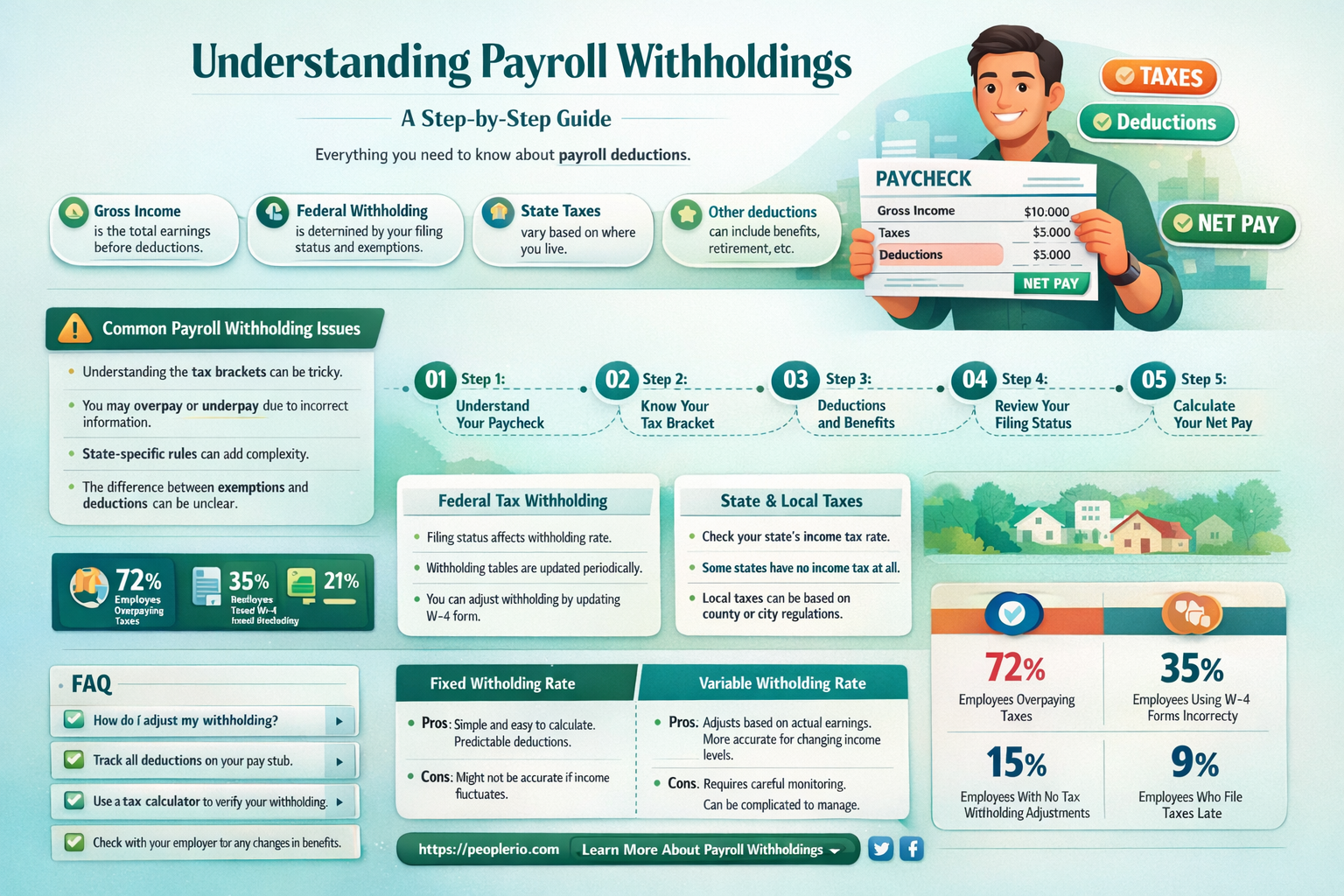

Payroll withholdings are calculated based on an employee's gross wages and are used to fund various government programs and initiatives. The process involves subtracting a certain percentage of an employee's earnings each pay period, which is then remitted to the appropriate government agencies. The amount withheld is determined by factors such as the employee's income level, marital status, and the number of allowances claimed on their W-4 form. Understanding how payroll withholdings are calculated is essential for both employers and employees to ensure compliance with tax laws and to accurately estimate take-home pay.

| Characteristics | Values |

|---|---|

| Federal Income Tax | Based on IRS tax tables and employee's W-4 form |

| Social Security Tax | 6.2% of gross wages up to annual wage base |

| Medicare Tax | 1.45% of gross wages |

| State Income Tax | Varies by state, based on state tax tables and employee's state tax withholding form |

| Local Income Tax | Varies by locality, based on local tax tables and employee's local tax withholding form |

| Unemployment Tax | Varies by state, based on state unemployment tax rates |

| Other Deductions | May include health insurance premiums, retirement plan contributions, and other voluntary deductions |

| Gross Wages | Total earnings before any deductions |

| Net Wages | Total earnings after all deductions |

| Pay Period | Frequency of pay, such as weekly, bi-weekly, semi-monthly, or monthly |

| Employee's Allowances | Number of allowances claimed on W-4 form affects federal income tax withholding |

| Tax Filing Status | Employee's tax filing status (single, married, head of household) affects federal income tax withholding |

| Wage Base | Maximum amount of wages subject to Social Security and Medicare taxes |

Explore related products

What You'll Learn

- Gross Income: Determining total earnings before deductions, including salary, wages, tips, and commissions

- Allowances: Understanding the number of allowances claimed on Form W-4, which affects withholding amounts

- Tax Withholding: Calculating federal income tax based on IRS tables and employee's filing status

- Social Security and Medicare: Withholding percentages for these programs, which are mandatory for most employees

- State and Local Taxes: Additional withholdings for state income tax, local taxes, and other regional deductions

![]()

Gross Income: Determining total earnings before deductions, including salary, wages, tips, and commissions

To calculate gross income, you must first understand what constitutes earnings before deductions. This includes salary, wages, tips, and commissions. Salary and wages are typically fixed amounts paid regularly, while tips and commissions are variable and depend on performance or sales.

For example, if an employee earns a base salary of $4,000 per month and receives an additional $500 in tips and $1,000 in commissions, their gross income for the month would be $5,500. It's important to note that gross income is calculated before any deductions, such as taxes, social security, or health insurance premiums, are taken out.

When calculating gross income, it's also important to consider any other sources of income, such as rental income or investment earnings. These amounts should be added to the total gross income to get an accurate picture of an individual's earnings before deductions.

In some cases, employees may receive non-cash compensation, such as stock options or employer-provided housing. These benefits should also be included in the gross income calculation, as they represent additional earnings.

Once the gross income is calculated, it can be used to determine the amount of payroll withholdings, such as federal and state income taxes, social security, and Medicare. These withholdings are typically calculated as a percentage of the gross income and are deducted from the employee's paycheck.

For example, if an employee's gross income is $5,500 per month, and the federal income tax withholding rate is 25%, the employee would have $1,375 withheld from their paycheck for federal income taxes. Similarly, if the state income tax withholding rate is 5%, the employee would have an additional $275 withheld for state income taxes.

In conclusion, calculating gross income is an essential step in determining payroll withholdings. By understanding what constitutes gross income and how to calculate it accurately, employees and employers can ensure that the correct amounts are withheld from paychecks and paid to the appropriate tax authorities.

Mastering Non-Farm Payroll Calculations: A Step-by-Step Guide for Beginners

You may want to see also

Explore related products

![]()

Allowances: Understanding the number of allowances claimed on Form W-4, which affects withholding amounts

The number of allowances claimed on Form W-4 is a critical factor in determining how much federal income tax is withheld from an employee's paycheck. Each allowance represents a specific amount of money that the employee expects to deduct from their taxable income, such as for dependents, mortgage interest, or charitable contributions. The more allowances claimed, the less tax is withheld, resulting in a larger paycheck but potentially a larger tax bill at the end of the year.

To understand the impact of allowances on withholding amounts, it's essential to know how the withholding system works. Employers use the information provided on Form W-4 to calculate the amount of tax to withhold from each paycheck. The form includes tables that correspond to different filing statuses and income levels, which help determine the appropriate withholding amount based on the number of allowances claimed.

For example, if a single taxpayer claims two allowances, the employer will withhold less tax than if the same taxpayer claimed zero allowances. This is because the two allowances reduce the taxpayer's taxable income, resulting in a lower tax liability. However, if the taxpayer's actual deductions at the end of the year are less than the amount withheld based on the claimed allowances, they may owe additional tax when filing their return.

It's also important to note that the number of allowances claimed can affect other aspects of payroll withholding, such as Social Security and Medicare taxes. While these taxes are typically withheld at a flat rate, the amount of taxable income subject to these taxes can be reduced by the allowances claimed on Form W-4.

In conclusion, understanding the number of allowances claimed on Form W-4 is crucial for both employees and employers. It directly impacts the amount of tax withheld from each paycheck and can have significant consequences for the taxpayer's overall tax liability. By carefully considering the number of allowances to claim, employees can optimize their withholding amounts and avoid potential tax surprises at the end of the year.

Mastering Hourly Payroll Calculations: A Step-by-Step Guide for Employers

You may want to see also

Explore related products

![]()

Tax Withholding: Calculating federal income tax based on IRS tables and employee's filing status

To calculate federal income tax withholdings, employers must refer to the IRS withholding tables, which provide a structured approach based on an employee's filing status and income. The process begins with the employee completing a Form W-4, which indicates their filing status, number of dependents, and any additional withholding they wish to have deducted. This information is crucial as it determines the amount of tax withheld from each paycheck.

The IRS tables are divided into different sections corresponding to the various filing statuses: single, married filing jointly, married filing separately, and head of household. Each section contains a series of rows and columns that intersect to provide the specific withholding amount based on the employee's income and the information provided on their W-4 form. Employers must match the employee's income to the corresponding row and then locate the column that aligns with the number of dependents and any additional withholding requested.

For example, if a single employee earns $1,000 per week and claims no dependents, the employer would locate the row for $1,000 in the single filing status section and then find the column for zero dependents. The intersection of this row and column would provide the exact amount of federal income tax to be withheld from the employee's paycheck.

It's important to note that the IRS updates its withholding tables annually to reflect changes in tax laws and rates. Employers must ensure they are using the most current tables to accurately calculate withholdings. Failure to do so could result in under or over-withholding, leading to potential penalties or employees owing additional taxes when filing their annual returns.

In addition to federal income tax, employers may also need to withhold state and local taxes, as well as other deductions such as Social Security and Medicare. However, the focus of this section is solely on federal income tax withholdings, which are calculated using the IRS tables and the employee's filing status as outlined above.

Efficient Payroll Management: Kenya's Aren Calculator Explained

You may want to see also

Explore related products

![]()

Social Security and Medicare: Withholding percentages for these programs, which are mandatory for most employees

Social Security and Medicare are two critical programs funded through payroll withholdings, which are mandatory for most employees in the United States. The withholding percentages for these programs are set by law and are subject to change based on legislative adjustments. As of the latest information available up to April 2023, the Social Security tax rate is 6.2% for both employees and employers, while the Medicare tax rate is 1.45% for employees and 1.45% for employers. Additionally, there is an extra 0.9% Medicare tax for employees who earn more than $200,000 per year ($250,000 for married couples filing jointly).

To calculate the Social Security and Medicare withholdings, employers must first determine the employee's gross wages for the pay period. Gross wages include all forms of compensation, such as salaries, wages, tips, and bonuses. Once the gross wages are determined, the employer applies the respective withholding percentages to calculate the amount to be withheld for each program. For example, if an employee earns $1,000 in a pay period, the Social Security withholding would be $62 ($1,000 x 0.062), and the Medicare withholding would be $14.50 ($1,000 x 0.0145).

It is important for employers to accurately calculate and remit these withholdings to the Internal Revenue Service (IRS) on a timely basis. Failure to do so can result in penalties and interest charges. Employees should also review their pay stubs to ensure that the correct amounts are being withheld and report any discrepancies to their employer.

In addition to the basic withholding percentages, there are other factors that can affect the calculation of Social Security and Medicare taxes. For instance, certain types of income, such as tips and bonuses, may be subject to additional withholding requirements. Employers must also consider the annual wage base limits for Social Security taxes, which are adjusted for inflation each year. As of 2023, the wage base limit for Social Security taxes is $147,000.

Understanding how Social Security and Medicare withholdings are calculated is essential for both employers and employees. Employers must ensure compliance with the law to avoid penalties, while employees should be aware of the amounts being withheld to plan for their financial future and ensure they are receiving the correct benefits. By staying informed about the latest tax rates and regulations, both parties can contribute to the sustainability of these vital programs.

Understanding IRA Calculations in Payroll: A Comprehensive Guide

You may want to see also

Explore related products

![]()

State and Local Taxes: Additional withholdings for state income tax, local taxes, and other regional deductions

In addition to federal income tax withholdings, employees may also have state and local taxes deducted from their paychecks. These additional withholdings can vary significantly depending on the state and locality in which the employee resides or works. State income tax rates range from 0% to over 16%, and local taxes can add another 1% to 4% or more.

To calculate state and local tax withholdings, employers must first determine which taxes apply to their employees based on their work location and residency status. For example, an employee who lives in one state but works in another may be subject to both states' income taxes. Employers must then use the appropriate tax tables or formulas to calculate the amount of tax to withhold.

State and local tax withholdings can also include other regional deductions, such as city or county taxes, transit taxes, or special district taxes. These taxes may be used to fund local services, infrastructure projects, or other community needs. Employers must be aware of all applicable taxes and deductions in order to accurately calculate their employees' payroll withholdings.

One common mistake employers make is failing to account for state and local tax credits or exemptions. For example, some states offer tax credits for certain types of income, such as military pay or teacher salaries. Employers must also be aware of any local tax exemptions or abatements that may apply to their employees.

To avoid errors and ensure compliance with state and local tax laws, employers should regularly review and update their payroll withholding procedures. This may involve consulting with tax professionals or using payroll software that automatically calculates and updates tax withholdings based on the latest tax rates and regulations.

In conclusion, state and local tax withholdings are an important aspect of payroll processing that requires careful attention to detail and knowledge of applicable tax laws. By understanding the unique aspects of state and local taxes, employers can ensure accurate and compliant payroll withholdings for their employees.

Efficient Payroll Calculation: Mastering 45-Minute Time Tracking for Accuracy

You may want to see also

Frequently asked questions

Payroll withholdings are primarily calculated based on an employee's gross wages, federal income tax withholding, Social Security tax, Medicare tax, and any applicable state and local taxes.

Federal income tax withholding is determined using the employee's Form W-4, which provides the employer with the necessary information to calculate the amount of tax to withhold based on the employee's filing status, number of allowances, and additional withholding amounts.

Social Security and Medicare taxes are payroll taxes that fund the Social Security and Medicare programs. These taxes are withheld from an employee's wages and matched by the employer, ensuring that both the employee and employer contribute to these essential government programs.

Yes, in addition to federal, Social Security, and Medicare taxes, payroll withholdings may also include state and local income taxes, unemployment insurance taxes, and other voluntary deductions such as retirement plan contributions or health insurance premiums.

Payroll withholdings are typically submitted to the government on a quarterly basis, although the specific frequency may vary depending on the employer's size and the amount of taxes withheld. Employers must file Form 941, Employer's Quarterly Federal Tax Return, to report and pay the withheld taxes to the IRS.

![The People'S Right Defended : Being an Examination of the Romish Principle of Withholding the Scriptures from the Laity : Together with a Discussion of Some Other Points in the 1831 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)