A paragraph introducing the topic 'can you adjust your simple ira contribution as an employee':

Understanding the flexibility of your retirement savings plan is crucial for effective financial planning. If you're an employee with a Simple Individual Retirement Account (IRA), you might be wondering about the possibility of adjusting your contributions. The good news is that, in most cases, you can modify your Simple IRA contributions subject to certain rules and limits. This allows you to adapt your retirement savings strategy to changes in your financial situation or goals. However, it's important to be aware of the specific guidelines and potential implications of such adjustments to ensure you're making the most informed decisions for your future.

| Characteristics | Values |

|---|---|

| Contribution Type | Simple IRA |

| Contributor | Employee |

| Adjustability | Yes |

| Contribution Limit | Varies by year, typically $15,500 (2023) |

| Catch-Up Contributions | Additional $3,000 for those 50 and older |

| Investment Options | Limited to IRA-eligible investments |

| Tax Implications | Contributions are pre-tax, reducing taxable income |

| Withdrawal Rules | Generally, funds can be withdrawn at age 59.5+ |

| Penalties for Early Withdrawal | 10% penalty plus taxes on earnings |

| Required Minimum Distributions | Start at age 73 (as of 2023) |

| Employer Involvement | Employer may match contributions |

Explore related products

What You'll Learn

- Contribution Limits: Understand the annual maximums and adjust accordingly

- Payroll Deductions: Coordinate with HR to modify deduction amounts

- Investment Options: Review and select appropriate funds within your IRA

- Tax Implications: Consult a tax advisor to optimize contributions for tax benefits

- Withdrawal Rules: Familiarize yourself with early withdrawal penalties and exceptions

![]()

Contribution Limits: Understand the annual maximums and adjust accordingly

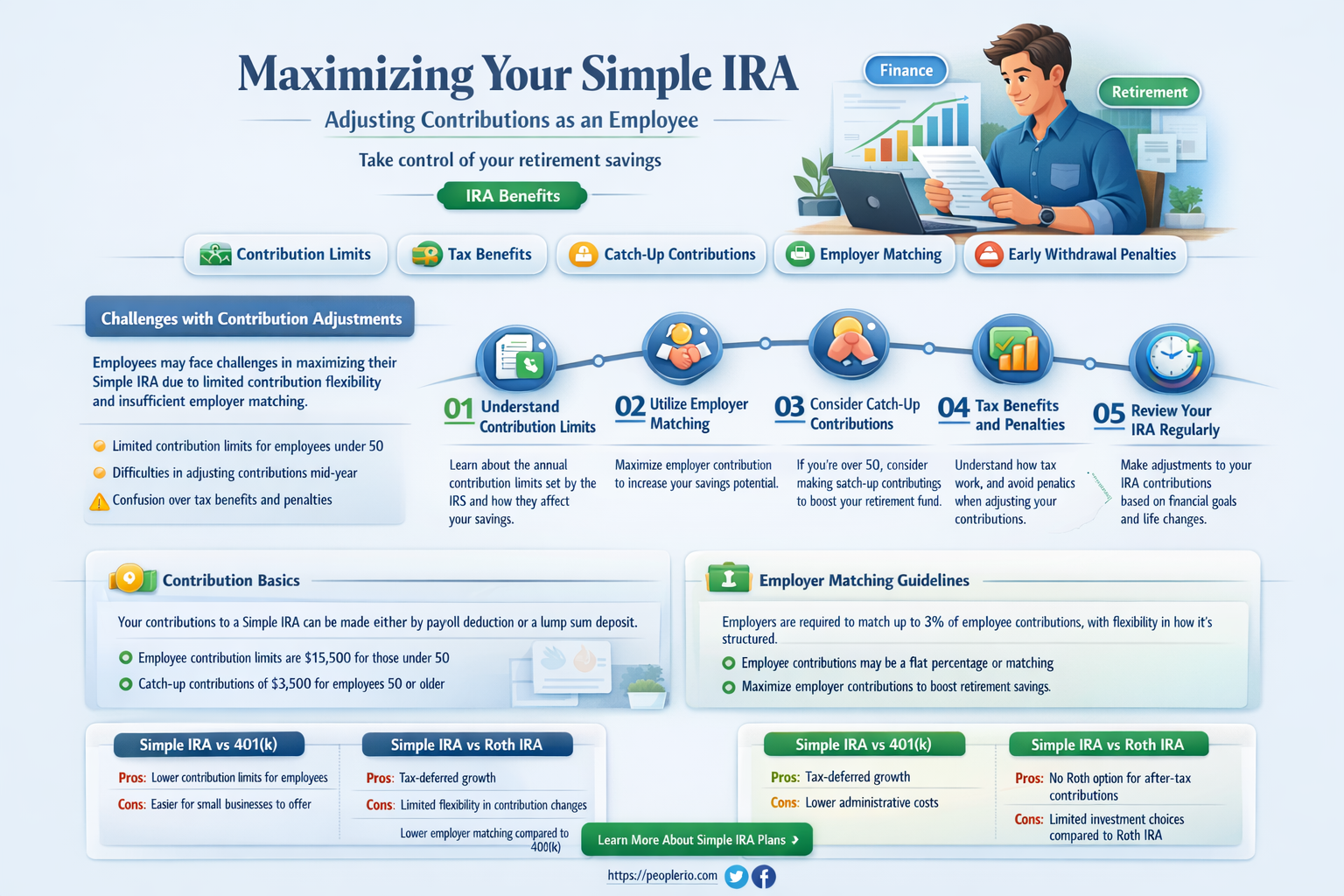

Understanding the contribution limits for your Simple IRA is crucial for maximizing your retirement savings while staying within the legal guidelines set by the IRS. As of 2023, the annual contribution limit for a Simple IRA is $15,500 for employees under the age of 50. If you are 50 or older, you are allowed an additional catch-up contribution of $3,000, bringing your total to $18,500. These limits are subject to change, so it's essential to stay updated on the current IRS guidelines.

To adjust your contributions accordingly, you should first review your current contribution amount and compare it to the annual maximum. If you are not contributing the full amount allowed, consider increasing your contributions to take advantage of the tax benefits and maximize your retirement savings. Keep in mind that any contributions you make above the annual limit will be subject to penalties and taxes.

One strategy to ensure you are contributing within the limits is to set up automatic contributions through your employer's payroll deduction system. This way, you can split your contributions evenly throughout the year and avoid the risk of over-contributing. Additionally, if you receive a bonus or a raise, consider allocating a portion of that extra income towards your Simple IRA to boost your savings without exceeding the contribution limits.

It's also important to be aware of any employer matching contributions, as these can impact your overall contribution limit. Some employers may match a certain percentage of your contributions, which can help you reach the maximum limit more quickly. However, be cautious not to rely too heavily on employer matching, as it may not always be guaranteed.

In summary, understanding and adjusting your Simple IRA contributions within the annual limits is key to optimizing your retirement savings. By staying informed about the current IRS guidelines, reviewing your contributions regularly, and utilizing strategies such as automatic contributions and employer matching, you can make the most of your Simple IRA while avoiding potential penalties and taxes.

Using Employee Class as Key in HashMap: Best Practices and Pitfalls

You may want to see also

Explore related products

![]()

Payroll Deductions: Coordinate with HR to modify deduction amounts

To modify your payroll deductions for a Simple IRA, you'll need to coordinate with your Human Resources department. This process typically involves submitting a request form or updating your contribution information through an online portal provided by your employer. It's important to note that changes to your payroll deductions may take a few pay cycles to process, so plan accordingly if you're looking to adjust your contributions for a specific reason, such as reaching the annual contribution limit or changing your financial situation.

When coordinating with HR, be prepared to provide the specific amount you wish to deduct from each paycheck. You may also need to specify the frequency of the deductions, such as weekly, bi-weekly, or monthly. Keep in mind that there may be minimum or maximum contribution limits set by your employer or the IRS, so review these guidelines before submitting your request.

In some cases, your employer may offer an automatic escalation feature, which allows you to increase your contributions by a certain percentage each year. This can be a helpful tool for maximizing your retirement savings without having to manually adjust your deductions annually. However, be aware that this feature may not be available with all employers or retirement plans.

If you're unsure about the process or have questions about your specific situation, don't hesitate to reach out to your HR representative or a financial advisor for guidance. They can help you navigate the process and ensure that you're making the best decisions for your financial future.

Remember, adjusting your payroll deductions is an important step in managing your retirement savings. By coordinating with HR and staying informed about your contribution options, you can take control of your financial future and work towards a more secure retirement.

Can Wegmans Employees Accept Tips? Understanding the Policy and Etiquette

You may want to see also

Explore related products

![]()

Investment Options: Review and select appropriate funds within your IRA

Once you've determined the maximum contribution limit for your Simple IRA, the next crucial step is selecting the right investment funds. This decision can significantly impact your retirement savings growth and overall financial security. Start by reviewing the investment options available within your IRA plan. Typically, these may include a range of mutual funds, exchange-traded funds (ETFs), and possibly individual stocks or bonds.

Consider your risk tolerance and investment horizon when choosing funds. If you're younger and have a longer time until retirement, you may opt for more aggressive investments with higher potential returns, such as growth stocks or high-yield bonds. Conversely, if you're closer to retirement age, you might prefer more conservative options like dividend-paying stocks, index funds, or short-term bonds to preserve your capital.

Diversification is key to minimizing risk. Spread your contributions across different asset classes and sectors to avoid overexposure to any single market segment. For example, you might allocate a portion of your portfolio to technology stocks, another to healthcare, and a third to international markets. Regularly rebalancing your portfolio can also help maintain an optimal asset allocation over time.

Pay attention to the fees associated with each fund, as these can eat into your returns. Look for funds with low expense ratios, and consider the impact of transaction costs when buying and selling shares. Additionally, be aware of any minimum investment requirements or restrictions that may apply to certain funds within your IRA.

Finally, if you're unsure about how to proceed, consider consulting with a financial advisor or using a robo-advisor service. These professionals can provide personalized guidance based on your specific financial situation and goals, helping you make informed investment decisions that align with your overall retirement strategy.

Understanding Employee Classification: The 1099 vs W-2 Debate

You may want to see also

![]()

Tax Implications: Consult a tax advisor to optimize contributions for tax benefits

Navigating the tax landscape can be complex, especially when it comes to optimizing retirement contributions. Consulting a tax advisor is crucial to ensure that your Simple IRA contributions are structured in a way that maximizes tax benefits. A tax professional can provide tailored advice based on your specific financial situation, helping you to avoid common pitfalls and make the most of available tax incentives.

One key consideration is the timing of your contributions. Contributions to a Simple IRA must be made by the tax filing deadline, typically April 15th, to be eligible for tax deductions in the previous year. A tax advisor can help you strategize the best time to make contributions to align with your tax planning goals. Additionally, they can guide you on how to coordinate your Simple IRA contributions with other retirement accounts, such as a 401(k) or Roth IRA, to optimize your overall retirement savings strategy.

Another important aspect to consider is the impact of your contributions on your taxable income. Simple IRA contributions are generally tax-deductible, which can help reduce your taxable income and potentially lower your tax liability. However, there are limits to how much you can contribute each year, and exceeding these limits can result in penalties. A tax advisor can help you navigate these contribution limits and ensure that you are maximizing your deductions without running afoul of IRS regulations.

Furthermore, a tax advisor can provide insights into how changes in tax laws may affect your Simple IRA contributions. Tax legislation is subject to change, and staying informed about these changes is essential to maintaining an effective retirement savings strategy. By working with a tax professional, you can stay up-to-date on the latest tax developments and adjust your contributions accordingly to optimize your tax benefits.

In conclusion, consulting a tax advisor is a valuable step in optimizing your Simple IRA contributions for tax benefits. They can provide personalized guidance on contribution timing, coordination with other retirement accounts, adherence to contribution limits, and staying informed about tax law changes. By leveraging their expertise, you can ensure that your retirement savings strategy is both effective and tax-efficient.

Negotiating Your Raise: Understanding Percentage Increases as an Employee

You may want to see also

![]()

Withdrawal Rules: Familiarize yourself with early withdrawal penalties and exceptions

Familiarizing yourself with the withdrawal rules of your Simple IRA is crucial to avoid unexpected penalties and make the most of your retirement savings. One key aspect to understand is the early withdrawal penalty, which typically applies if you withdraw funds before reaching age 59½. This penalty is designed to discourage premature use of retirement funds and ensure they are available when you truly need them.

The early withdrawal penalty usually consists of a 10% tax on the withdrawn amount, in addition to any regular income tax owed. However, there are several exceptions to this rule that you should be aware of. For instance, if you use the withdrawn funds for qualified education expenses, such as tuition and fees for yourself, your spouse, or your dependents, you may be exempt from the penalty. Similarly, if you are using the funds to purchase your first home, you may be able to withdraw up to $10,000 penalty-free.

Another important exception is for individuals who become disabled. If you are unable to work due to a disability, you may be able to withdraw funds from your Simple IRA without incurring the early withdrawal penalty. Additionally, if you are a reservist or National Guard member called to active duty, you may also be eligible for penalty-free withdrawals.

It's essential to note that while these exceptions can help you avoid the early withdrawal penalty, you will still need to pay regular income tax on the withdrawn funds. Furthermore, if you do not qualify for an exception, the penalty can significantly reduce the value of your withdrawal, making it a less attractive option.

To navigate these rules effectively, it's recommended that you consult with a financial advisor or tax professional who can provide personalized guidance based on your specific circumstances. They can help you understand the implications of different withdrawal strategies and ensure you are making informed decisions about your retirement savings.

In summary, understanding the withdrawal rules of your Simple IRA, including the early withdrawal penalty and its exceptions, is vital for managing your retirement funds wisely. By familiarizing yourself with these rules and seeking professional advice when needed, you can make the most of your savings and avoid costly mistakes.

Addressing Poor Documentation: How to Write Up an Employee Effectively

You may want to see also

Frequently asked questions

Yes, you can adjust your Simple IRA contribution as an employee. You have the flexibility to change the amount you contribute to your Simple IRA plan at any time during the year.

To adjust your Simple IRA contribution, you need to contact your plan administrator or the human resources department at your employer. They will provide you with the necessary forms or online portal access to modify your contribution amount.

Yes, there is a contribution limit for Simple IRAs. As of 2023, the maximum contribution limit for employees is $15,500 per year. However, this limit may change over time due to inflation adjustments, so it's essential to check the current limit with your plan administrator or the IRS.

Yes, you can stop contributing to your Simple IRA temporarily. If you need to pause your contributions for any reason, such as a financial hardship or a change in employment status, you can do so by notifying your plan administrator or the human resources department at your employer. Keep in mind that stopping contributions may impact your long-term retirement savings goals.