Unemployment compensation, often referred to as unemployment benefits, is a critical financial safety net provided to individuals who have lost their jobs through no fault of their own. A common question that arises is whether unemployment compensation qualifies as earned income. Earned income typically refers to money received in exchange for work or services performed, such as wages, salaries, or tips. However, unemployment benefits are generally considered a form of unearned income because they are not directly tied to current employment or active labor. Instead, they are funded by payroll taxes paid by employers and are designed to provide temporary financial assistance to eligible workers during periods of unemployment. Understanding the classification of unemployment compensation as unearned income is essential for tax purposes, eligibility for certain government programs, and financial planning during job transitions.

| Characteristics | Values |

|---|---|

| Is unemployment compensation considered earned income for federal tax purposes? | No |

| Reasoning | Unemployment compensation is not considered earned income because it is not received in exchange for services performed. It is a form of government assistance. |

| Tax Treatment | Unemployment compensation is taxable as ordinary income at the federal level. |

| Impact on Tax Credits | Since it's not earned income, unemployment compensation does not qualify for certain tax credits like the Earned Income Tax Credit (EITC). |

| State Tax Treatment | Varies by state; some states may tax unemployment compensation, while others may not. |

| Social Security and Medicare Taxes | Unemployment compensation is not subject to Social Security and Medicare taxes. |

| Reporting on Tax Returns | Reported on Form 1099-G and entered on line 7 of Form 1040 or Form 1040-SR. |

| Withholding Option | Taxpayers can choose to have federal taxes withheld from their unemployment compensation payments. |

| Latest IRS Guidance | As of the latest IRS guidance (2023), unemployment compensation remains taxable and not considered earned income. |

Explore related products

$5.99 $11.99

What You'll Learn

![]()

Definition of earned income

Earned income, at its core, refers to compensation received in exchange for labor or services rendered. This includes wages, salaries, tips, and self-employment income. The Internal Revenue Service (IRS) defines earned income as income derived from active participation in a trade or business, making it a critical distinction for tax purposes. For instance, a freelance graphic designer’s project fees qualify as earned income because they are directly tied to their work. In contrast, passive income, such as dividends or rental income, does not meet this definition. Understanding this distinction is essential when evaluating whether unemployment compensation falls into the earned income category.

Unemployment compensation, provided by state or federal programs, serves as a financial safety net for individuals who lose their jobs through no fault of their own. While it replaces a portion of lost wages, it is not considered earned income under IRS guidelines. This is because unemployment benefits are not tied to current labor or services but rather to previous employment history and contributions to unemployment insurance. For example, a laid-off factory worker receiving unemployment benefits is not actively earning those funds through ongoing work. This classification has significant implications for tax filings and eligibility for certain tax credits, such as the Earned Income Tax Credit (EITC), which explicitly excludes unemployment compensation.

From a practical standpoint, distinguishing earned income from other forms of income is crucial for financial planning. For individuals relying on unemployment benefits, recognizing that these payments are not earned income helps in accurately reporting taxes and managing expectations regarding deductions and credits. For instance, a single parent earning $15,000 annually from part-time work and receiving $5,000 in unemployment benefits would only report the $15,000 as earned income on their tax return. This clarity ensures compliance with tax laws and avoids potential penalties for misreporting.

Comparatively, earned income and unemployment compensation serve different purposes in an individual’s financial landscape. Earned income reflects current productivity and is subject to payroll taxes, while unemployment compensation is a temporary support mechanism funded by employer contributions and, in some cases, employee taxes. This distinction highlights why unemployment benefits are treated differently in tax calculations. For example, while earned income may qualify for retirement account contributions, unemployment compensation does not. Understanding these differences empowers individuals to make informed decisions about budgeting, tax planning, and long-term financial strategies.

In conclusion, the definition of earned income hinges on the direct exchange of labor for compensation, a criterion unemployment benefits do not meet. This clear distinction impacts tax obligations, eligibility for certain credits, and overall financial planning. By recognizing the unique nature of unemployment compensation, individuals can navigate their financial situations more effectively, ensuring accuracy in tax reporting and maximizing available resources during periods of joblessness.

Unemployment Benefits After Workers' Comp: What You Need to Know

You may want to see also

Explore related products

![]()

Unemployment compensation eligibility

Unemployment compensation, often referred to as unemployment insurance (UI), is a critical safety net for workers who lose their jobs through no fault of their own. However, eligibility for these benefits is not automatic and hinges on specific criteria that vary by state. To qualify, individuals must meet three primary requirements: they must have earned a minimum amount of wages during a defined base period, typically the first four of the last five completed calendar quarters before filing the claim; they must be unemployed due to reasons beyond their control, such as layoffs or company closures; and they must be actively seeking new employment. Failing to meet any of these criteria can result in denial of benefits, making it essential for claimants to understand their state’s specific rules.

The process of determining eligibility begins with the base period, a 12-month timeframe used to calculate earnings. For example, if a claim is filed in October 2023, the base period would likely be from October 2022 to September 2023. States require a minimum earnings threshold during this period, which varies widely. In California, for instance, claimants must have earned at least $1,300 in one quarter of the base period, plus additional amounts based on total earnings. In contrast, Florida requires a minimum of $3,400 in the entire base period. Understanding these thresholds is crucial, as insufficient earnings will disqualify an applicant regardless of their employment history.

Another critical factor is the reason for unemployment. Benefits are generally denied if an individual quits voluntarily without good cause or is terminated for misconduct. However, "good cause" is broadly interpreted and can include unsafe working conditions, significant changes in job duties, or family-related reasons. For example, a worker who leaves a job due to a sudden relocation of a spouse may still qualify. Conversely, being fired for chronic tardiness or insubordination typically disqualifies an individual. Documentation, such as termination letters or witness statements, can be pivotal in proving eligibility in disputed cases.

Active job search requirements further complicate eligibility, as claimants must demonstrate consistent efforts to find new employment. This typically involves applying to a minimum number of jobs weekly, often two to three, and keeping detailed records of these efforts. Some states, like Texas, require claimants to register with their workforce commission and accept suitable job offers. Failure to comply can lead to benefit suspension. Practical tips include using job search platforms like Indeed or LinkedIn, attending career fairs, and leveraging local workforce centers for assistance. Maintaining a log of applications, interviews, and employer contacts is essential to avoid disputes.

Finally, eligibility is not permanent and must be recertified weekly or biweekly, depending on the state. Claimants must report any earnings from part-time or temporary work, as these can reduce benefit amounts. For example, in New York, earnings over $50 per week are deducted dollar-for-dollar from the benefit payment. Additionally, claimants must remain able and available to work, meaning they cannot turn down suitable job offers without valid reasons. Understanding these ongoing requirements ensures uninterrupted benefits and avoids potential overpayment penalties. By navigating these complexities, eligible individuals can maximize their financial support during periods of unemployment.

Where to Report Unemployment Compensation on Your 1040 Form

You may want to see also

Explore related products

![]()

Tax implications of benefits

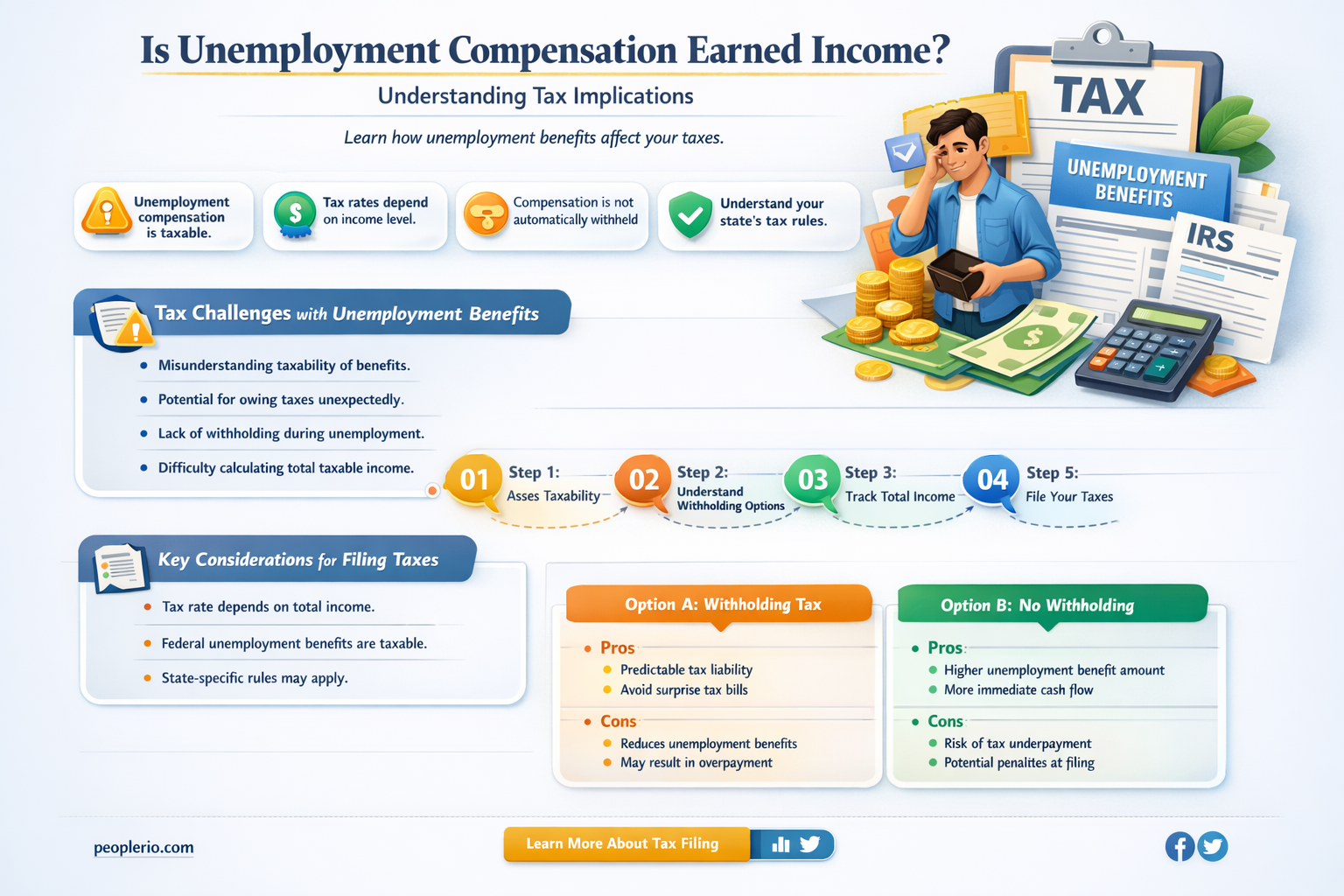

Unemployment compensation, often a financial lifeline during job transitions, carries significant tax implications that recipients must navigate carefully. Unlike traditional wages, unemployment benefits are generally considered taxable income at the federal level, meaning they must be reported on your annual tax return. This classification stems from the Internal Revenue Service (IRS) view that such benefits replace lost wages, thus qualifying as earned income for tax purposes. However, the treatment at the state level varies widely, with some states exempting unemployment compensation from taxation entirely, while others align with federal rules or impose their own tax rates.

For taxpayers, understanding these distinctions is crucial for accurate reporting and avoiding penalties. If you receive unemployment benefits, the paying agency should provide you with Form 1099-G, which details the total amount paid during the tax year. This form is essential for completing your tax return, as it ensures you report the correct amount of taxable income. Failure to include this information can result in audits or additional taxes owed, along with potential interest and penalties.

One practical tip for managing the tax impact of unemployment benefits is to opt for federal tax withholding at the time of payment. By completing Form W-4V, you can request that federal income tax be deducted from your benefits, reducing the likelihood of a large tax bill at year-end. This proactive approach is particularly beneficial for individuals who anticipate difficulty saving for tax obligations. Additionally, consulting a tax professional can provide tailored advice based on your specific financial situation and state of residence.

Comparatively, the tax treatment of unemployment benefits contrasts with other forms of assistance, such as welfare payments or workers’ compensation, which are often tax-exempt. This disparity highlights the importance of understanding the unique rules governing each type of benefit. For instance, while unemployment compensation is taxable, Supplemental Nutrition Assistance Program (SNAP) benefits are not. Recognizing these differences ensures compliance with tax laws and maximizes your financial stability during periods of unemployment.

In conclusion, the tax implications of unemployment benefits demand careful attention to federal and state regulations. By staying informed, utilizing available tools like tax withholding, and seeking professional guidance when needed, recipients can effectively manage their tax obligations. This proactive approach not only ensures compliance but also minimizes financial stress during an already challenging time.

Unemployment Benefits and Social Security: Understanding Their Interplay and Impact

You may want to see also

Explore related products

$12.38 $18.99

![]()

Federal vs. state guidelines

Unemployment compensation, often a financial lifeline for those between jobs, is subject to varying interpretations under federal and state guidelines. At the federal level, the IRS classifies unemployment benefits as taxable income, categorizing them as "unearned income" rather than "earned income." This distinction is crucial because earned income qualifies for certain tax credits, such as the Earned Income Tax Credit (EITC), while unearned income does not. For example, a single taxpayer earning $15,000 in unemployment benefits in 2023 would not be eligible for the EITC, as it is not considered earned income.

States, however, have their own rules that can complicate this picture. While most states follow federal guidelines in taxing unemployment benefits, some states, like California, Pennsylvania, and New Jersey, exempt unemployment compensation from state income tax entirely. This creates a disparity where a taxpayer in California might pay federal taxes on their unemployment benefits but no state taxes, while a taxpayer in Ohio would pay both. Understanding these state-specific rules is essential for accurate tax planning and avoiding unexpected liabilities.

Another layer of complexity arises when considering state-specific programs that supplement federal unemployment benefits. For instance, during the COVID-19 pandemic, the Federal Pandemic Unemployment Compensation (FPUC) provided additional weekly benefits, which were treated as taxable income both federally and in most states. However, states like Washington and Oregon allowed taxpayers to deduct a portion of their unemployment benefits from their state taxable income, offering partial relief. Such variations highlight the need for taxpayers to consult state tax codes or a tax professional to navigate these nuances.

From a practical standpoint, taxpayers should take proactive steps to manage their tax obligations. For federal taxes, opting for withholding on unemployment benefits (Form W-4V) can prevent a large tax bill at filing time. For state taxes, reviewing the specific treatment of unemployment compensation in your state is critical. For example, in Indiana, unemployment benefits are fully taxable, so taxpayers should plan accordingly. Additionally, keeping detailed records of all unemployment payments and any taxes withheld can simplify the filing process and ensure compliance with both federal and state requirements.

In conclusion, while federal guidelines clearly classify unemployment compensation as unearned income, state rules introduce significant variability. Taxpayers must be diligent in understanding these differences to avoid penalties and optimize their financial situation. Whether through withholding, deductions, or professional advice, navigating the federal vs. state landscape is key to managing unemployment benefits effectively.

Is Unemployment Compensation Included in GDP Calculations?

You may want to see also

Explore related products

![]()

Impact on other income sources

Unemployment compensation, often a financial lifeline during job transitions, interacts with other income sources in ways that can either bolster or complicate a recipient’s financial landscape. For instance, individuals receiving unemployment benefits while also earning part-time income may face reduced benefit amounts, as many states apply an earnings offset formula. In California, for example, the first $25 of weekly wages is disregarded, and 50% of remaining earnings are deducted from the unemployment check. This mechanism ensures benefits supplement, rather than replace, earned income, but it requires careful budgeting to avoid unexpected shortfalls.

From a tax perspective, unemployment compensation’s classification as unearned income creates a ripple effect on other income sources. Unlike earned income, which qualifies for tax deductions like the Earned Income Tax Credit (EITC), unemployment benefits do not. This distinction can reduce overall tax credits for individuals with mixed income streams. For example, a single filer earning $10,000 from part-time work and $5,000 in unemployment benefits would not qualify for the EITC, as the credit is based solely on earned income. Understanding this interplay is crucial for accurate tax planning and avoiding penalties.

The impact extends to retirement savings as well. Unemployment compensation does not qualify for contributions to retirement accounts like IRAs or 401(k)s, which typically require earned income. This limitation can disrupt long-term financial goals, particularly for those relying on unemployment benefits for extended periods. For instance, a 40-year-old receiving unemployment for six months would need to resume earned income to continue tax-advantaged retirement contributions. Strategically timing contributions or exploring alternative savings vehicles, such as health savings accounts (HSAs), can mitigate this gap.

Finally, unemployment benefits can influence eligibility for means-tested programs like Medicaid or SNAP, which consider both earned and unearned income. While unemployment compensation is counted as income for these programs, its temporary nature may allow recipients to maintain eligibility temporarily. However, individuals transitioning to earned income must navigate complex reporting requirements to avoid overpayment or disqualification. For example, a household receiving SNAP benefits must report changes in income within 10 days in most states, necessitating proactive communication with caseworkers to ensure compliance.

In summary, unemployment compensation’s classification as unearned income creates a layered impact on other financial sources, from benefit offsets and tax implications to retirement savings and public assistance eligibility. Navigating these interactions requires a strategic approach, including meticulous budgeting, tax planning, and timely reporting. By understanding these dynamics, individuals can optimize their financial stability during periods of unemployment and beyond.

Georgia Unemployment Compensation: Understanding Your Weekly Benefit Amount

You may want to see also

Frequently asked questions

No, unemployment compensation is not considered earned income for tax purposes. It is classified as unearned income by the IRS.

Yes, unemployment benefits can reduce your earned income tax credit (EITC) because they lower your total earned income, which is a key factor in determining EITC eligibility.

No, unemployment compensation is not counted as earned income for Social Security benefit calculations, as it does not reflect wages from employment.

![California Unemployment Insurance Code [2025 Edition]](https://m.media-amazon.com/images/I/513sESs2WkL._AC_UL320_.jpg)