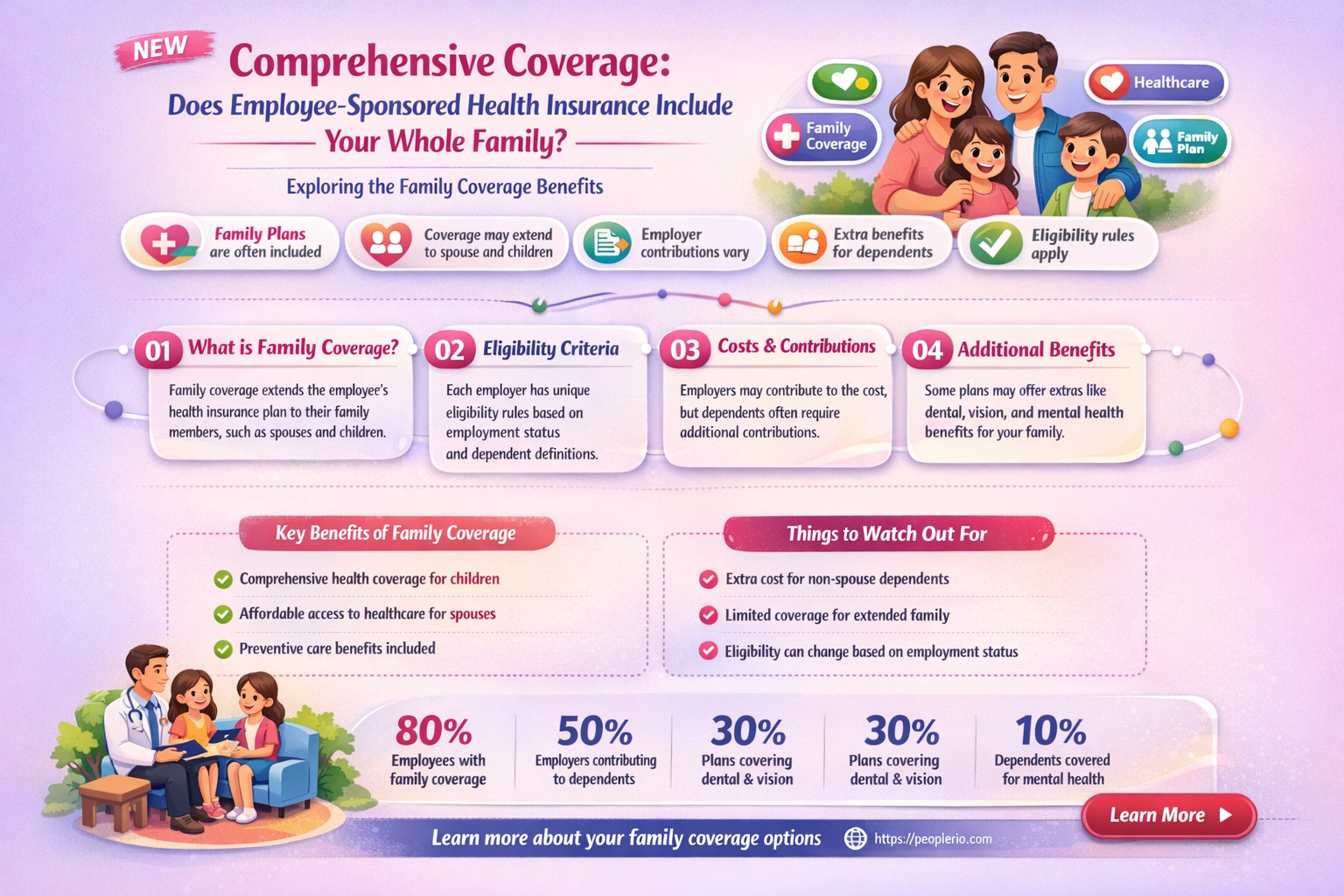

Employee-sponsored health insurance is a common benefit provided by many employers, offering financial protection against medical expenses. However, understanding the specifics of such coverage can be complex. One key question that arises is whether this insurance extends to the entire family of the employee. Typically, employee-sponsored plans do offer the option to cover dependents, which usually include spouses and children. The extent of this coverage, though, can vary significantly based on the employer's policy, the insurance provider, and the specific plan chosen. Some plans may cover only the employee, while others might include comprehensive family coverage. It's also important to consider the cost implications, as adding family members to an employee's plan can substantially increase premiums. Therefore, it's crucial for employees to carefully review their plan's details and consult with their employer or insurance provider to fully understand the coverage options available to them and their families.

| Characteristics | Values |

|---|---|

| Coverage Scope | Typically covers the employee and their dependents, including spouse and children |

| Cost Sharing | Employee may need to contribute a portion of the premium, copays, and deductibles |

| Network Providers | Access to a specific network of healthcare providers |

| Prescription Coverage | Often includes prescription drug coverage |

| Dental and Vision | May include dental and vision care, but not always |

| Pre-existing Conditions | Coverage for pre-existing conditions may vary |

| Waiting Period | Some plans have a waiting period before coverage begins |

| Annual Limits | May have annual limits on certain types of care |

| Coordination of Benefits | If multiple insurances are held, coordination of benefits will determine which plan pays first |

| Tax Implications | Premiums paid by the employer are generally tax-deductible for the employer and tax-free for the employee |

Explore related products

What You'll Learn

- Eligibility Criteria: Define who qualifies as family members under employee-sponsored health insurance plans

- Coverage Levels: Explore the extent of coverage provided for family members, including any limitations or exclusions

- Cost Implications: Discuss the financial aspects, such as premiums, deductibles, and out-of-pocket expenses for family coverage

- Plan Types: Compare different types of plans (e.g., HMO, PPO) and their implications for family health insurance

- Enrollment Process: Outline the steps required to enroll family members in an employee-sponsored health insurance plan

![]()

Eligibility Criteria: Define who qualifies as family members under employee-sponsored health insurance plans

Employee-sponsored health insurance plans often provide coverage for family members, but the definition of "family" can vary significantly from one plan to another. Typically, these plans consider the following individuals as eligible family members: spouses, domestic partners, children (including adopted and stepchildren), and sometimes parents or grandparents. However, the specifics can get quite detailed.

For instance, some plans may require that children be under a certain age, such as 26, to qualify for coverage, while others might extend this benefit to adult children if they are still dependents. Similarly, the definition of a domestic partner can differ, with some plans requiring a formal domestic partnership agreement or proof of a long-term relationship.

It's also important to note that some plans may have restrictions on covering family members with pre-existing conditions or may require additional premiums for such coverage. Furthermore, the process of adding or removing family members from an employee-sponsored plan usually involves specific enrollment periods or qualifying events, such as marriage, birth, or adoption.

To fully understand who qualifies as a family member under an employee-sponsored health insurance plan, it's crucial to review the plan's detailed eligibility criteria and consult with the plan administrator or a human resources representative if there are any questions or uncertainties.

Unlocking Educational Opportunities: Advent Health's Tuition Reimbursement Program

You may want to see also

Explore related products

![]()

Coverage Levels: Explore the extent of coverage provided for family members, including any limitations or exclusions

Employee-sponsored health insurance plans often provide coverage for family members, but the extent of this coverage can vary significantly. Typically, these plans cover spouses and dependent children, but there may be limitations or exclusions based on factors such as age, marital status, or employment status of the family members. For instance, some plans may only cover children up to a certain age, or may require that spouses be financially dependent on the employee.

It's important to carefully review the details of your employee-sponsored health insurance plan to understand the specific coverage levels for your family members. This includes understanding any limitations or exclusions that may apply, as well as any additional costs or premiums that may be required for family coverage. By doing so, you can ensure that you and your family have the appropriate level of health insurance coverage.

When exploring the extent of coverage provided for family members, it's also important to consider any potential changes in your family's circumstances that could impact your coverage. For example, if you have a child who is approaching the age limit for coverage, or if your spouse is considering returning to work, it's important to understand how these changes could affect your health insurance plan.

In addition to understanding the coverage levels for your family members, it's also important to consider the quality of the coverage provided. This includes factors such as the network of healthcare providers, the types of services covered, and the out-of-pocket costs associated with the plan. By evaluating these factors, you can determine whether the employee-sponsored health insurance plan is the best option for your family's healthcare needs.

Ultimately, the key to ensuring that your family has the appropriate level of health insurance coverage is to carefully review and understand the details of your employee-sponsored health insurance plan. This includes exploring the extent of coverage provided for family members, understanding any limitations or exclusions, and considering any potential changes in your family's circumstances that could impact your coverage. By doing so, you can make informed decisions about your family's healthcare and ensure that you have the protection you need.

Understanding 1099 Forms: Do They Cover Employee Health Care Expenses?

You may want to see also

Explore related products

![]()

Cost Implications: Discuss the financial aspects, such as premiums, deductibles, and out-of-pocket expenses for family coverage

The cost implications of employee-sponsored health insurance for family coverage can be significant. Premiums, which are the monthly payments made to maintain the insurance policy, can vary widely depending on the plan chosen and the employer's contribution. On average, employers cover about 80% of the premium cost for family plans, leaving the employee to pay the remaining 20%. However, this can still amount to a substantial monthly expense, especially for higher-tier plans that offer more comprehensive coverage.

Deductibles, which are the amounts paid out-of-pocket before the insurance coverage kicks in, are another important cost consideration. Family plans often have higher deductibles than individual plans, which can make it more challenging for families to afford necessary medical care. Additionally, out-of-pocket expenses, such as copays and coinsurance, can add up quickly, especially for families with multiple members who require regular medical attention.

One way to mitigate these costs is to carefully compare different insurance plans during the open enrollment period. Employees should consider their family's specific healthcare needs and budget when selecting a plan. For example, a plan with a lower premium but higher deductible might be more cost-effective for a family that does not anticipate many medical expenses, while a plan with a higher premium but lower deductible might be more suitable for a family with ongoing healthcare needs.

Another strategy for managing costs is to take advantage of tax-saving opportunities, such as Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs). These accounts allow employees to set aside pre-tax dollars for qualified medical expenses, which can help reduce their overall healthcare costs. Additionally, employees should be aware of any wellness programs or preventive care benefits offered by their employer, as these can help reduce healthcare costs in the long run by promoting healthier lifestyles and early intervention for potential health issues.

In conclusion, while employee-sponsored health insurance can provide valuable coverage for families, it is important to carefully consider the cost implications and explore strategies for managing these expenses. By comparing plans, taking advantage of tax-saving opportunities, and utilizing wellness programs, employees can help ensure that their families have access to affordable, high-quality healthcare.

Understanding HIPAA: Protecting Employee Health Records in the Workplace

You may want to see also

Explore related products

![]()

Plan Types: Compare different types of plans (e.g., HMO, PPO) and their implications for family health insurance

Health Maintenance Organizations (HMOs) and Preferred Provider Organizations (PPOs) are two common types of health insurance plans that families may consider when seeking coverage. HMOs typically require members to choose a primary care physician (PCP) and to receive care within a specific network of providers. This can lead to lower out-of-pocket costs for in-network care, but may also limit the flexibility to see specialists or receive care outside of the network.

In contrast, PPOs offer more flexibility in terms of provider choice, allowing members to see any licensed healthcare provider without the need for a referral from a PCP. However, this flexibility often comes at a higher cost, as PPOs may have higher premiums and out-of-pocket costs for out-of-network care.

When considering the implications of these plan types for family health insurance, it is important to weigh the potential benefits and drawbacks of each option. For families with young children or members with chronic health conditions, the predictability and lower costs of an HMO may be more appealing. On the other hand, families with members who require specialized care or who frequently travel may benefit from the flexibility of a PPO.

Ultimately, the choice between an HMO and a PPO will depend on the specific needs and preferences of the family. It is important to carefully review the details of each plan, including the provider network, coverage limitations, and out-of-pocket costs, before making a decision. By understanding the differences between these plan types, families can make an informed choice that best meets their healthcare needs and budget.

Understanding the Tax Implications of Employee Health Insurance Deductions

You may want to see also

Explore related products

$3.99

![Employee benefits survey : an MLR reader / U.S. Dept. of Labor, Bureau of Labor Statistics. 1990 [Leather Bound]](https://m.media-amazon.com/images/I/61IX47b4r9L._AC_UY218_.jpg)

![]()

Enrollment Process: Outline the steps required to enroll family members in an employee-sponsored health insurance plan

To enroll family members in an employee-sponsored health insurance plan, you must first gather the necessary information. This includes the names, dates of birth, and social security numbers of all family members you wish to enroll. You will also need to know the specific plan you are enrolling in, as different plans may have different enrollment requirements.

Once you have gathered the necessary information, you will need to fill out an enrollment form. This form will typically be provided by your employer's human resources department. Be sure to fill out the form completely and accurately, as any errors or omissions could delay the enrollment process.

After you have filled out the enrollment form, you will need to submit it to your employer's human resources department. This can typically be done online, by mail, or in person. Be sure to submit the form by the deadline specified by your employer, as late submissions may not be accepted.

Once your enrollment form has been submitted, you will need to wait for confirmation from your employer's human resources department. This confirmation will typically be sent to you via email or mail, and will include information about the effective date of your family members' coverage.

In some cases, you may be required to provide additional documentation to support your enrollment. This could include proof of marriage, birth certificates, or other relevant documents. Be sure to provide these documents promptly to avoid any delays in the enrollment process.

Finally, be sure to review your family members' coverage regularly to ensure that it remains up-to-date and accurate. This includes updating your employer's human resources department of any changes in your family's status, such as births, deaths, or changes in employment. By keeping your coverage up-to-date, you can ensure that your family members have the protection they need in the event of an unexpected illness or injury.

Unveiling the Truth: Are Employee Health Incentive Programs Truly Confidential?

You may want to see also

Frequently asked questions

Yes, many employee-sponsored health insurance plans offer coverage for the employee's spouse and dependent children. However, the specifics can vary depending on the plan and the employer's policies.

Dependents usually include the employee's spouse and children who are under a certain age, often 26, unless they are disabled. Some plans may also cover domestic partners and stepchildren, but this varies by plan and employer.

The cost of adding family members can vary significantly. Some employers may cover a portion of the premiums for family members, while others may require the employee to pay the full premium. It's important to review the plan details and consult with the employer's benefits administrator.

Generally, an employee can choose to exclude their spouse or children from their plan during the initial enrollment period or during open enrollment periods. However, they may not be able to add them back until the next open enrollment period, unless there is a qualifying life event, such as marriage, birth, or loss of other coverage.