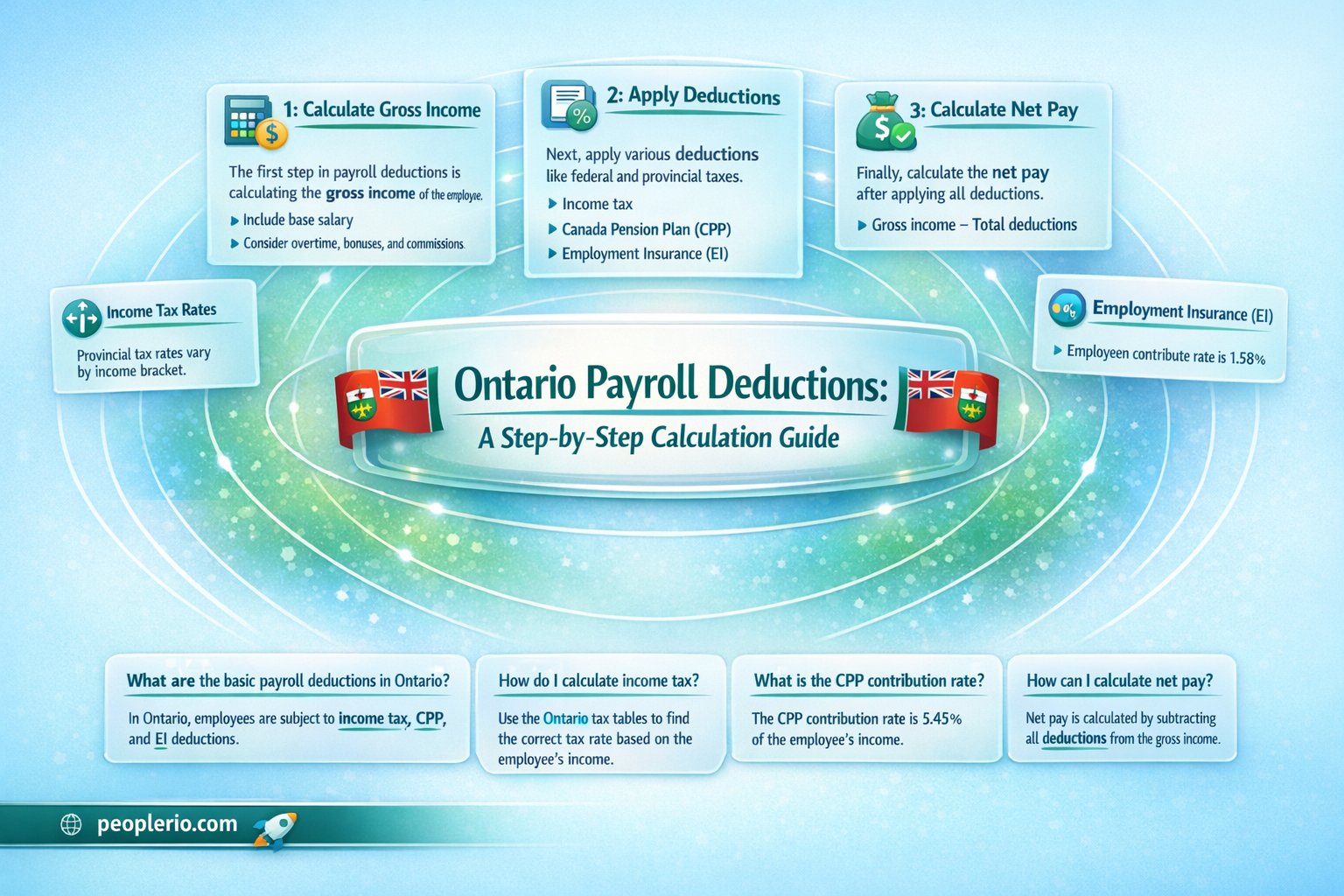

Calculating payroll deductions in Ontario involves several key steps. First, you need to determine the employee's gross income for the pay period. Next, you'll calculate the deductions for income tax, which are based on the employee's taxable income and the tax rates set by the province. In addition to income tax, you'll also need to deduct Canada Pension Plan (CPP) contributions, which are calculated as a percentage of the employee's earnings up to a certain maximum. Another important deduction is for Employment Insurance (EI), which is also calculated as a percentage of earnings. Finally, you may need to consider other deductions such as health insurance premiums or union dues, depending on the specific circumstances of the employee. It's important to ensure that all deductions are calculated accurately and in compliance with Ontario's payroll deduction regulations.

| Characteristics | Values |

|---|---|

| Province | Ontario |

| Calculation | Payroll deductions |

| Components | Income tax, CPP, EI, WSIB |

| Income tax rate | 5.05% (provincial) |

| CPP rate | 5.25% (employee contribution) |

| EI rate | 1.62% (employee contribution) |

| WSIB rate | Varies (employer contribution) |

| Calculation | Gross income - deductions = net pay |

| Resources | CRA website, Ontario government website |

Explore related products

What You'll Learn

- Understanding Ontario Payroll Deductions: Overview of provincial payroll taxes and deductions in Ontario

- Calculating Ontario Health Insurance Plan (OHIP) Premiums: How to determine OHIP premiums based on employee income

- Ontario Pension Plan (OPP) Contributions: Calculating mandatory OPP contributions for employees and employers

- Taxable Benefits and Allowances: Identifying and calculating taxable benefits, such as parking and meal allowances

- Payroll Deduction Formulas and Examples: Step-by-step formulas and examples for calculating total payroll deductions in Ontario

![]()

Understanding Ontario Payroll Deductions: Overview of provincial payroll taxes and deductions in Ontario

Ontario payroll deductions encompass a range of provincial taxes and deductions that employers must withhold from employees' wages. These deductions are integral to funding various provincial programs and services, including healthcare, education, and social assistance. Understanding these deductions is crucial for both employers and employees to ensure compliance with provincial regulations and to accurately calculate take-home pay.

The primary payroll deductions in Ontario include the Ontario Health Insurance Plan (OHIP), the Ontario Disability Support Program (ODSP), and the Workplace Safety and Insurance Board (WSIB) premiums. OHIP deductions fund the provincial healthcare system, providing coverage for medical services and hospital stays. ODSP deductions support the program that offers financial assistance to individuals with disabilities, helping them cover living expenses and access necessary services. WSIB premiums contribute to the workers' compensation system, which provides benefits to employees who are injured or become ill due to their work.

Employers are responsible for calculating and remitting these deductions to the appropriate provincial authorities. The deduction amounts are typically based on a percentage of the employee's earnings, with specific rates set by the province. For example, the OHIP deduction rate is 1.5% of the employee's gross earnings, up to a maximum annual amount. Employers must also consider other factors, such as the employee's age, income level, and employment status, when determining the applicable deduction rates.

To accurately calculate Ontario payroll deductions, employers can use the following steps:

- Determine the employee's gross earnings for the pay period.

- Apply the OHIP deduction rate to the gross earnings, ensuring not to exceed the annual maximum.

- Calculate the ODSP deduction based on the employee's earnings and the applicable rate.

- Compute the WSIB premium by applying the appropriate rate to the employee's earnings, considering the industry and the employee's role.

- Sum the deductions to determine the total amount to be withheld from the employee's wages.

It is essential for employers to stay informed about any changes to Ontario's payroll deduction rates and regulations, as these can impact the calculation process and the overall cost of employment. Additionally, employees should be aware of these deductions to understand their take-home pay and to ensure that they are receiving the correct benefits and protections.

Healthcare Costs: Should They Be Factored into Gross Payroll?

You may want to see also

Explore related products

![]()

Calculating Ontario Health Insurance Plan (OHIP) Premiums: How to determine OHIP premiums based on employee income

To calculate Ontario Health Insurance Plan (OHIP) premiums based on employee income, you need to follow a specific formula that takes into account the employee's annual earnings. The OHIP premium rate is a percentage of the employee's income, and this rate can change annually. As of the latest update, the OHIP premium rate is 1.35% of the employee's annual earnings up to a maximum amount, which is adjusted yearly for inflation.

First, determine the employee's annual income. This includes all taxable earnings, such as wages, salaries, commissions, and bonuses. Once you have the annual income figure, apply the OHIP premium rate to calculate the total premium amount. For example, if an employee earns $50,000 annually, the OHIP premium would be 1.35% of $50,000, which equals $675.

It's important to note that there is a maximum premium amount that an employee can be required to pay. This maximum is based on a percentage of the average industrial wage in Ontario. If an employee's income exceeds this threshold, their OHIP premium will be capped at the maximum amount.

Additionally, employees who earn less than a certain amount annually may be eligible for a reduced OHIP premium rate or even exempt from paying premiums altogether. This is to ensure that low-income individuals have access to health care without undue financial burden.

When calculating OHIP premiums, it's crucial to use the correct premium rate for the current year and to accurately determine the employee's annual income. Mistakes in these calculations can lead to incorrect premium amounts being deducted, which can cause issues for both the employee and the employer.

In summary, calculating OHIP premiums based on employee income involves determining the annual earnings, applying the correct premium rate, and considering any maximum or reduced premium thresholds that may apply. This process ensures that employees contribute a fair amount towards their health care coverage while also protecting low-income individuals from excessive financial strain.

Understanding Railroad Payroll Deductions: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Ontario Pension Plan (OPP) Contributions: Calculating mandatory OPP contributions for employees and employers

To calculate mandatory Ontario Pension Plan (OPP) contributions for employees and employers, you need to understand the contribution rates and the earnings thresholds. As of the latest information available up to June 2024, the OPP contribution rate for employees is 9.95% of their earnings, while for employers, it is 11.95% of the employee's earnings. These rates are subject to change, so it's essential to verify the current rates with the OPP or a reliable source.

The first step in calculating OPP contributions is to determine the employee's earnings for the pay period. Earnings include salary, wages, commissions, bonuses, and any other form of compensation. Once you have the earnings figure, you can apply the contribution rates. For example, if an employee earns $1,000 in a pay period, the employee's OPP contribution would be $99.50 (9.95% of $1,000), and the employer's contribution would be $119.50 (11.95% of $1,000).

It's important to note that OPP contributions are typically deducted from the employee's gross pay before taxes are calculated. This means that the contributions are made on a pre-tax basis, which can reduce the employee's taxable income. Employers must also ensure that they are accurately reporting and remitting OPP contributions to avoid penalties and interest charges.

In addition to the basic contribution rates, there are other factors that can affect OPP contributions, such as the employee's age and the type of employment. For example, employees who are 65 years of age or older may be eligible for reduced OPP contributions. Employers should also be aware of any special rules or exemptions that may apply to certain types of employees or industries.

To ensure accurate OPP contributions, employers should regularly review and update their payroll systems to reflect any changes in contribution rates or earnings thresholds. It's also a good practice to communicate with employees about their OPP contributions and how they are calculated, as this can help to avoid misunderstandings and ensure transparency in the payroll process.

In summary, calculating mandatory OPP contributions involves determining the employee's earnings, applying the appropriate contribution rates, and ensuring that the contributions are deducted and remitted correctly. Employers should stay informed about any changes to OPP rules and regulations to maintain compliance and avoid potential penalties.

Understanding Payroll Costs Calculation for PPP Loans

You may want to see also

Explore related products

![]()

Taxable Benefits and Allowances: Identifying and calculating taxable benefits, such as parking and meal allowances

Identifying and calculating taxable benefits is a crucial aspect of payroll deductions in Ontario. Taxable benefits are perks provided by employers to employees that have a monetary value and are subject to taxation. Common examples include parking allowances, meal allowances, and transportation costs. To accurately calculate payroll deductions, it's essential to understand how these benefits are taxed and reported.

When it comes to parking allowances, employers must determine the fair market value of the benefit provided. This can be calculated by considering the cost of parking in the area where the employee works. For example, if an employer provides a parking space in a downtown Toronto location where the average monthly parking fee is $200, the fair market value of the benefit would be $200 per month. This amount would then be added to the employee's gross income and taxed accordingly.

Meal allowances are another common taxable benefit. Employers may provide employees with a daily meal allowance or a meal plan. The fair market value of the meal allowance is determined by the cost of purchasing a meal in the area where the employee works. For instance, if an employer provides a daily meal allowance of $15 and the average cost of a meal in the area is $12, the fair market value of the benefit would be $3 per day. This amount would be added to the employee's gross income and taxed.

It's important to note that some benefits may be exempt from taxation. For example, if an employer provides a meal allowance to an employee who works in a remote location where there are no meal options available, the allowance may be exempt from taxation. Additionally, some benefits may be subject to a different tax rate than regular income. Employers should consult with a tax professional to determine the tax implications of specific benefits.

In conclusion, accurately identifying and calculating taxable benefits is essential for payroll deductions in Ontario. Employers must determine the fair market value of benefits such as parking and meal allowances and add them to the employee's gross income for taxation purposes. Understanding the tax implications of these benefits can help employers avoid penalties and ensure compliance with tax laws.

Understanding Payroll's Role in Cost of Goods Sold Calculations

You may want to see also

Explore related products

![]()

Payroll Deduction Formulas and Examples: Step-by-step formulas and examples for calculating total payroll deductions in Ontario

To calculate payroll deductions in Ontario, you'll need to follow a series of steps that involve applying various formulas to the employee's gross pay. Let's break down the process with some step-by-step formulas and examples.

First, you'll need to calculate the employee's gross pay, which is the total amount of money earned before any deductions are made. Once you have the gross pay, you can start applying the following formulas to calculate the different types of payroll deductions.

The first deduction you'll need to make is for Canada Pension Plan (CPP) contributions. The CPP contribution rate is 5.1% of the employee's gross pay, up to a maximum annual contribution of $3,500. To calculate the CPP deduction, you can use the following formula:

CPP Deduction = Gross Pay × 0.051

For example, if an employee's gross pay is $50,000, the CPP deduction would be:

CPP Deduction = $50,000 × 0.051 = $2,550

Next, you'll need to calculate the employee's Ontario Health Insurance Plan (OHIP) premiums. The OHIP premium rate is 1.5% of the employee's gross pay, up to a maximum annual premium of $900. To calculate the OHIP premium, you can use the following formula:

OHIP Premium = Gross Pay × 0.015

For example, if an employee's gross pay is $50,000, the OHIP premium would be:

OHIP Premium = $50,000 × 0.015 = $750

After calculating the CPP deduction and OHIP premium, you'll need to calculate the employee's income tax deductions. This can be a bit more complex, as it depends on the employee's taxable income and the tax rates that apply. However, you can use the following formula to calculate the federal income tax deduction:

Federal Income Tax Deduction = Taxable Income × Federal Tax Rate

For example, if an employee's taxable income is $40,000 and the federal tax rate is 15%, the federal income tax deduction would be:

Federal Income Tax Deduction = $40,000 × 0.15 = $6,000

You'll also need to calculate the provincial income tax deduction, which is based on the employee's taxable income and the Ontario tax rates. The Ontario tax rates are progressive, meaning that the tax rate increases as the taxable income increases. You can use the following formula to calculate the provincial income tax deduction:

Provincial Income Tax Deduction = Taxable Income × Provincial Tax Rate

For example, if an employee's taxable income is $40,000 and the Ontario tax rate is 9.9%, the provincial income tax deduction would be:

Provincial Income Tax Deduction = $40,000 × 0.099 = $3,960

Finally, you'll need to calculate the total payroll deductions by adding up all of the individual deductions. You can use the following formula to calculate the total payroll deductions:

Total Payroll Deductions = CPP Deduction + OHIP Premium + Federal Income Tax Deduction + Provincial Income Tax Deduction

For example, if the CPP deduction is $2,550, the OHIP premium is $750, the federal income tax deduction is $6,000, and the provincial income tax deduction is $3,960, the total payroll deductions would be:

Total Payroll Deductions = $2,550 + $750 + $6,000 + $3,960 = $13,260

By following these steps and using the formulas provided, you can accurately calculate the total payroll deductions for an employee in Ontario.

Understanding Payroll Withholdings: A Step-by-Step Guide

You may want to see also

Frequently asked questions

Payroll deductions in Ontario typically include federal and provincial income taxes, Canada Pension Plan (CPP) contributions, Employment Insurance (EI) premiums, and possibly other deductions such as union dues or garnishments.

To calculate the federal income tax deduction, you need to use the federal tax rates and brackets provided by the Canada Revenue Agency (CRA). Apply the appropriate tax rate to the employee's taxable income to determine the federal income tax deduction.

The CPP contribution rate for 2023 in Ontario is 5.7% of the employee's pensionable earnings, up to the maximum pensionable earnings limit.

The EI premium deduction is calculated as 1.6% of the employee's insurable earnings, up to the maximum insurable earnings limit. Multiply the employee's insurable earnings by the EI premium rate to determine the deduction.

Yes, in addition to provincial income tax, there may be other provincial deductions such as the Ontario Health Insurance Plan (OHIP) premium, which is calculated based on the employee's income.