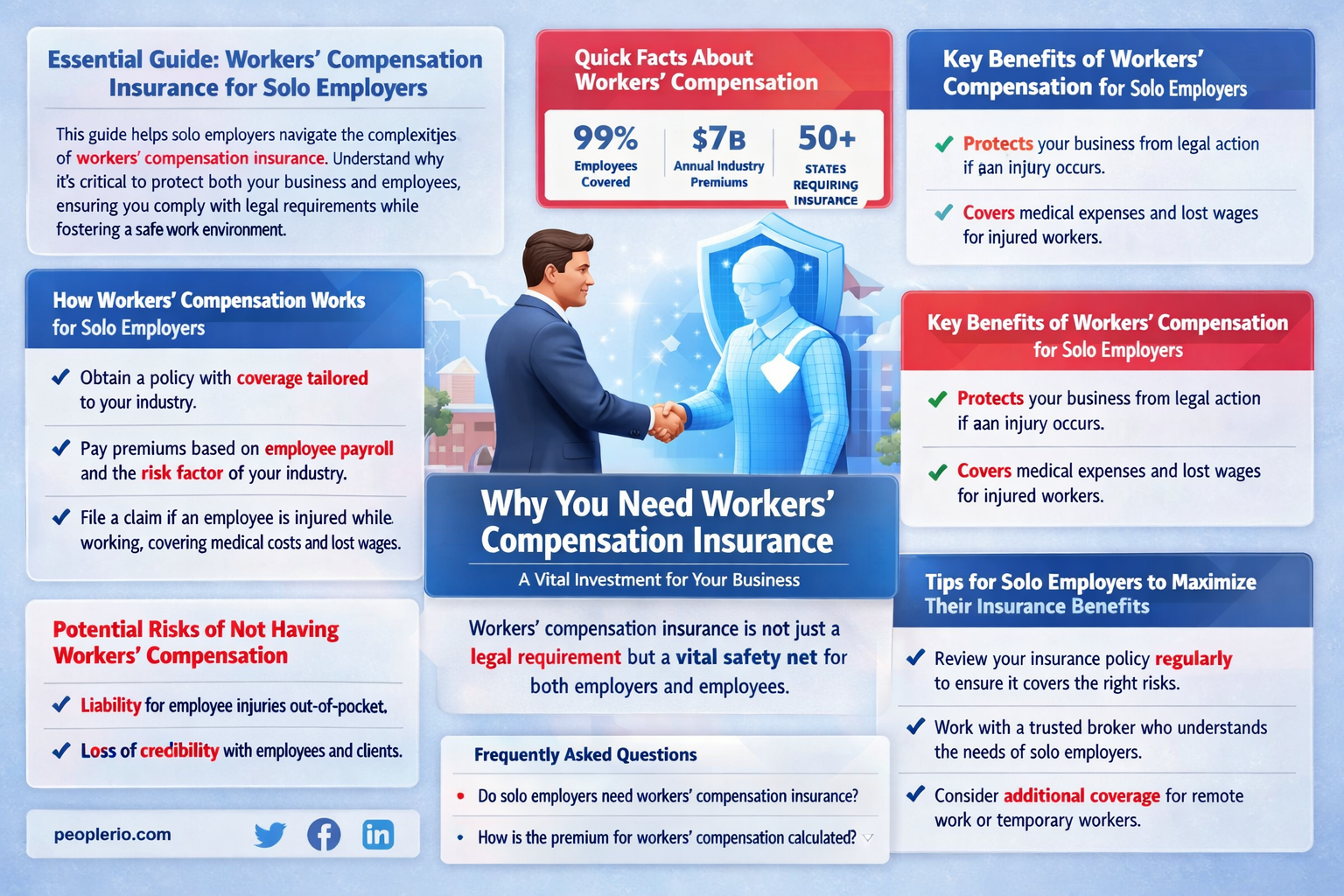

Workers' compensation insurance is a crucial aspect of business operations, especially when it comes to protecting your employees. If you're a business owner with even just one employee, you might be wondering whether you need workers' compensation insurance. The answer is yes, in most cases. Workers' compensation insurance provides financial protection for employees who suffer work-related injuries or illnesses, covering medical expenses and lost wages. Even with a single employee, the risk of workplace accidents exists, and having this insurance in place can help safeguard both your employee and your business from potential financial burdens. It's essential to check the specific requirements in your state, as some may have different regulations regarding the number of employees needed to mandate workers' compensation insurance.

Explore related products

What You'll Learn

- Legal Requirements: Understand state-specific mandates for workers' compensation insurance coverage

- Employee Eligibility: Determine which employees qualify for coverage under workers' compensation laws

- Cost Factors: Evaluate the financial aspects, including premiums and potential claims costs

- Risk Assessment: Consider the nature of work and associated risks to decide on insurance necessity

- Alternative Options: Explore other insurance types or self-insurance options if applicable

![]()

Legal Requirements: Understand state-specific mandates for workers' compensation insurance coverage

Workers' compensation insurance is a critical aspect of business operations, especially when it comes to ensuring compliance with legal requirements. Each state has its own set of mandates regarding workers' compensation coverage, which can vary significantly. For instance, some states require coverage for all employees, regardless of the number, while others have specific thresholds, such as requiring coverage only if a business has four or more employees.

Understanding these state-specific mandates is crucial for business owners to avoid legal repercussions and ensure they are providing the necessary protections for their workers. It's important to note that failing to comply with these requirements can result in hefty fines, penalties, and even the loss of business licenses. Therefore, it's essential for employers to familiarize themselves with the laws in their state and take the appropriate steps to secure the required coverage.

One of the key aspects of workers' compensation insurance is that it provides financial protection to employees who are injured on the job or develop work-related illnesses. This coverage typically includes medical expenses, lost wages, and rehabilitation costs. In exchange for this protection, employees generally waive their right to sue their employer for negligence related to their injuries.

When determining whether workers' compensation insurance is necessary for a business with only one employee, it's important to consider the specific laws in the state where the business operates. Some states, such as Texas and Florida, do not require workers' compensation coverage for businesses with fewer than four employees. However, other states, like California and New York, have more stringent requirements and may mandate coverage even for businesses with a single employee.

In addition to state-specific mandates, there are also federal requirements that businesses must consider. For example, the Federal Employers Liability Act (FELA) requires railroad employers to provide workers' compensation coverage to their employees. Similarly, the Longshore and Harbor Workers' Compensation Act (LHWCA) mandates coverage for maritime workers.

Ultimately, the decision of whether to obtain workers' compensation insurance for a business with one employee depends on the specific legal requirements in the state where the business operates. However, even if coverage is not legally required, it may still be a prudent business decision to secure insurance to protect both the employee and the business in the event of a workplace injury.

Understanding Workers' Comp Insurance Costs in California

You may want to see also

Explore related products

![]()

Employee Eligibility: Determine which employees qualify for coverage under workers' compensation laws

To determine employee eligibility for workers' compensation coverage, it's essential to understand the specific criteria set forth by your state's laws. Generally, employees are eligible if they are injured or become ill as a direct result of their job duties. This includes full-time, part-time, and seasonal workers, as well as some independent contractors, depending on the state's definition of an employee.

The first step in determining eligibility is to review your state's workers' compensation statutes. These laws will outline the specific requirements for coverage, including the types of injuries or illnesses that qualify, the timeframe for reporting the injury, and any exclusions or limitations. For example, some states may exclude certain types of workers, such as volunteers or undocumented immigrants, from coverage.

Once you have a clear understanding of your state's laws, you can begin to assess each employee's situation individually. This involves gathering detailed information about the employee's job duties, the nature of their injury or illness, and the circumstances surrounding the incident. You may need to conduct interviews, review medical records, and gather witness statements to ensure you have a comprehensive understanding of the situation.

After gathering all the necessary information, you can make a determination about the employee's eligibility for workers' compensation coverage. If the employee meets the criteria set forth by your state's laws, you will need to file a claim with your workers' compensation insurance carrier. If the employee does not meet the criteria, you may need to provide them with alternative options for medical care and financial support.

It's important to note that determining employee eligibility for workers' compensation coverage can be a complex and time-consuming process. If you are unsure about any aspect of the process, it's recommended that you consult with a qualified legal professional or a workers' compensation insurance expert. They can provide you with guidance and support to ensure that you are making accurate and informed decisions about employee eligibility.

Exploring Self-Insurance Options for Workers' Compensation in California

You may want to see also

Explore related products

![]()

Cost Factors: Evaluate the financial aspects, including premiums and potential claims costs

Evaluating the financial aspects of workers' compensation insurance involves a detailed analysis of both premiums and potential claims costs. Premiums are the regular payments made to the insurance carrier to maintain coverage, while claims costs are the expenses incurred when an employee files a claim for a work-related injury or illness.

To accurately assess premiums, it's essential to understand the factors that influence them. These include the classification of your business, the payroll size, the claims history, and the state in which you operate. Insurance carriers use these factors to determine the level of risk associated with your business and, consequently, the premium rates. For instance, a business classified as high-risk, such as construction or manufacturing, will likely face higher premiums compared to a low-risk business like an office-based company.

Claims costs can be more challenging to predict but are equally important to consider. These costs can include medical expenses, lost wages, rehabilitation costs, and legal fees. The severity and frequency of claims can significantly impact your business's financial health. For example, a single severe claim can result in substantial costs that may exceed the annual premium payments.

To mitigate these financial risks, it's crucial to implement effective risk management strategies. This can involve creating a safe work environment, providing proper training to employees, and having a comprehensive return-to-work program. By reducing the likelihood and severity of claims, you can potentially lower both your premiums and claims costs.

In conclusion, evaluating the financial aspects of workers' compensation insurance requires a thorough understanding of premium factors and claims costs. By proactively managing risks and maintaining a safe work environment, you can help ensure that your business remains financially stable and protected against potential liabilities.

Exploring the Trends: Has Workers' Compensation Insurance Seen a Decline?

You may want to see also

Explore related products

![]()

Risk Assessment: Consider the nature of work and associated risks to decide on insurance necessity

To determine whether workers' compensation insurance is necessary for a single employee, a thorough risk assessment is crucial. This involves evaluating the nature of the work being performed and identifying potential hazards or risks associated with it. For instance, if the employee is involved in manual labor, construction, or any activity that poses a physical risk, workers' compensation insurance would likely be essential. On the other hand, if the employee's role is primarily administrative and office-based, the need for such insurance might be less apparent.

When conducting a risk assessment, it's important to consider both the likelihood and severity of potential injuries or illnesses. This can be done by reviewing historical data on workplace accidents, consulting with industry experts, and observing the work environment firsthand. By understanding the specific risks involved, an employer can make an informed decision about the necessity of workers' compensation insurance.

Moreover, employers should also consider the legal requirements and regulations in their jurisdiction. In many places, workers' compensation insurance is mandated by law, regardless of the number of employees or the nature of the work. Failing to comply with these regulations can result in significant penalties and legal consequences.

In addition to legal obligations, employers should also weigh the financial implications of workers' compensation insurance. While the premiums can be costly, the potential costs of medical bills, lost wages, and legal fees in the event of an uninsured workplace injury can be far more substantial. By investing in workers' compensation insurance, employers can protect themselves from financial ruin and ensure that their employees receive the necessary care and support in the event of a work-related injury or illness.

Ultimately, the decision to purchase workers' compensation insurance for a single employee should be based on a careful evaluation of the risks involved, legal requirements, and financial considerations. By taking a proactive approach to risk assessment and insurance coverage, employers can create a safer and more secure work environment for all their employees.

Indiana Churches and Workers' Compensation Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Alternative Options: Explore other insurance types or self-insurance options if applicable

If you're a business owner with a single employee, you may be wondering if workers' compensation insurance is necessary. While it's typically required for businesses with multiple employees, there are alternative options to consider if you only have one employee. One such option is to explore other types of insurance that may provide similar coverage or to consider self-insurance if applicable.

When it comes to alternative insurance types, you may want to look into general liability insurance or business owners' policies. These types of insurance can provide coverage for a variety of risks, including bodily injury and property damage. While they may not offer the same level of coverage as workers' compensation insurance, they can still provide some protection for your business.

Another option to consider is self-insurance, also known as self-funded insurance. This is when a business chooses to pay for each out-of-pocket claim as they are incurred instead of paying a fixed premium to an insurance carrier. Self-insurance can be a viable option for businesses with a low risk of workplace injuries or illnesses, as it can potentially save money on premiums. However, it's important to note that self-insurance also comes with greater financial risk, as the business is responsible for covering all claims.

Before making a decision about alternative insurance options or self-insurance, it's important to carefully evaluate the risks and benefits. Consider factors such as the nature of your business, the likelihood of workplace injuries or illnesses, and your financial resources. It may also be helpful to consult with an insurance professional or a business advisor to discuss your options and make an informed decision.

In conclusion, while workers' compensation insurance is typically required for businesses with multiple employees, there are alternative options to consider if you only have one employee. Exploring other types of insurance or considering self-insurance can provide viable alternatives, but it's important to carefully evaluate the risks and benefits before making a decision.

Seeking Compensation: Health Insurance Broker Negligence Explained

You may want to see also

Frequently asked questions

Yes, in most states, you are required to have workers' compensation insurance even if you have just one employee. This is to ensure that your employee is protected in case of work-related injuries or illnesses.

Some states have exceptions for certain types of businesses or employees. For example, in some states, sole proprietors or partners may not need workers' compensation insurance for themselves, but they would still need it for any other employees they hire. Additionally, some states may have different requirements for certain industries, such as agriculture or domestic work.

The cost of workers' compensation insurance varies depending on factors such as the state you're in, the type of work your employee does, and your company's claims history. On average, the premium for workers' compensation insurance can range from $500 to $2,000 per year for one employee. However, it's important to shop around and get quotes from different insurance providers to find the best rate for your business.