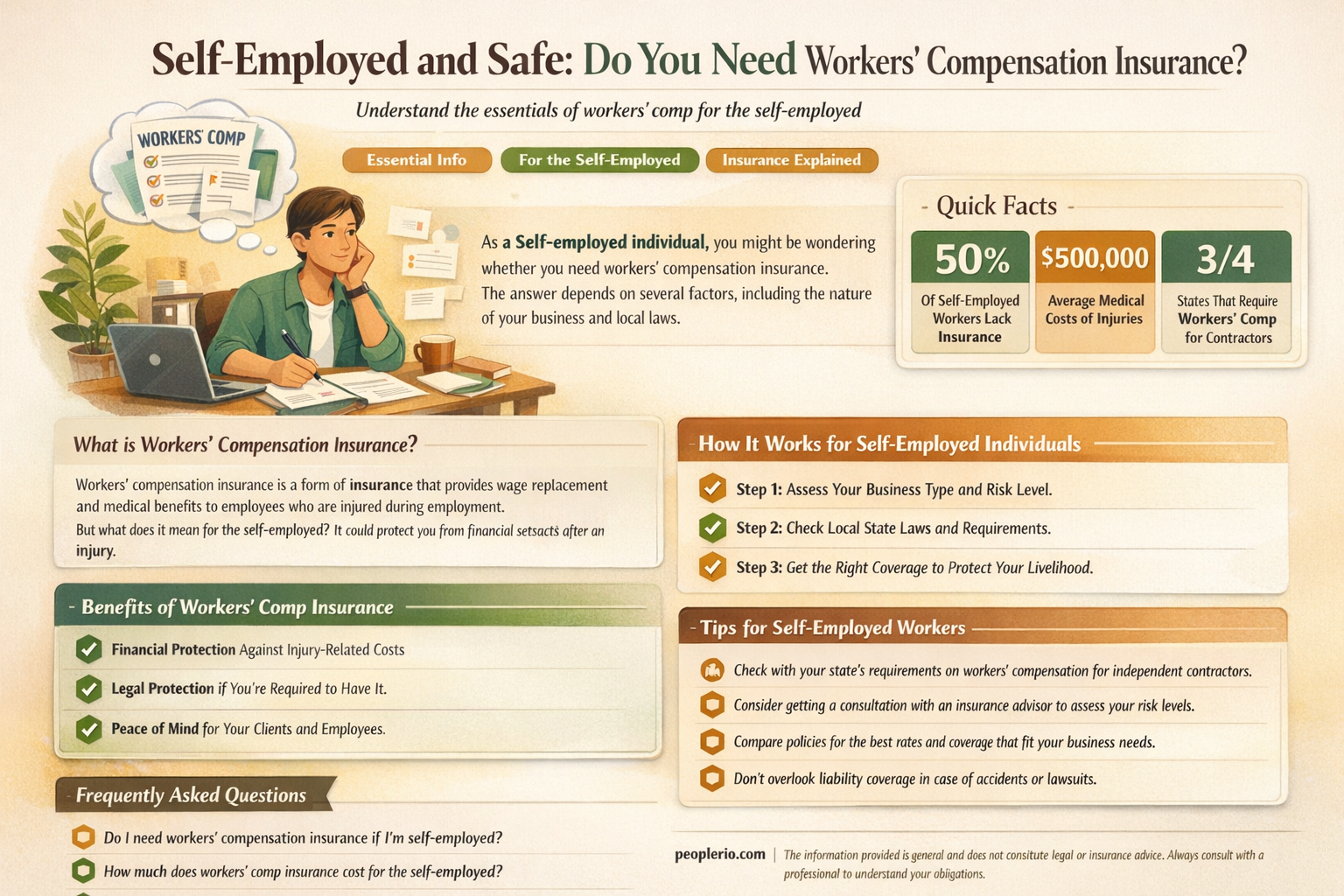

Workers' compensation insurance is a crucial safety net for employees who suffer work-related injuries or illnesses. However, when it comes to the self-employed, the need for this type of insurance isn't always clear-cut. As a self-employed individual, you may not have employees of your own, but you could still be at risk of work-related injuries. In such cases, having workers' compensation insurance can provide you with financial protection and peace of mind. It's important to note that the requirements for workers' compensation insurance vary by state and the nature of your work. Some states may require self-employed individuals in certain high-risk industries to carry this insurance, while others may leave it up to the individual's discretion. Ultimately, it's essential to weigh the potential risks and benefits to determine if workers' compensation insurance is right for you as a self-employed person.

Explore related products

What You'll Learn

- Legal Requirements: Understand state laws regarding workers' compensation insurance for self-employed individuals

- Risk Assessment: Evaluate the risks associated with your self-employment activities and the potential need for coverage

- Types of Coverage: Explore different types of workers' compensation insurance policies available for self-employed workers

- Cost Considerations: Research and compare the costs of various workers' compensation insurance options

- Alternatives to Insurance: Discover alternative risk management strategies if workers' compensation insurance isn't required or feasible

![]()

Legal Requirements: Understand state laws regarding workers' compensation insurance for self-employed individuals

Understanding state laws regarding workers' compensation insurance for self-employed individuals is crucial because regulations vary significantly from one state to another. For instance, some states mandate that all businesses with employees must carry workers' compensation insurance, while others may exempt certain types of businesses or allow for alternative forms of coverage. Self-employed individuals must navigate these complexities to ensure compliance and protect themselves from potential legal and financial repercussions.

To begin, self-employed individuals should research their state's specific requirements by consulting the state's department of labor or insurance commissioner's website. These resources typically provide detailed information on who is required to carry workers' compensation insurance, the types of coverage available, and the consequences of non-compliance. Additionally, self-employed individuals may want to consider consulting with a legal or insurance professional who specializes in workers' compensation to ensure they fully understand their obligations and options.

One unique aspect of workers' compensation insurance for self-employed individuals is the potential for alternative coverage options. In some states, self-employed individuals may be able to opt for a different type of insurance, such as a private disability insurance policy, which can provide similar benefits without the need for a traditional workers' compensation policy. However, it is essential to carefully evaluate these alternatives to ensure they provide adequate coverage and comply with state laws.

Another important consideration is the impact of workers' compensation insurance on business operations. Self-employed individuals must factor in the cost of premiums and the potential for increased administrative burdens when managing a workers' compensation policy. Additionally, they should be aware of the potential for audits or inspections to ensure compliance with state regulations, which can add another layer of complexity to business operations.

In conclusion, understanding state laws regarding workers' compensation insurance for self-employed individuals is a critical aspect of managing a successful business. By researching state-specific requirements, considering alternative coverage options, and factoring in the impact on business operations, self-employed individuals can make informed decisions that protect both themselves and their businesses.

Essential Guide: Workers' Compensation Insurance for Solo Employers

You may want to see also

Explore related products

![]()

Risk Assessment: Evaluate the risks associated with your self-employment activities and the potential need for coverage

As a self-employed individual, it's crucial to conduct a thorough risk assessment to determine the potential hazards associated with your activities. This evaluation will help you identify whether you need workers' compensation insurance. Begin by listing all the tasks and duties you perform regularly, then consider the inherent risks of each. For instance, if you're a construction worker, you might face risks such as falls, equipment malfunctions, or exposure to hazardous materials. Conversely, if you're a graphic designer, your risks might be more related to repetitive strain injuries or eye strain from prolonged screen time.

Once you've identified the risks, assess the likelihood of each occurring and the potential severity of the consequences. This will help you prioritize which risks to address first. For example, a risk with a high likelihood of occurrence and severe consequences should be mitigated immediately. You can use a risk assessment matrix to visualize and categorize these risks effectively.

After prioritizing your risks, research the cost of workers' compensation insurance and compare it to the potential costs of not having coverage. Consider factors such as medical expenses, lost income, and legal fees. If the potential costs of not having coverage outweigh the premiums, it may be wise to invest in workers' compensation insurance.

Additionally, consider the legal requirements in your state or country regarding workers' compensation insurance for self-employed individuals. Some jurisdictions may require certain types of self-employed workers to carry this insurance, while others may not. It's essential to be aware of these regulations to avoid any legal issues.

Finally, consult with a professional, such as an insurance agent or a business advisor, to discuss your specific situation and get tailored advice. They can help you navigate the complexities of workers' compensation insurance and ensure you make an informed decision.

Can Your Employer Cancel Health Insurance During Workers' Comp in California?

You may want to see also

Explore related products

![]()

Types of Coverage: Explore different types of workers' compensation insurance policies available for self-employed workers

Self-employed workers often overlook the importance of workers' compensation insurance, assuming it's only necessary for traditional employees. However, accidents can happen to anyone, and without proper coverage, self-employed individuals may face significant financial risks. Fortunately, there are several types of workers' compensation insurance policies available to protect self-employed workers.

One option is a traditional workers' compensation policy, which provides coverage for medical expenses, lost wages, and other benefits if an employee is injured on the job. Self-employed workers can purchase this type of policy to cover themselves and any employees they may have. Another option is a self-employed workers' compensation policy, which is specifically designed for individuals who work for themselves. This type of policy typically offers similar benefits to a traditional policy but may have different eligibility requirements and premium structures.

Additionally, some self-employed workers may opt for a business owners' policy (BOP), which combines workers' compensation coverage with other types of business insurance, such as liability and property insurance. A BOP can be a cost-effective way for self-employed workers to protect themselves and their business assets. It's essential to note that the specific types of coverage and policies available may vary depending on the state in which the self-employed worker operates.

When selecting a workers' compensation policy, self-employed workers should consider factors such as the level of coverage, the premium cost, and the policy's exclusions and limitations. It's also crucial to understand the claims process and the support available from the insurance provider in the event of an accident. By carefully evaluating these factors, self-employed workers can choose a policy that provides the necessary protection for themselves and their business.

In conclusion, self-employed workers have several options when it comes to workers' compensation insurance. By understanding the different types of policies available and carefully considering their specific needs and circumstances, self-employed individuals can make informed decisions about the coverage that's right for them. This not only helps protect their financial well-being but also ensures they can continue to operate their business with confidence.

Texas Workers' Compensation Insurance: Employer Requirements Explained

You may want to see also

Explore related products

![]()

Cost Considerations: Research and compare the costs of various workers' compensation insurance options

When evaluating workers' compensation insurance options, it's crucial to consider the costs involved. This type of insurance can vary significantly depending on several factors, including the nature of your business, the number of employees you have, and the state in which you operate. To make an informed decision, you should research and compare the costs of various workers' compensation insurance options.

One of the first steps in this process is to understand the different types of workers' compensation insurance policies available. There are several options, including traditional workers' compensation insurance, self-insurance, and captive insurance. Each of these options has its own unique cost structure and benefits. For example, traditional workers' compensation insurance is typically purchased through an insurance carrier and can provide a high level of coverage, but it may also come with higher premiums. Self-insurance, on the other hand, involves setting aside funds to cover potential claims, which can be more cost-effective for larger businesses but may also carry more risk.

Another important factor to consider is the state in which you operate. Workers' compensation insurance requirements and costs can vary significantly from state to state. Some states have state-funded workers' compensation programs, while others require businesses to purchase insurance through private carriers. Additionally, some states have more stringent requirements for workers' compensation coverage, which can impact the cost of insurance.

To effectively compare the costs of different workers' compensation insurance options, it's important to consider not only the premiums but also other factors such as deductibles, coverage limits, and additional fees. You should also evaluate the potential long-term costs associated with each option, such as the impact on your business's financial stability and the potential for future rate increases.

In conclusion, researching and comparing the costs of various workers' compensation insurance options is a critical step in determining the best coverage for your business. By understanding the different types of policies available, the factors that impact costs, and the specific requirements of your state, you can make an informed decision that will help protect your business and your employees.

Understanding Workers' Compensation Insurance Requirements in Illinois

You may want to see also

Explore related products

![]()

Alternatives to Insurance: Discover alternative risk management strategies if workers' compensation insurance isn't required or feasible

If you're self-employed, you may not be required to carry workers' compensation insurance, but that doesn't mean you're immune to work-related injuries or illnesses. In fact, as a sole proprietor, you may be even more vulnerable to financial losses due to unexpected health issues. That's why it's crucial to explore alternative risk management strategies to protect yourself and your business.

One option is to purchase a personal accident insurance policy. This type of coverage can provide financial protection in the event of an accident, regardless of whether it occurs on the job or during your personal time. Another alternative is to invest in a health savings account (HSA) or flexible spending account (FSA), which can help you save money on medical expenses and reduce your taxable income.

Additionally, you may want to consider purchasing a disability insurance policy. This type of coverage can provide income replacement if you're unable to work due to a disability, ensuring that you can continue to support yourself and your family even if you're sidelined by an injury or illness.

It's also important to prioritize workplace safety and ergonomics to minimize the risk of accidents and injuries. This may involve investing in ergonomic equipment, such as a comfortable chair and desk setup, as well as implementing safety protocols, like wearing protective gear when necessary.

Finally, consider diversifying your income streams to reduce your reliance on a single source of revenue. This can help mitigate the financial impact of an unexpected injury or illness, as you'll have other sources of income to fall back on.

Remember, while workers' compensation insurance may not be required for self-employed individuals, it's still essential to have a plan in place to manage risks and protect your financial well-being. By exploring these alternative strategies, you can create a safety net that will help you navigate unexpected challenges and continue to thrive in your self-employed career.

Missouri Workers' Comp Insurance: A Must for Contractors?

You may want to see also

Frequently asked questions

It depends on the laws of your state and the nature of your work. Some states require all businesses, including sole proprietors, to carry workers' compensation insurance, while others may exempt self-employed individuals without employees.

If you don't have workers' compensation insurance and you get injured while working, you may be personally liable for your medical expenses and lost wages. This could lead to significant financial hardship.

The cost of workers' compensation insurance for self-employed individuals varies depending on factors such as your occupation, your income, and the state you work in. It's best to get quotes from multiple insurance providers to find the most affordable option.

Yes, freelancers and independent contractors can purchase workers' compensation insurance. This can help protect you from financial losses if you're injured while working on a project.

Some alternatives to workers' compensation insurance for self-employed individuals include disability insurance, health insurance, and personal liability insurance. These types of insurance can help cover your medical expenses and lost wages if you're injured or unable to work.