications of using these funds for payroll costs. Consulting with a tax professional and staying informed about the latest tax guidance can help businesses navigate these complex issues and ensure compliance with all applicable tax laws.

Understanding Payroll Requirements: Social Security Cards and Employer Mandates

You may want to see also

Explore related products

![]()

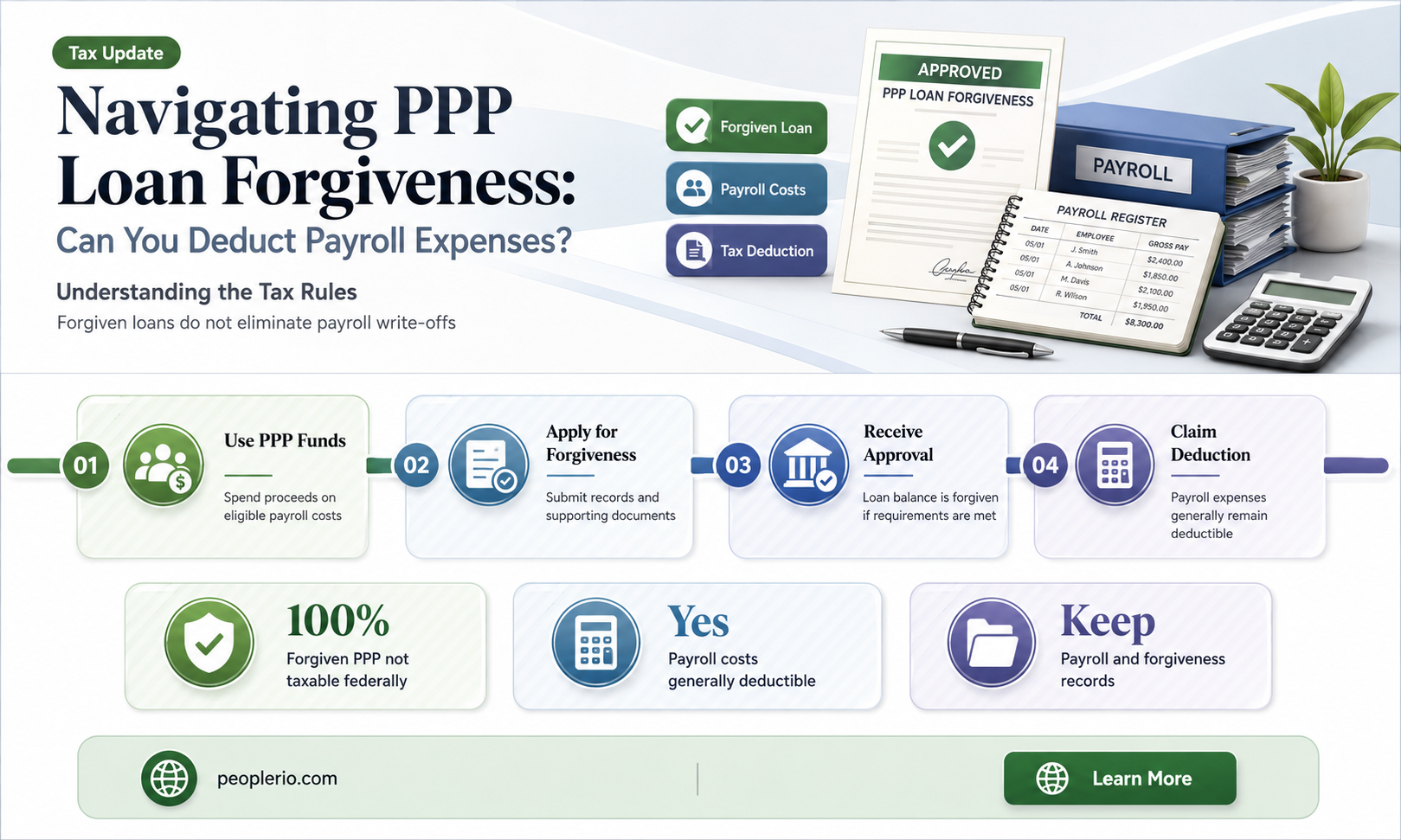

Recent Updates: Reviewing any recent changes or updates to PPP loan rules and regulations

The recent updates to PPP loan rules and regulations have brought about significant changes that business owners need to be aware of. One of the most pressing questions is whether payroll paid with a PPP loan can be deducted. The answer to this question has implications for how businesses manage their finances and plan for tax season.

Previously, the IRS had stated that expenses paid with PPP loan funds were not deductible. However, recent legislation has changed this stance. The Consolidated Appropriations Act, 2021, which was signed into law in December 2020, allows businesses to deduct expenses paid with PPP loan funds. This includes payroll costs, as well as other eligible expenses such as rent, utilities, and mortgage interest.

It's important to note that while the law now allows for these deductions, there are still some limitations and requirements that must be met. For example, the expenses must be directly related to the business's operations and cannot be personal expenses. Additionally, the business must have applied for and received a PPP loan in good faith, meaning that they must have had a genuine need for the funds and used them for their intended purpose.

To take advantage of these deductions, business owners should keep detailed records of their PPP loan expenses. This includes maintaining receipts, invoices, and other documentation that supports the business's use of the funds. It's also a good idea to consult with a tax professional to ensure that all deductions are properly claimed and that the business is in compliance with all applicable laws and regulations.

In conclusion, the recent updates to PPP loan rules and regulations have provided businesses with more flexibility in how they manage their finances and plan for tax season. By understanding these changes and taking the necessary steps to comply with the law, business owners can maximize their deductions and minimize their tax liability.

H1B Visa Holders: Understanding Payroll Cessation by Employers

You may want to see also

Frequently asked questions

Yes, you can deduct payroll costs paid with a PPP loan on your business tax return. The IRS has clarified that these expenses are deductible, even though the PPP loan itself is forgiven.

Eligible payroll costs include salaries, wages, tips, and employee benefits such as health insurance and retirement contributions. These costs must be incurred during the covered period of the PPP loan.

There is no specific limit to the amount of payroll costs you can deduct if paid with a PPP loan. However, the total amount of eligible expenses cannot exceed the loan amount received.

If the PPP loan is not forgiven, you can still deduct the payroll costs incurred during the covered period. The loan itself would need to be repaid, but the payroll expenses are deductible as usual.

While there are no special requirements, it is important to maintain accurate records and documentation of payroll costs incurred during the covered period. This will help substantiate the deductions claimed on your business tax return.