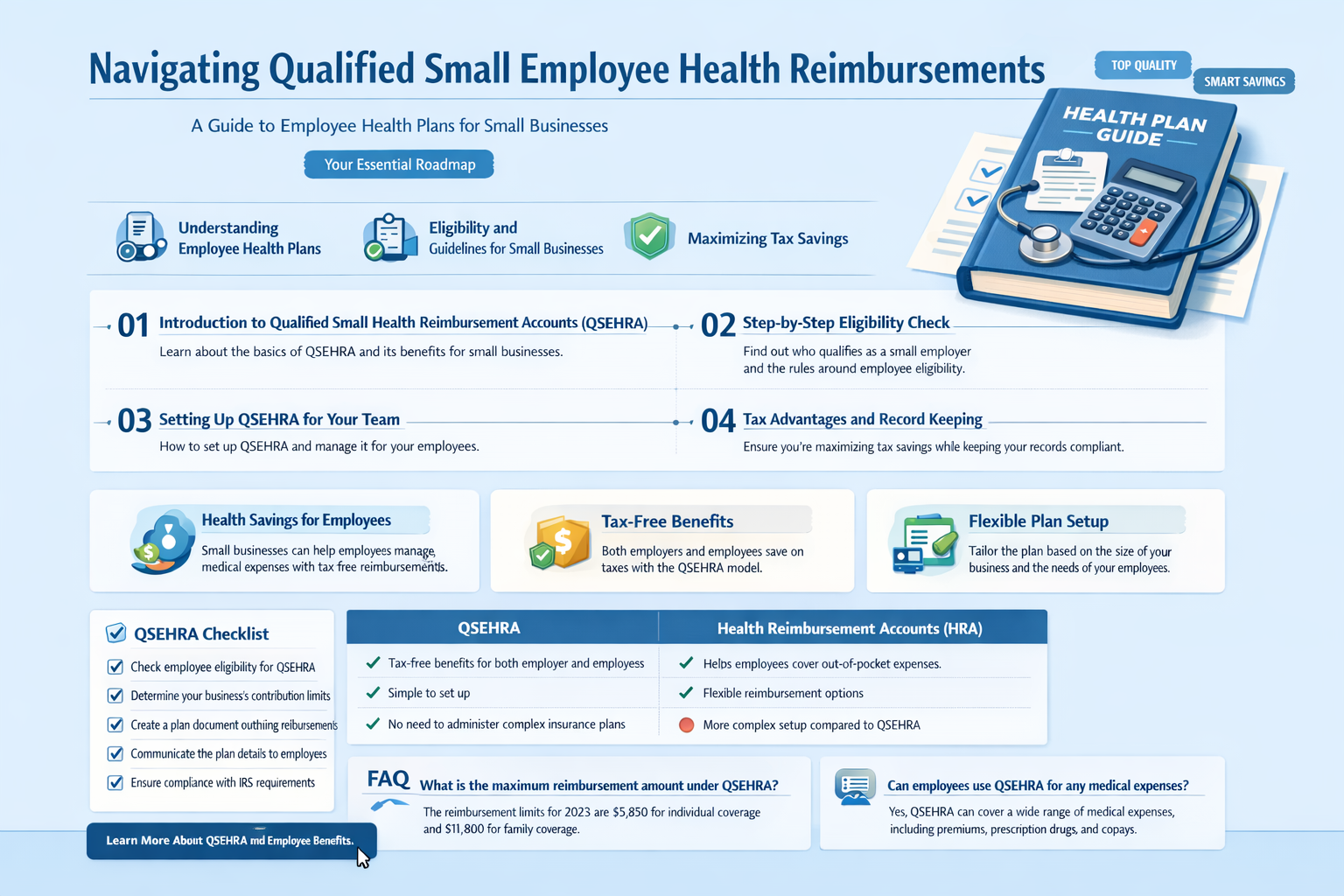

The Qualified Small Employer Health Reimbursement Arrangement (QSEHRA) is a type of health reimbursement arrangement that allows small employers to reimburse their employees for health insurance premiums and other medical expenses. To set up a QSEHRA, employers must meet certain eligibility requirements, such as having fewer than 50 full-time employees and not being subject to the Affordable Care Act's employer mandate. Once established, the QSEHRA can provide a tax-advantaged way for employers to help their employees afford health insurance and other healthcare costs.

| Characteristics | Values |

|---|---|

| Name | Qualified Small Employee Health Reimbursement Arrangement (QSEHRA) |

| Purpose | To reimburse small employees for health insurance premiums or medical expenses |

| Eligibility | Small employers with fewer than 50 full-time equivalent employees |

| Contribution Limit | Varies by year, indexed for inflation |

| Tax Treatment | Employer contributions are tax-deductible; reimbursements are tax-free to employees |

| Administration | Employers must establish a written plan and maintain records of contributions and reimbursements |

| Compliance | Must comply with IRS regulations and reporting requirements |

| Advantages | Allows small employers to provide health benefits without purchasing group insurance; flexible and customizable |

| Disadvantages | Limited contribution amounts; may not cover all employee health expenses |

| Alternatives | Group health insurance, Health Savings Accounts (HSAs), Flexible Spending Accounts (FSAs) |

Explore related products

What You'll Learn

- Eligibility Criteria: Understand the requirements for employees to qualify for the health reimbursement arrangement

- Documentation Needed: Gather necessary documents such as receipts, invoices, and proof of insurance coverage

- Reimbursement Process: Familiarize yourself with the step-by-step procedure for submitting and processing reimbursement claims

- Tax Implications: Learn about the tax benefits and potential implications of participating in a qualified health reimbursement arrangement

- Common Mistakes to Avoid: Identify and steer clear of frequent errors that could delay or complicate the reimbursement process

![]()

Eligibility Criteria: Understand the requirements for employees to qualify for the health reimbursement arrangement

To qualify for the health reimbursement arrangement (HRA), employees must meet specific eligibility criteria set by the employer. These criteria typically include factors such as employment status, job classification, and possibly the number of hours worked per week. For instance, an employer might require that employees work at least 30 hours per week to be eligible for the HRA. Additionally, the criteria may stipulate that only full-time employees are eligible, excluding part-time or temporary workers.

Another important aspect of eligibility criteria is the definition of "qualified small employer." According to the IRS, a qualified small employer is one that has fewer than 50 full-time employees and does not offer a self-insured health plan. This means that if an employer has 50 or more full-time employees, they would not be eligible to offer a qualified small employer HRA. Furthermore, if an employer offers a self-insured health plan, they are also disqualified from offering an HRA.

The eligibility criteria may also include requirements related to the employee's health insurance coverage. For example, an employer might require that employees have a high-deductible health plan (HDHP) to be eligible for the HRA. This is because HRAs are designed to help employees cover the costs of their health insurance premiums and out-of-pocket medical expenses, so it makes sense that employees with HDHPs would be the primary beneficiaries.

Employers may also set eligibility criteria based on the employee's income level. For instance, an employer might require that employees earn below a certain income threshold to be eligible for the HRA. This is because HRAs are intended to help lower-income employees afford health insurance, so it would be reasonable to limit eligibility to those who truly need the assistance.

Finally, employers may have additional eligibility criteria that are specific to their company or industry. For example, an employer might require that employees have been with the company for a certain amount of time before they become eligible for the HRA. Alternatively, an employer might require that employees meet certain performance or productivity standards to be eligible.

In conclusion, understanding the eligibility criteria for the health reimbursement arrangement is crucial for both employers and employees. Employers need to ensure that they are offering the HRA to the right employees, while employees need to know whether they qualify for the benefit. By carefully reviewing the eligibility criteria, both parties can make informed decisions about the HRA and how it can best be used to support employee health and well-being.

Ensuring Workplace Wellness: Effective Strategies for Monitoring Employee Health

You may want to see also

Explore related products

$162 $245.95

![]()

Documentation Needed: Gather necessary documents such as receipts, invoices, and proof of insurance coverage

To properly execute a Qualified Small Employer Health Reimbursement Arrangement (QSEHRA), meticulous documentation is paramount. This section will guide you through the essential documents required to ensure compliance and facilitate smooth reimbursement processes.

First and foremost, you will need to gather all receipts and invoices related to the health expenses incurred by your employees. These documents serve as proof of the expenditures and are necessary to validate the reimbursement claims. It is crucial to ensure that the receipts and invoices are itemized, showing the specific services or products purchased, along with the corresponding dates and amounts.

In addition to receipts and invoices, you must also obtain proof of insurance coverage for each employee participating in the QSEHRA. This can include insurance cards, policy documents, or letters from the insurance provider confirming the employee's enrollment and coverage dates. Having this documentation on hand will help verify that the expenses claimed are indeed eligible for reimbursement under the arrangement.

Furthermore, it is advisable to maintain a comprehensive record of all communications and interactions with employees regarding their health expenses and reimbursement claims. This can include emails, phone call logs, and meeting notes. Such documentation can be invaluable in resolving any disputes or clarifying misunderstandings that may arise during the reimbursement process.

Lastly, consider implementing a system for organizing and storing these documents securely. This could involve using a dedicated software platform or creating a filing system that allows for easy access and retrieval of the necessary paperwork. By keeping your documentation in order, you can streamline the reimbursement process and reduce the risk of errors or delays.

In summary, the key to successful QSEHRA administration lies in thorough documentation. By gathering and maintaining the necessary receipts, invoices, proof of insurance coverage, and communication records, you can ensure a smooth and compliant reimbursement process for your employees.

Are Employee Health Insurance Contributions Taxable? Key Facts Explained

You may want to see also

Explore related products

![]()

Reimbursement Process: Familiarize yourself with the step-by-step procedure for submitting and processing reimbursement claims

To initiate the reimbursement process for qualified small employee health expenses, you must first gather all necessary documentation. This includes itemized receipts for medical expenses, a completed reimbursement claim form, and any supporting documentation required by your employer's plan. Ensure that all receipts are clear and legible, and that they include the date of service, the provider's name, and the amount charged.

Once you have gathered all necessary documentation, you should review your employer's reimbursement policy to ensure that you understand the eligible expenses and the reimbursement process. This policy will outline the types of expenses that are eligible for reimbursement, the maximum reimbursement amount, and the deadline for submitting claims. It is important to note that some employers may have specific requirements for submitting claims, such as using a designated online portal or mailing claims to a specific address.

After reviewing your employer's policy, you should complete the reimbursement claim form. This form will typically require you to provide your name, employee ID number, the date of service, the provider's name, the amount charged, and a description of the service or expense. Be sure to double-check the form for accuracy and completeness before submitting it.

Once you have completed the claim form, you should submit it along with your supporting documentation to your employer's designated claims administrator. This may be done electronically through an online portal, or by mailing the documents to a specific address. Be sure to keep a copy of your claim form and supporting documentation for your records.

After submitting your claim, you should expect to receive a confirmation of receipt from the claims administrator. This confirmation will typically include a claim number and an estimated processing time. If you do not receive a confirmation within a reasonable timeframe, you should follow up with the claims administrator to ensure that your claim has been received and is being processed.

Finally, once your claim has been processed, you should receive a reimbursement payment from your employer. This payment will typically be made through direct deposit or by mailing a check to your designated address. If you have any questions or concerns about the reimbursement process, you should contact your employer's claims administrator for assistance.

Understanding FICA: Are Employee Paid Health Insurance Premiums Subject to FICA?

You may want to see also

![]()

Tax Implications: Learn about the tax benefits and potential implications of participating in a qualified health reimbursement arrangement

Participating in a qualified health reimbursement arrangement (HRA) can offer significant tax benefits to small employers and their employees. One of the primary advantages is that contributions made by the employer to the HRA are tax-deductible as a business expense. This can help reduce the overall taxable income of the business, leading to lower tax liabilities. Additionally, the funds within the HRA grow tax-free, meaning that any interest or investment gains are not subject to taxation.

For employees, the benefits are equally compelling. Reimbursements from the HRA for qualified medical expenses are tax-free, providing a valuable perk that can help offset the costs of healthcare. This tax-free status applies to both current and future medical expenses, making it a flexible and attractive option for employees. Furthermore, employees who contribute to the HRA through payroll deductions may be able to reduce their taxable income, depending on the specific structure of the plan.

However, it's important to note that there are certain conditions that must be met to qualify for these tax benefits. The HRA must be properly structured and administered, and the expenses reimbursed must be for qualified medical care. Employers should also be aware of the potential implications of offering an HRA, such as the need to comply with relevant tax laws and regulations. Failure to meet these requirements could result in the loss of tax benefits or even penalties.

To maximize the tax advantages of an HRA, employers should consult with a tax professional or benefits advisor to ensure that their plan is properly set up and administered. This may involve reviewing the plan's design, contribution levels, and reimbursement procedures to ensure compliance with tax laws. Additionally, employers should communicate the tax benefits of the HRA to their employees, as this can help increase participation and improve overall satisfaction with the benefits package.

In conclusion, the tax implications of participating in a qualified health reimbursement arrangement can be significant, offering valuable benefits to both employers and employees. By understanding and meeting the necessary requirements, businesses can leverage HRAs as a powerful tool for managing healthcare costs and improving their overall tax position.

Understanding Health Coverage Eligibility as a Walgreens Employee

You may want to see also

![]()

Common Mistakes to Avoid: Identify and steer clear of frequent errors that could delay or complicate the reimbursement process

One common mistake to avoid when dealing with qualified small employee health reimbursement is failing to maintain accurate and detailed records. This can lead to delays in the reimbursement process as the insurance provider may request additional documentation to verify the claims. To steer clear of this error, it is essential to keep meticulous records of all medical expenses, including receipts, invoices, and explanations of benefits.

Another frequent error is not understanding the specific requirements and limitations of the reimbursement plan. This can result in submitting claims for expenses that are not covered or exceed the plan's limits. To avoid this, employees should familiarize themselves with the terms and conditions of their reimbursement plan, including any deductibles, copays, or maximum payout amounts.

A third mistake to avoid is missing deadlines for submitting reimbursement claims. Insurance providers often have strict timeframes within which claims must be filed, and failing to meet these deadlines can result in denied claims. To prevent this, employees should be aware of the submission deadlines and ensure that their claims are filed promptly.

Additionally, it is crucial to avoid submitting incomplete or inaccurate information on reimbursement forms. This can lead to delays or denials in the reimbursement process. To avoid this, employees should carefully review their forms for any errors or missing information before submitting them.

Lastly, not following up on the status of reimbursement claims can also be a mistake. If a claim is denied or delayed, it is essential to follow up with the insurance provider to understand the reason and take any necessary steps to resolve the issue. By staying proactive and informed, employees can avoid common mistakes and ensure a smoother reimbursement process.

Are Employee Paid Health Insurance Premiums Subject to FUTA?

You may want to see also

Frequently asked questions

A QSEHRA is a type of health reimbursement arrangement that allows small employers to reimburse their employees for individual health insurance premiums and out-of-pocket medical expenses. It is designed to help small businesses provide health benefits to their employees without the need for a traditional group health insurance plan.

Small employers with fewer than 50 full-time equivalent employees are eligible to offer a QSEHRA. Additionally, the employer must not offer a group health insurance plan to any of their employees.

With a QSEHRA, employees purchase their own individual health insurance plans and submit their premiums and qualified medical expenses to their employer for reimbursement. The employer then reimburses the employee up to a certain dollar amount per month, which is determined by the employer.

For employers, a QSEHRA can be a more cost-effective way to provide health benefits to their employees compared to a traditional group health insurance plan. It also allows employers to offer a flexible benefit that can be tailored to their employees' individual needs. For employees, a QSEHRA can provide them with more control over their health insurance choices and potentially lower their out-of-pocket expenses.

Yes, there are tax implications for a QSEHRA. The reimbursements made by the employer are generally tax-free to the employee, as long as they are used for qualified medical expenses. However, the employer may need to report the reimbursements on the employee's W-2 form and may also need to pay employment taxes on the reimbursements. It is important for employers to consult with a tax professional to ensure they are complying with all applicable tax laws and regulations.