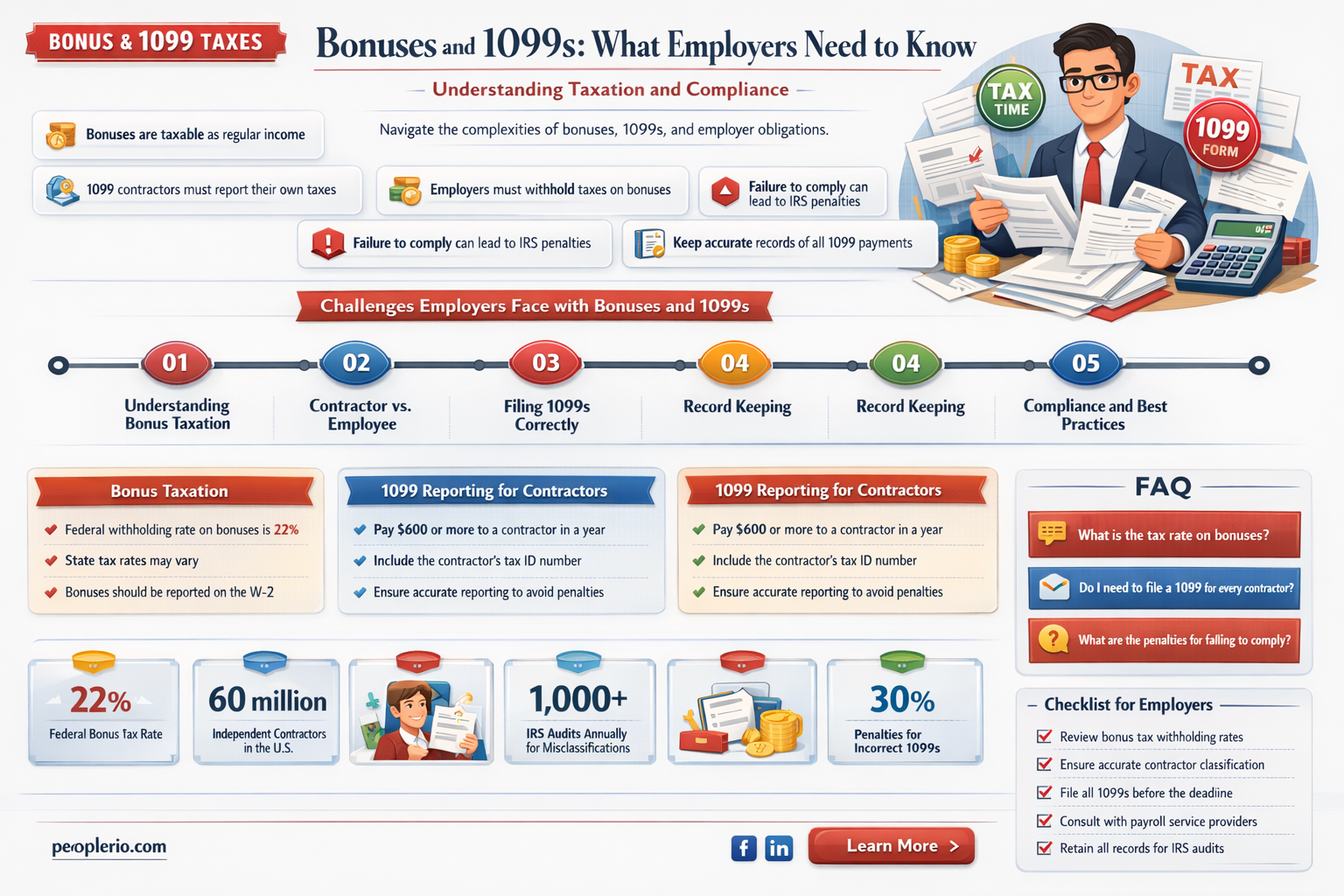

The question of whether an employee can be issued a 1099 form for a bonus is a common one in the realm of tax and employment law. Generally, bonuses are considered taxable income and are subject to withholding and reporting requirements. However, the specific circumstances under which a 1099 form should be used can vary. For instance, if the bonus is given to an independent contractor rather than an employee, a 1099 might be appropriate. On the other hand, if the bonus is given to an employee, it would typically be reported on a W-2 form. It's crucial to understand the tax implications and legal distinctions to ensure compliance with IRS regulations and avoid potential penalties.

| Characteristics | Values |

|---|---|

| Employee Type | Regular, Full-time |

| Bonus Type | Performance-based, Discretionary |

| Payment Method | Lump sum, Separate check |

| Tax Reporting | Reported on W-2, Subject to withholding |

| Legal Compliance | Must comply with labor laws, No discrimination |

| Documentation | Written agreement, Performance records |

Explore related products

![[BEST PRACTICE] Find the Perfect Training: Incl. Bonus – Selection criteria, financing, checklists, practical examples for success on the labour market (Best Practice Edition)](https://m.media-amazon.com/images/I/71Nu54i1+7L._AC_UY218_.jpg)

What You'll Learn

- Definition of 1099 Employee: An independent contractor, not a regular employee, with flexibility in work and responsibilities

- Bonus Classification: A bonus can be classified as miscellaneous income or non-employee compensation on a 1099 form

- Tax Implications: Both the employer and the 1099 employee have tax obligations for the bonus amount

- Reporting Requirements: Employers must report 1099 payments to the IRS and provide a copy to the contractor

- Legal Considerations: Ensure compliance with labor laws and regulations when classifying workers and issuing bonuses

![]()

Definition of 1099 Employee: An independent contractor, not a regular employee, with flexibility in work and responsibilities

A 1099 employee is fundamentally different from a traditional W-2 employee. While W-2 employees are considered regular workers with consistent schedules and responsibilities, 1099 employees are independent contractors who have more autonomy over their work. This distinction is crucial for employers when considering how to compensate their workers, especially when it comes to bonuses.

One of the key benefits of being a 1099 employee is the flexibility it offers. Independent contractors can often set their own schedules, choose their projects, and work from any location they prefer. This level of autonomy can be highly appealing to professionals who value work-life balance or have specific personal commitments. However, this flexibility also means that 1099 employees are responsible for managing their own time and resources effectively, which can be challenging for some individuals.

From an employer's perspective, hiring 1099 employees can provide significant advantages. Employers are not required to pay payroll taxes, provide health insurance, or offer other benefits typically associated with full-time employment. This can result in substantial cost savings for businesses, especially those that are just starting out or operating on a tight budget. Additionally, employers can often hire 1099 employees on a project-by-project basis, allowing them to scale their workforce up or down as needed without the long-term commitment of full-time hires.

However, it's important to note that misclassifying an employee as a 1099 contractor can have serious legal and financial consequences. The IRS has strict guidelines for determining whether a worker is an employee or an independent contractor, and employers must ensure that they are in compliance with these regulations. Failure to do so can result in penalties, back taxes, and even lawsuits from misclassified workers seeking benefits and compensation.

In the context of bonuses, 1099 employees are typically not eligible for the same types of bonuses as W-2 employees. Since bonuses are often considered a form of compensation for regular employees, they may not be applicable to independent contractors who are already being paid for their specific services or projects. However, employers may still choose to offer bonuses to 1099 employees as a way to incentivize exceptional performance or to foster a positive working relationship. In such cases, it's important for employers to clearly communicate the terms and conditions of the bonus to avoid any misunderstandings or disputes.

Ultimately, understanding the definition and implications of a 1099 employee is essential for both employers and workers. By recognizing the unique characteristics and benefits of independent contracting, businesses can make informed decisions about their workforce and compensation strategies, while professionals can choose the work arrangement that best suits their needs and preferences.

Addressing Poor Documentation: How to Write Up an Employee Effectively

You may want to see also

Explore related products

![]()

Bonus Classification: A bonus can be classified as miscellaneous income or non-employee compensation on a 1099 form

A bonus can indeed be classified as miscellaneous income or non-employee compensation on a 1099 form, but this classification depends on the nature of the bonus and the relationship between the payer and the recipient. Typically, bonuses given to employees as part of their regular compensation package are considered wages and are reported on a W-2 form. However, if a bonus is given to a non-employee, such as a contractor or freelancer, or if it is considered a special payment outside of regular wages, it may be reported on a 1099 form.

The classification of a bonus as miscellaneous income or non-employee compensation can have significant tax implications for the recipient. Miscellaneous income is generally subject to self-employment tax, which means the recipient may need to pay both the employee and employer portions of Social Security and Medicare taxes. Non-employee compensation, on the other hand, is not subject to self-employment tax, but the recipient may still need to pay income tax on the bonus.

To determine whether a bonus should be classified as miscellaneous income or non-employee compensation on a 1099 form, the payer should consider the following factors: the nature of the payment, the relationship between the payer and the recipient, and any contractual agreements in place. If the bonus is a one-time payment for services rendered and there is no ongoing employment relationship, it is more likely to be classified as non-employee compensation. However, if the bonus is part of a regular compensation package or is given to an employee as an incentive, it is more likely to be classified as miscellaneous income.

In conclusion, the classification of a bonus as miscellaneous income or non-employee compensation on a 1099 form depends on the specific circumstances of the payment. It is important for payers to carefully consider the nature of the bonus and the relationship with the recipient to ensure accurate reporting and compliance with tax laws. Recipients should also be aware of the tax implications of receiving a bonus classified as miscellaneous income or non-employee compensation and should consult with a tax professional if they have any questions or concerns.

Understanding Employee Classification: The 1099 vs W-2 Debate

You may want to see also

Explore related products

![]()

Tax Implications: Both the employer and the 1099 employee have tax obligations for the bonus amount

The tax implications for both the employer and the 1099 employee regarding a bonus amount are multifaceted and require careful consideration. From the employer's perspective, bonuses paid to 1099 employees are generally considered taxable income and must be reported on the employee's Form 1099-MISC. This means the employer is responsible for withholding taxes from the bonus amount and ensuring accurate reporting to the IRS. Failure to do so can result in penalties and fines for the employer.

For the 1099 employee, receiving a bonus can significantly impact their tax liability. Unlike regular employees who have taxes withheld from their paychecks, 1099 employees are responsible for paying their own taxes, including self-employment tax, income tax, and any applicable state and local taxes. This means that when a 1099 employee receives a bonus, they must set aside a portion of the funds to cover their tax obligations. It's crucial for 1099 employees to understand their tax responsibilities and plan accordingly to avoid any surprises during tax season.

One unique aspect of taxing bonuses for 1099 employees is the potential for the bonus to push the employee into a higher tax bracket. Since 1099 employees are responsible for paying their own taxes, a large bonus can increase their overall income and potentially lead to a higher tax rate. This underscores the importance of careful tax planning and consultation with a tax professional to ensure that both the employer and the 1099 employee are prepared for the tax implications of a bonus.

In addition to federal taxes, state and local taxes must also be considered. Some states have specific rules regarding the taxation of bonuses, and it's essential for both the employer and the 1099 employee to be aware of these regulations. For example, some states may require additional withholding or reporting for bonuses, while others may have different tax rates for bonuses compared to regular income.

To navigate these complex tax implications, both employers and 1099 employees should consider seeking guidance from a tax professional. A tax expert can provide personalized advice and ensure that all tax obligations are met, helping to avoid potential penalties and fines. By understanding and addressing the tax implications of bonuses, both parties can ensure compliance with tax laws and make informed financial decisions.

Navigating 1099 Forms for Former Employees: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Reporting Requirements: Employers must report 1099 payments to the IRS and provide a copy to the contractor

Employers have specific reporting obligations when it comes to 1099 payments, which are crucial for both tax compliance and maintaining accurate financial records. The IRS requires that any payment made to a contractor or freelancer, typically classified as a non-employee, must be reported on a 1099 form. This form serves as a record of the income received by the contractor and is used by the IRS to ensure that the individual reports the income on their tax return.

The process of reporting 1099 payments involves several key steps. First, employers must gather the necessary information about the contractors they have paid, including their name, address, and taxpayer identification number (TIN). This information is typically collected at the beginning of the year or when the contractor is first hired. Employers must then keep track of all payments made to each contractor throughout the year, ensuring that they accurately report the total amount paid on the 1099 form.

One common misconception is that 1099 forms are only required for large payments or for payments made to individuals who work for the employer on a regular basis. However, the IRS requires that any payment made to a contractor, regardless of the amount or frequency, must be reported on a 1099 form. This includes one-time payments, such as bonuses or commissions, as well as regular payments for services rendered.

Failure to report 1099 payments can result in penalties for the employer, including fines and interest on the unpaid taxes. Additionally, the contractor may face difficulties when filing their tax return if they do not receive a 1099 form, as they may not be aware of the income they received or may have difficulty proving the amount of income they earned.

To avoid these issues, employers should ensure that they have a system in place for tracking and reporting 1099 payments. This may involve using accounting software or working with a tax professional to ensure that all payments are accurately recorded and reported. By following the IRS's reporting requirements, employers can help ensure that both they and their contractors remain in compliance with tax laws and regulations.

Navigating 1099 Forms for Part-Time Employees: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Legal Considerations: Ensure compliance with labor laws and regulations when classifying workers and issuing bonuses

Navigating the complex landscape of labor laws and regulations is crucial when classifying workers and issuing bonuses, especially in the context of 1099 employees. Misclassification can lead to significant legal and financial repercussions for businesses. To ensure compliance, employers must understand the distinctions between employees and independent contractors, as well as the criteria used by the IRS and state labor departments to determine worker status.

One key consideration is the level of control an employer has over the worker. If the employer dictates the worker's schedule, tasks, and methods of work, this suggests an employment relationship rather than an independent contractor arrangement. Additionally, the permanence of the relationship and the extent to which the worker is integrated into the company's operations are important factors. Employers should also consider the economic realities of the situation, such as whether the worker relies on the company for their livelihood and whether they have the opportunity to profit or lose money based on their work performance.

When it comes to issuing bonuses, employers must be mindful of the tax implications and reporting requirements. Bonuses paid to 1099 employees are generally considered taxable income and must be reported on the employee's 1099 form. Employers should also ensure that they are withholding the appropriate amount of taxes from the bonus payment, if required. Furthermore, employers should be aware of any state-specific laws and regulations regarding bonus payments, as these can vary significantly from federal guidelines.

To mitigate the risk of misclassification and ensure compliance with labor laws, employers should consult with legal and tax professionals. These experts can provide guidance on proper classification procedures and help employers develop policies and practices that align with federal and state regulations. Regular audits and reviews of worker classifications can also help identify and correct any potential issues before they become major problems.

In conclusion, ensuring compliance with labor laws and regulations when classifying workers and issuing bonuses is a critical aspect of managing a workforce. By understanding the key factors that determine worker status and staying informed about tax implications and reporting requirements, employers can avoid costly mistakes and maintain a legally sound operation.

Navigating 1099 Forms for Full-Time Employees: A Comprehensive Guide

You may want to see also

Frequently asked questions

Yes, you can issue a 1099 form to an employee for a bonus. The 1099 form is used to report miscellaneous income, which includes bonuses, to the Internal Revenue Service (IRS).

The purpose of a 1099 form is to report miscellaneous income to the IRS. This includes income that is not subject to withholding, such as bonuses, commissions, and rental income.

Anyone who receives miscellaneous income of $600 or more during the tax year is required to receive a 1099 form. This includes employees who receive bonuses.

To fill out a 1099 form for an employee bonus, you will need to provide the employee's name, address, and social security number. You will also need to report the amount of the bonus in Box 7 of the form.

If you do not issue a 1099 form for an employee bonus, you may be subject to penalties from the IRS. Additionally, the employee may not be able to report the bonus income on their tax return, which could lead to them owing more taxes.