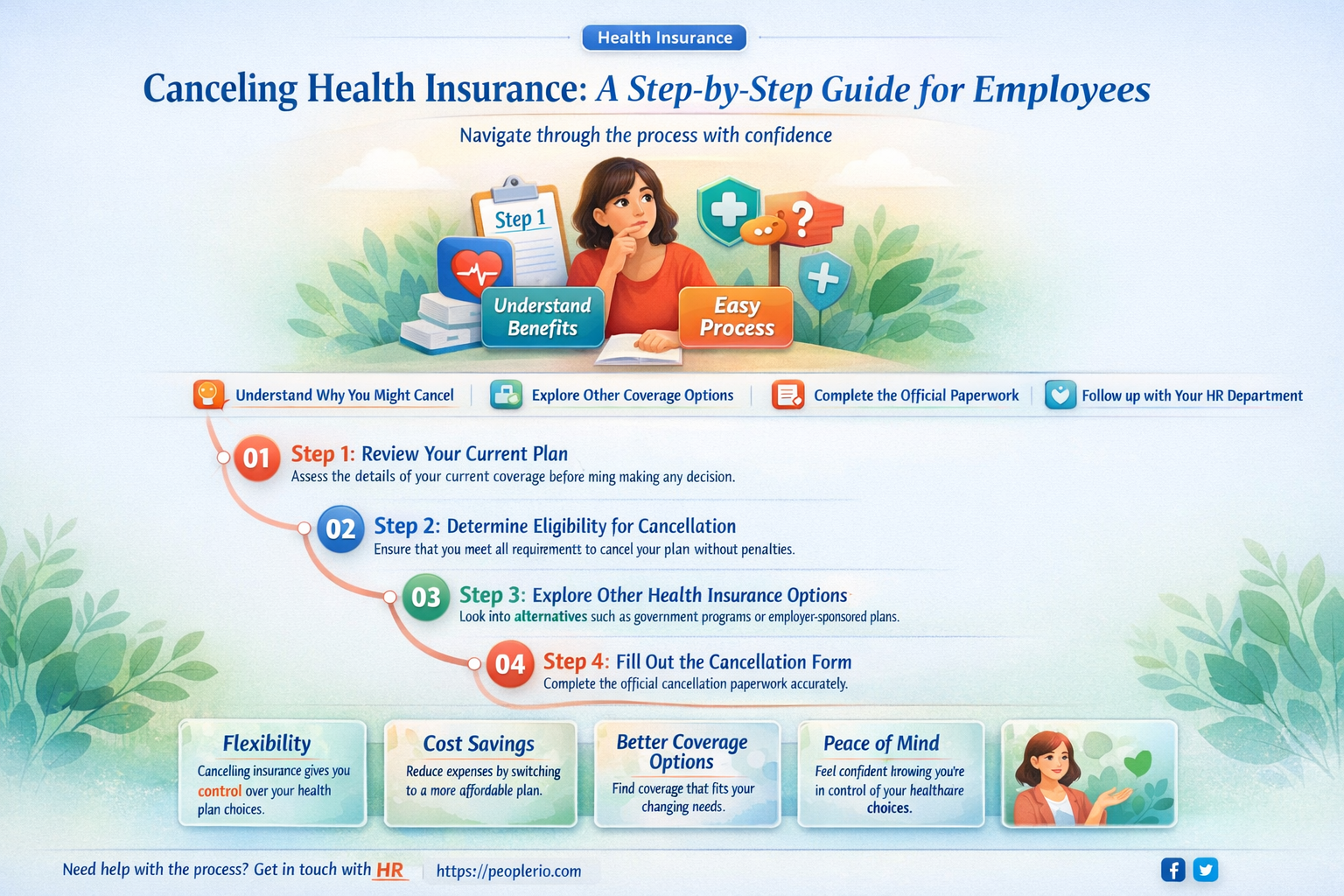

An employee may need to cancel their health insurance for various reasons, such as a change in employment status, eligibility for other coverage, or personal preference. The process typically involves notifying the employer's human resources department or the insurance provider directly, often within a specific timeframe to avoid penalties. It's important for the employee to understand their rights and options, including any potential impacts on their healthcare coverage and financial obligations. They should also be aware of any required documentation and the effective date of the cancellation to ensure a smooth transition.

| Characteristics | Values |

|---|---|

| Cancellation Process | Typically involves contacting the HR department or insurance provider |

| Notice Period | May require a certain notice period, such as 30 days |

| Documentation | Might need to fill out a cancellation form or provide written notice |

| Effective Date | Cancellation becomes effective at the end of the billing cycle or specified date |

| Refund | Could be eligible for a prorated refund depending on the policy |

| Impact on Benefits | Loss of health insurance coverage for the employee and dependents |

| Alternatives | Employee may need to find alternative coverage or enroll in a new plan |

| Employer Notification | Employer must be notified to stop payroll deductions and update records |

| COBRA Rights | Employee may be entitled to temporary continuation of coverage under COBRA |

| State Regulations | Cancellation process may vary based on state insurance regulations |

Explore related products

What You'll Learn

- Understanding Cancellation Policies: Review the employee's health insurance plan to understand the cancellation policy and any penalties

- Qualifying Life Events: Determine if the employee has experienced a qualifying life event that allows for cancellation without penalties

- Open Enrollment Periods: Inform the employee about open enrollment periods when they can switch or cancel their health insurance

- Alternative Coverage Options: Discuss alternative health insurance options available to the employee if they decide to cancel their current plan

- Impact on Benefits: Explain how canceling health insurance might affect the employee's overall benefits package and financial situation

![]()

Understanding Cancellation Policies: Review the employee's health insurance plan to understand the cancellation policy and any penalties

To navigate the complexities of canceling health insurance, it's crucial to first understand the cancellation policies outlined in your employee health insurance plan. This involves a thorough review of the plan documents to grasp any stipulations, timelines, and potential penalties associated with cancellation.

Begin by locating the specific section of your insurance plan that details the cancellation process. This section should outline the steps you need to take to cancel your coverage, including any required notifications to your employer or the insurance provider. Pay close attention to any deadlines or timeframes mentioned, as failing to cancel within the specified period could result in continued premium deductions or other complications.

Next, review the plan for any penalties or fees associated with cancellation. Some plans may impose a penalty for early cancellation, while others may require you to pay back any subsidies or discounts received if you cancel before the end of the plan year. Understanding these potential costs can help you make an informed decision about whether and when to cancel your coverage.

Additionally, consider the impact of canceling your health insurance on your overall financial and health situation. While canceling may save you money on premiums in the short term, it could leave you vulnerable to significant out-of-pocket expenses in the event of unexpected medical needs. Evaluate your current health status, financial stability, and risk tolerance before making a decision.

Finally, if you're unsure about any aspect of the cancellation process or the implications of canceling your coverage, don't hesitate to reach out to your employer's human resources department or the insurance provider directly for clarification. They can provide personalized guidance based on your specific situation and help you make the best decision for your needs.

Walgreens' Role in Employee Health Insurance: A Comprehensive Look

You may want to see also

Explore related products

![]()

Qualifying Life Events: Determine if the employee has experienced a qualifying life event that allows for cancellation without penalties

A qualifying life event is a significant change in an employee's personal circumstances that may necessitate the cancellation of their health insurance without incurring penalties. These events can include, but are not limited to, marriage, divorce, birth or adoption of a child, death of a spouse or dependent, or a change in employment status. It's crucial for employees to understand that they must provide documentation to substantiate the occurrence of such an event. This documentation could be a marriage certificate, divorce decree, birth certificate, or a letter from their employer confirming a change in employment status.

Employees should be aware that there is typically a limited timeframe within which they must request cancellation following a qualifying life event. This period can vary depending on the insurance provider and the specific terms of the policy, but it is often around 30 to 60 days. Missing this window could result in the employee being locked into their current plan until the next open enrollment period.

Furthermore, it's important to note that not all changes in personal circumstances qualify as life events for the purpose of health insurance cancellation. For instance, moving to a new address or changing jobs within the same company may not be considered qualifying events. Employees should carefully review their policy documents or consult with their human resources department to determine what constitutes a qualifying life event under their specific plan.

In some cases, employees may be required to provide additional information or complete certain forms to initiate the cancellation process. This could include details about the new plan they intend to enroll in or confirmation that they have secured alternative coverage. Being proactive and gathering all necessary information in advance can help streamline the process and reduce the risk of delays or complications.

Ultimately, understanding the provisions related to qualifying life events can empower employees to make informed decisions about their health insurance coverage. By staying informed about their rights and responsibilities, employees can navigate the complexities of health insurance cancellation with greater confidence and ease.

Tax Implications of Health Insurance for Contract Employees Explained

You may want to see also

Explore related products

![]()

Open Enrollment Periods: Inform the employee about open enrollment periods when they can switch or cancel their health insurance

Open enrollment periods are a critical time for employees to review and make changes to their health insurance coverage. These periods, which typically occur once a year, provide an opportunity for employees to switch plans, add or remove dependents, or even cancel their coverage altogether. It's essential for employees to be aware of these periods and understand their options to make informed decisions about their health insurance.

During open enrollment, employees should carefully evaluate their current health insurance plan and consider any changes in their personal or financial circumstances that may affect their coverage needs. This could include changes in income, family size, or health status. Employees should also research the available plans and compare the benefits, costs, and provider networks to determine which plan best meets their needs.

To cancel their health insurance, employees must follow the proper procedures during the open enrollment period. This typically involves submitting a cancellation request through their employer's benefits portal or contacting the insurance provider directly. It's important to note that canceling health insurance may have tax implications, and employees should consult with a tax professional before making a decision.

Employers play a crucial role in informing employees about open enrollment periods and providing them with the necessary resources to make informed decisions about their health insurance. This includes distributing information about the available plans, hosting informational sessions, and offering one-on-one consultations with benefits experts. By providing employees with the tools and support they need, employers can help ensure that their workforce has access to the health insurance coverage that best meets their needs.

In conclusion, open enrollment periods are a valuable opportunity for employees to review and make changes to their health insurance coverage. By understanding their options and following the proper procedures, employees can make informed decisions about their health insurance and ensure they have the coverage they need. Employers, in turn, should provide their employees with the necessary resources and support to navigate the open enrollment process successfully.

Exploring Employee Assistance Programs in Health Insurance Plans

You may want to see also

![]()

Alternative Coverage Options: Discuss alternative health insurance options available to the employee if they decide to cancel their current plan

If an employee is considering canceling their current health insurance plan, it's crucial to explore alternative coverage options to ensure continuous protection. One viable alternative is to enroll in a Health Savings Account (HSA) or Health Reimbursement Arrangement (HRA), which can provide tax advantages and flexibility in managing healthcare expenses. These accounts allow employees to set aside pre-tax dollars for qualified medical expenses, offering a cost-effective way to handle out-of-pocket costs.

Another option to consider is purchasing individual health insurance through a private insurer or a health insurance marketplace. This route may offer more comprehensive coverage than an HSA or HRA, but it's essential to carefully compare plans and premiums to find the best fit. Employees should also investigate whether they are eligible for Medicaid or other state-sponsored programs, which can provide affordable coverage for those who meet specific income and residency requirements.

For employees who are part of a large organization, it may be possible to negotiate a group health insurance plan with a different provider. This approach can leverage the collective bargaining power of the workforce to secure more favorable terms and premiums. Additionally, employees should explore whether their employer offers any other benefits, such as dental or vision insurance, that can be purchased separately to supplement their health coverage.

When evaluating alternative health insurance options, employees should carefully consider factors such as coverage limits, deductibles, copays, and provider networks. It's also important to assess the overall cost of each plan, including premiums, out-of-pocket expenses, and potential tax implications. By thoroughly researching and comparing different options, employees can make an informed decision that best meets their healthcare needs and financial situation.

Understanding Florida's Employee Health Care Act: Key Requirements Explained

You may want to see also

![]()

Impact on Benefits: Explain how canceling health insurance might affect the employee's overall benefits package and financial situation

Canceling health insurance can have far-reaching consequences on an employee's overall benefits package and financial situation. One immediate impact is the loss of coverage for medical expenses, which can lead to significant out-of-pocket costs in the event of an illness or injury. This can be particularly devastating for employees with chronic conditions or those who require ongoing medical treatment.

Furthermore, canceling health insurance may also affect an employee's eligibility for other benefits, such as dental and vision coverage, which are often bundled together with health insurance plans. This can result in a decrease in the overall value of the employee's benefits package, making it more difficult for them to attract and retain top talent.

From a financial perspective, canceling health insurance can lead to a decrease in an employee's take-home pay, as they may be required to pay more in taxes and other deductions. This can be a significant blow to employees who are already struggling to make ends meet, and may lead to a decrease in their overall standard of living.

Additionally, canceling health insurance can also have long-term consequences, such as affecting an employee's ability to qualify for future insurance plans or obtain affordable coverage. This can be particularly problematic for employees who may need to seek new employment or start their own business, as they may find it difficult to secure adequate health insurance coverage without a job.

In conclusion, canceling health insurance can have a significant impact on an employee's overall benefits package and financial situation, leading to a decrease in coverage, eligibility for other benefits, take-home pay, and long-term financial security. As such, it is important for employees to carefully consider the potential consequences before making a decision to cancel their health insurance coverage.

Exploring the Entrepreneurial Side of Home Health Employment

You may want to see also

Frequently asked questions

To cancel your health insurance, you typically need to contact your employer's human resources department or the insurance provider directly. You may need to fill out a cancellation form or provide written notice stating your intention to cancel.

Canceling health insurance can leave you without coverage for medical expenses, which can be costly. You may also face penalties or fees for canceling, depending on the terms of your policy. Additionally, you might need to find alternative coverage or enroll in a new plan during the next open enrollment period.

The deadline to cancel health insurance can vary depending on your employer's policies or the terms of your insurance plan. Some plans may allow you to cancel at any time, while others may have specific deadlines or require you to wait until the next open enrollment period. It's best to check with your employer or insurance provider for the exact cancellation policy.