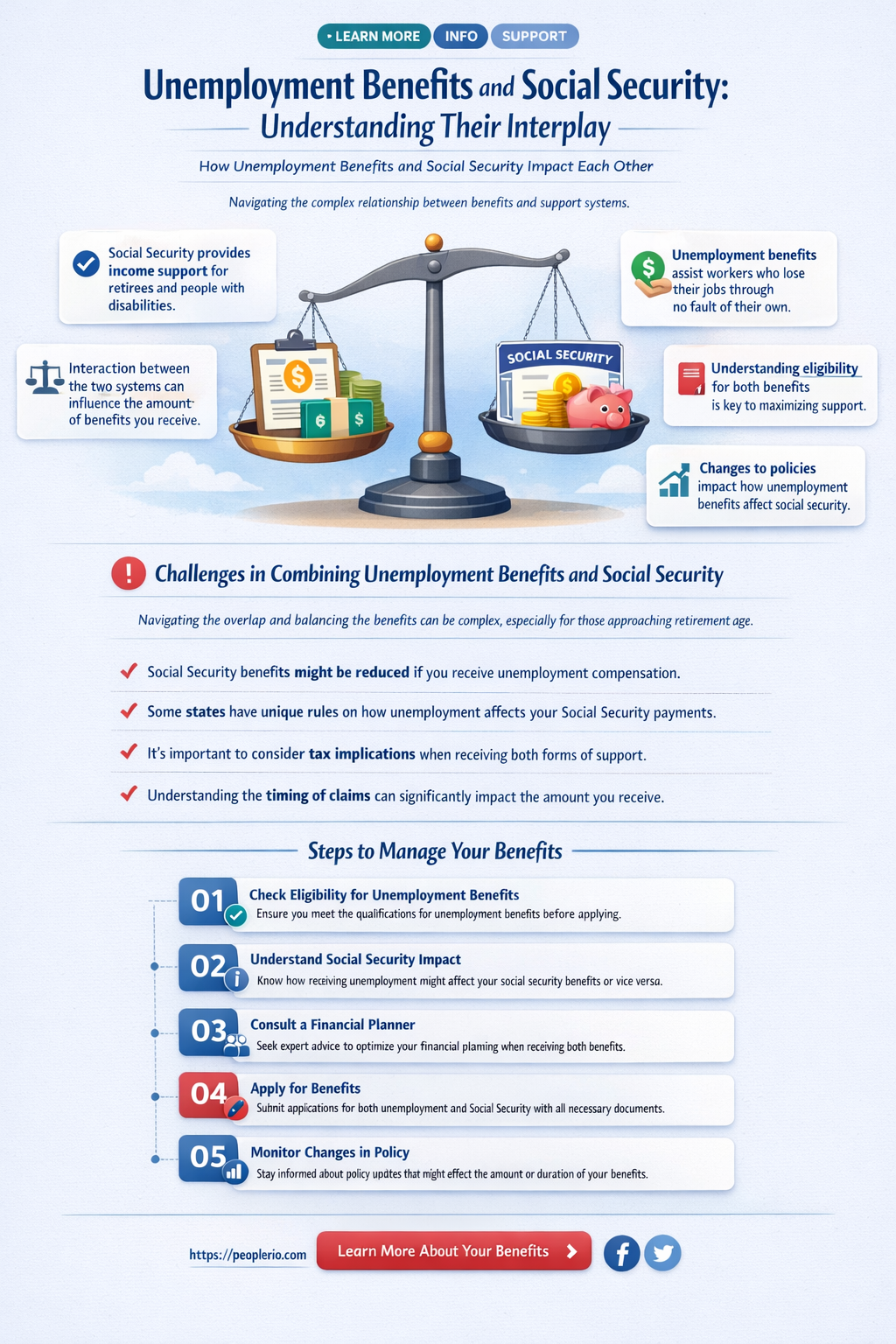

Unemployment compensation and Social Security are two distinct but interconnected components of the U.S. social safety net, and understanding how they interact is crucial for individuals planning their financial futures. While unemployment benefits provide temporary financial assistance to those who lose their jobs through no fault of their own, Social Security offers long-term retirement, disability, and survivor benefits. A common question arises regarding whether receiving unemployment compensation impacts Social Security benefits, particularly in terms of eligibility, benefit amounts, or taxation. Generally, unemployment benefits do not directly reduce Social Security retirement benefits, as they are funded through different payroll taxes and calculated using separate formulas. However, unemployment compensation is considered taxable income, which could potentially increase an individual’s combined income, thereby affecting the taxation of their Social Security benefits. Additionally, extended periods of unemployment might reduce an individual’s lifetime earnings, which could indirectly lower their Social Security benefit amount, as benefits are based on the highest 35 years of earnings. Thus, while there is no direct link between the two programs, the interplay of income, taxation, and earnings history highlights the importance of understanding how unemployment compensation might indirectly influence Social Security benefits.

Explore related products

What You'll Learn

![]()

Impact on Social Security Benefits Calculation

Unemployment compensation, a vital safety net for those between jobs, does not directly reduce Social Security benefits. This is a critical distinction for anyone navigating the complexities of retirement planning. Social Security benefits are calculated based on your highest 35 years of earnings, adjusted for inflation. Unemployment benefits, being temporary and often lower than regular wages, do not factor into this calculation. However, the interplay between these two systems can still influence your financial strategy.

Consider the timing of claiming Social Security benefits. If you’re receiving unemployment compensation, you might be tempted to delay claiming Social Security to maximize your monthly benefit. Social Security benefits increase by about 8% annually if delayed past full retirement age (currently 66 or 67, depending on birth year) up to age 70. For example, if your full retirement age is 67 and you delay until 70, your benefit could be 24% higher. Unemployment compensation can provide a temporary income bridge, allowing you to strategically delay Social Security and secure a higher benefit later.

However, there’s a cautionary note. While unemployment benefits don’t directly affect Social Security calculations, they can impact your overall tax situation. Unemployment compensation is taxable income, and if it pushes you into a higher tax bracket, it could increase the taxes you owe on your Social Security benefits. Up to 85% of Social Security benefits may be taxable if your combined income (adjusted gross income + nontaxable interest + half of Social Security benefits) exceeds certain thresholds: $25,000 for single filers and $32,000 for married couples filing jointly. Planning around these thresholds can help minimize tax liabilities.

Another practical consideration is the impact of part-time work while receiving unemployment benefits. If you take a part-time job, your unemployment compensation may be reduced, but this income could still be factored into your Social Security earnings record if it’s substantial enough to count toward your 35 highest-earning years. For 2023, earnings above $1,780 in a month (or $21,360 annually) are considered substantial and could improve your Social Security benefit calculation. Balancing part-time work with unemployment benefits requires careful planning to maximize both short-term income and long-term Social Security benefits.

In summary, while unemployment compensation doesn’t directly affect Social Security benefit calculations, it can influence your overall financial strategy. Delaying Social Security claims, managing tax implications, and strategically balancing part-time work are actionable steps to optimize both benefits. Understanding these nuances ensures you make informed decisions that align with your retirement goals.

Georgia Unemployment Compensation: Understanding Your Weekly Benefit Amount

You may want to see also

Explore related products

![]()

Eligibility Changes for Early Retirement Benefits

Unemployment compensation, often a lifeline during job transitions, can subtly influence your Social Security benefits, particularly if you’re considering early retirement. The interplay between these two systems hinges on timing, income thresholds, and eligibility rules. For those eyeing early retirement benefits, understanding how unemployment compensation affects your financial landscape is critical. Here’s a focused guide to navigating these changes.

Example & Analysis: Consider a 62-year-old worker who claims unemployment benefits while contemplating early Social Security retirement benefits. If they earn above the annual earnings limit ($21,240 in 2023) while receiving unemployment, their Social Security benefits may be temporarily reduced. For every $2 earned above this limit, $1 is withheld from their Social Security payments. However, unemployment compensation itself is not counted as earnings for this calculation. The key takeaway? Timing matters. Claiming unemployment benefits in the same year as early retirement could inadvertently trigger benefit reductions if other earned income pushes you over the threshold.

Practical Steps: To avoid unintended penalties, coordinate your claims strategically. First, calculate your total earned income, excluding unemployment benefits, to ensure it stays below the annual limit. Second, delay claiming Social Security retirement benefits until you’re no longer receiving unemployment compensation, especially if you’re still in the workforce part-time. Third, consult the Social Security Administration’s earnings test rules to understand how your specific income sources interact with early retirement benefits.

Cautions: Be wary of the “trial work period” misconception. While this term applies to disability benefits, early retirees often confuse it with their situation. Unemployment compensation does not trigger a trial work period for retirement benefits, but it can still impact your overall financial planning. Additionally, state-specific unemployment rules may vary, so verify how your state handles benefit calculations and reporting.

Is Unemployment Compensation Included in GDP Calculations?

You may want to see also

Explore related products

![]()

Effect on Disability Insurance Claims

Unemployment compensation can indirectly influence disability insurance claims by altering an individual’s financial behavior and eligibility considerations. When someone receives unemployment benefits, they may delay filing for disability insurance (DI) because the immediate income from unemployment provides temporary financial relief. This delay can be strategic, as applicants often wait to see if their health improves or if they can return to work. However, prolonged reliance on unemployment benefits may exhaust other resources, leaving DI as the only remaining option, which can lead to a surge in claims once unemployment benefits expire.

Consider the interplay between these programs in the context of eligibility. Unemployment compensation is designed for those actively seeking work, while disability insurance requires proof of inability to work due to a medical condition. If an individual files for both simultaneously, it could raise red flags with the Social Security Administration (SSA). For example, claiming unemployment might suggest the applicant is capable of work, potentially jeopardizing their DI claim. To avoid this, applicants should consult legal or financial advisors to ensure their claims align with program requirements and do not inadvertently disqualify them from DI benefits.

A practical tip for those navigating this situation is to document all medical evidence thoroughly before filing for DI. This includes medical records, treatment plans, and physician statements confirming the inability to work. If unemployment benefits are claimed first, applicants should be prepared to explain the transition from seeking work to being unable to work due to disability. Timing is critical—filing for DI too soon after receiving unemployment benefits may trigger scrutiny, while waiting too long can strain finances. A well-timed, evidence-backed application can mitigate these risks.

Comparatively, the impact of unemployment compensation on DI claims varies by age and occupation. Younger workers may view unemployment as a temporary bridge while exploring job options, delaying DI claims. Older workers, especially those nearing retirement age, might transition directly from unemployment to DI if their health deteriorates. For instance, a 55-year-old construction worker with a chronic back injury might exhaust unemployment benefits before filing for DI, whereas a 30-year-old office worker with a temporary injury might prioritize unemployment while recovering. Understanding these demographic differences can help tailor strategies for maximizing benefits.

In conclusion, while unemployment compensation does not directly affect disability insurance claims, its influence on financial decisions and eligibility perceptions can significantly shape the timing and success of DI applications. By strategically managing the transition between programs, documenting medical evidence, and considering age- and occupation-specific factors, individuals can navigate this complex landscape more effectively. Proactive planning and informed decision-making are key to securing the support needed during challenging times.

Can Unemployment Benefits Be Garnished? Understanding Legal Limits and Protections

You may want to see also

Explore related products

![]()

Reduction in Overall Social Security Payouts

Unemployment compensation, while a vital safety net for those between jobs, can inadvertently trigger a reduction in overall Social Security payouts for certain individuals. This occurs primarily through the Social Security Administration's (SSA) Windfall Elimination Provision (WEP) and Government Pension Offset (GPO) rules, which aim to adjust benefits for those who receive pensions from jobs not covered by Social Security. For example, a teacher who worked in a public school system not covered by Social Security and later collects unemployment benefits may see their Social Security payments reduced if they also qualify for a pension from that job.

The WEP specifically targets individuals who have split their careers between jobs covered by Social Security and those that are not. If you have fewer than 30 years of substantial earnings under Social Security, your benefit formula is adjusted downward, resulting in a lower monthly payout. For instance, in 2023, the maximum monthly reduction under WEP is $521, but the actual reduction depends on your lifetime earnings record. To mitigate this, workers should aim to accumulate at least 30 years of substantial earnings under Social Security, as each additional year of covered employment reduces the WEP penalty.

The GPO, on the other hand, affects spousal and survivor benefits. If you receive a pension from a job not covered by Social Security, your spousal or survivor benefit may be reduced by two-thirds of your pension amount. For example, if your monthly pension is $600, your spousal benefit could be reduced by $400. This rule disproportionately impacts public sector workers, such as teachers or firefighters, who often rely on non-Social Security pensions. To plan ahead, individuals in such careers should consult a financial advisor to understand how their pension and unemployment benefits might interact with Social Security.

Practical steps to minimize these reductions include delaying Social Security claims until full retirement age or later, as this can increase monthly benefits. Additionally, individuals should carefully review their earnings history on their Social Security statement to ensure accuracy, as errors can exacerbate WEP penalties. For those nearing retirement, consider using online calculators provided by the SSA to estimate potential reductions and adjust retirement plans accordingly.

In conclusion, while unemployment compensation itself does not directly reduce Social Security payouts, its interaction with pensions from non-covered employment can lead to significant benefit reductions. Understanding the WEP and GPO rules, planning for substantial earnings under Social Security, and seeking professional advice are essential strategies to protect your retirement income. By taking proactive steps, individuals can navigate these complexities and secure a more stable financial future.

Where to Report Unemployment Compensation on Your 1040 Form

You may want to see also

Explore related products

![]()

Unemployment Duration and Benefit Adjustments

The duration of unemployment significantly influences the interplay between unemployment compensation and social security benefits, particularly for individuals nearing retirement age. Extended periods of unemployment can lead to reduced Social Security benefits because fewer years of earnings are factored into the benefit calculation. Social Security benefits are based on the highest 35 years of earnings, adjusted for inflation. If unemployment results in gaps in earnings history, lower-income years may be included, thereby decreasing the average indexed monthly earnings (AIME) used to determine benefit amounts. For example, someone who experiences two years of unemployment in their late 50s might see their Social Security benefit reduced by several hundred dollars per month upon retirement.

To mitigate this impact, individuals should strategically plan their unemployment benefit claims, especially if they are within a decade of retirement. One practical tip is to exhaust other financial resources, such as savings or part-time work, before tapping into unemployment benefits. This approach preserves higher-earning years in the Social Security calculation. Additionally, delaying Social Security claims beyond the minimum eligibility age of 62 can increase monthly benefits, offsetting some of the losses from unemployment-related earnings gaps. For instance, delaying benefits until age 70 can result in a 32% higher monthly payout compared to claiming at 62.

A comparative analysis reveals that younger workers have more time to recover from the financial impact of unemployment on Social Security benefits. For individuals in their 30s or 40s, a year or two of unemployment may have minimal long-term effects if they return to the workforce and maintain consistent earnings afterward. However, older workers, particularly those aged 55 and above, face greater challenges due to limited time to rebuild their earnings history. For this demographic, unemployment compensation should be viewed as a short-term bridge rather than a long-term solution, with a focus on retraining or finding employment quickly to minimize Social Security penalties.

Finally, it’s crucial to understand how state-specific unemployment benefit rules interact with Social Security planning. Some states offer more generous unemployment benefits, which can provide a financial cushion but may inadvertently discourage swift re-employment. Individuals should weigh the immediate benefits of unemployment compensation against the long-term implications for Social Security. Consulting a financial advisor or using online calculators to model different scenarios can help tailor strategies to individual circumstances, ensuring that short-term unemployment does not disproportionately affect retirement income.

Unemployment Benefits After Workers' Comp: What You Need to Know

You may want to see also

Frequently asked questions

No, unemployment compensation does not directly reduce your Social Security retirement benefits. They are separate programs, and receiving unemployment does not impact the amount of your Social Security retirement payments.

Unemployment compensation generally does not affect SSDI benefits, as they are different programs with distinct eligibility criteria. However, receiving unemployment may complicate your SSDI claim if it suggests you are able to work.

Yes, unemployment compensation is considered taxable income and is subject to federal income tax. It is also included in the calculation of Social Security taxes, as it is reported to the IRS.

No, receiving unemployment compensation does not delay your eligibility for Social Security retirement benefits. Your eligibility is based on your age and work history, not on whether you receive unemployment.

Unemployment compensation does not directly impact the amount of your future Social Security benefits. Your Social Security benefits are calculated based on your lifetime earnings from work covered by Social Security, not from unemployment benefits.