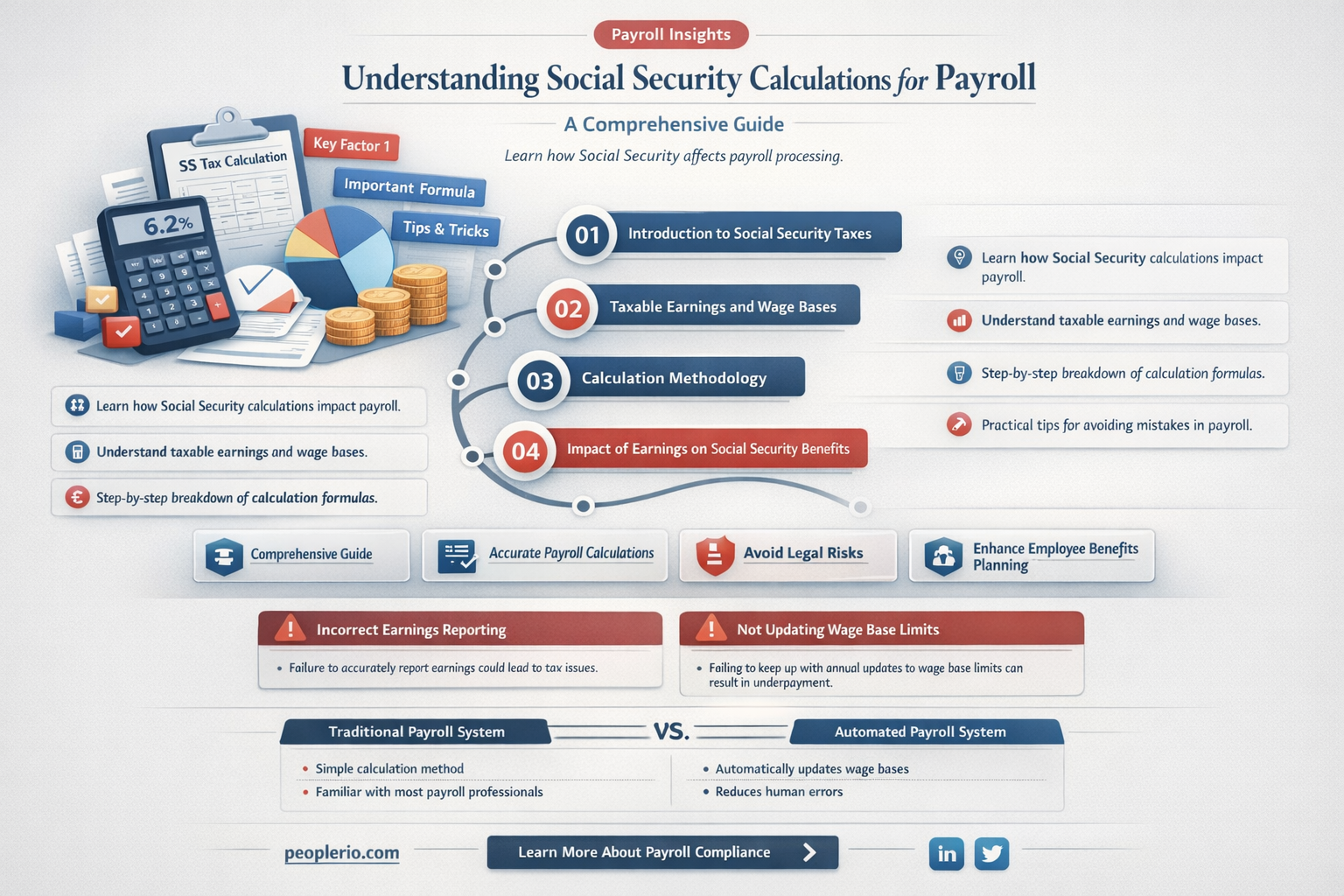

Social Security is a crucial component of payroll calculations in the United States, providing financial security to millions of Americans. The calculation of Social Security for payroll involves a percentage of an employee's gross wages, up to a certain wage base limit. As of 2023, the Social Security tax rate is 6.2% for both employers and employees, and the wage base limit is $147,000. This means that for every dollar an employee earns up to $147,000, 6.2 cents is deducted for Social Security. Employers are responsible for withholding this amount from their employees' paychecks and matching it with an equal contribution. Self-employed individuals must pay both the employee and employer portions of the Social Security tax. Understanding how Social Security is calculated for payroll is essential for both employers and employees to ensure accurate tax withholding and compliance with federal regulations.

| Characteristics | Values |

|---|---|

| Calculation Basis | Employee's gross wages |

| Contribution Rate | 6.2% (employee), 6.2% (employer) |

| Wage Base Limit | $147,000 (2023) |

| Earnings Test | Applies to workers under 62 |

| Benefits Calculation | Average Indexed Monthly Earnings (AIME) |

| Full Retirement Age | 66-67 (varies by birth year) |

| Early Retirement Penalty | Reduced benefits if taken before 62 |

| Survivor Benefits | Available to spouse and children |

| Disability Benefits | Available if unable to work due to disability |

| Taxation of Benefits | Taxable if income exceeds certain thresholds |

Explore related products

What You'll Learn

- Employee Contributions: Percentage of earnings deducted for Social Security taxes

- Employer Contributions: Matching contributions made by employers for each employee

- Taxable Wage Base: Maximum earnings subject to Social Security taxes annually

- Benefit Calculation: How lifetime earnings determine retirement, disability, and survivor benefits

- Self-Employment Taxes: Special considerations and rates for self-employed individuals

![]()

Employee Contributions: Percentage of earnings deducted for Social Security taxes

The calculation of Social Security taxes for payroll involves several key components, with employee contributions being a significant aspect. Employee contributions are calculated as a percentage of their earnings, which is then deducted from their gross pay. This percentage is determined by the Social Security Administration (SSA) and is subject to change annually. For example, in 2023, the employee contribution rate is 6.2% of earnings up to a certain wage base, which is adjusted for inflation each year.

To calculate the employee contribution, employers must first determine the employee's gross wages for the pay period. This includes all forms of compensation, such as salaries, wages, tips, and bonuses. Once the gross wages are established, the employer applies the current Social Security tax rate to calculate the amount to be deducted. For instance, if an employee earns $1,000 in a pay period and the tax rate is 6.2%, the employer would deduct $62 from the employee's paycheck for Social Security taxes.

It's important to note that there is a wage base limit, above which no additional Social Security taxes are deducted. This limit is also adjusted annually by the SSA. For example, in 2023, the wage base limit is $147,000. This means that once an employee's earnings reach this threshold, no further Social Security tax deductions are made for the remainder of the year.

Employers are responsible for accurately calculating and deducting these taxes from their employees' paychecks. They must also match the employee contributions by paying an equal amount into the Social Security system. This matching contribution is an additional cost to the employer and is not deducted from the employee's wages.

In summary, employee contributions for Social Security taxes are calculated as a percentage of their gross earnings, up to a certain wage base limit. Employers are responsible for deducting the correct amount from their employees' paychecks and matching these contributions with their own payments to the Social Security system. Understanding these calculations is crucial for both employers and employees to ensure accurate payroll processing and compliance with federal tax laws.

Calculating Average Monthly Payroll for PPP Loans: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Employer Contributions: Matching contributions made by employers for each employee

Employers play a crucial role in the social security system by making matching contributions for each employee. This means that for every dollar an employee pays into social security, the employer also contributes a dollar, effectively doubling the amount set aside for the employee's future benefits. This system is designed to ensure that both employees and employers share the responsibility of funding retirement, disability, and survivor benefits.

The matching contribution system is a key component of the social security calculation for payroll. Employers are required to withhold a certain percentage of an employee's wages for social security purposes and then match that amount with an equal contribution of their own. The total amount withheld and matched is then sent to the social security administration to fund the employee's benefits.

One important aspect of employer contributions is that they are capped at a certain amount each year. This cap is adjusted annually for inflation, but it means that high-wage earners may not have their full earnings subject to social security withholding and matching. For example, if the cap is set at $147,000 for a given year, then an employee earning $200,000 would only have the first $147,000 of their wages subject to social security withholding and matching.

Employer contributions also play a role in determining the amount of social security benefits an employee will receive upon retirement. The social security administration uses a complex formula to calculate benefits, which takes into account the employee's earnings history, the number of years they worked, and the age at which they retire. Employer contributions are a key factor in this formula, as they help to ensure that employees have a sufficient amount of money set aside to support them in their retirement years.

In addition to funding retirement benefits, employer contributions also help to support disability and survivor benefits. If an employee becomes disabled or passes away, their social security contributions, along with those of their employer, can provide financial support to them or their dependents. This is an important aspect of the social security system, as it helps to protect employees and their families from financial hardship in the event of an unexpected illness or death.

Overall, employer contributions are a vital part of the social security system, helping to ensure that employees have a reliable source of income in their retirement years, as well as providing support in the event of disability or death. By making matching contributions for each employee, employers demonstrate their commitment to the financial well-being of their workforce and help to maintain the stability of the social security system as a whole.

Mastering Payroll Percentages: A Guide to Calculating Deductions for Free

You may want to see also

Explore related products

![]()

Taxable Wage Base: Maximum earnings subject to Social Security taxes annually

The Taxable Wage Base represents the maximum amount of an employee's earnings that are subject to Social Security taxes each year. This figure is crucial for both employers and employees to understand, as it directly impacts the amount of taxes withheld and paid into the Social Security system. For 2023, the Taxable Wage Base is set at $147,000, meaning that any earnings above this threshold are not subject to Social Security taxes.

To calculate the Social Security tax for payroll, employers must first determine the Taxable Wage Base for each employee. This involves reviewing the employee's gross wages and ensuring that the correct amount is used for tax calculations. If an employee's earnings exceed the Taxable Wage Base, the excess amount is not included in the Social Security tax calculations. Employers are responsible for withholding the appropriate amount of Social Security tax from each paycheck and remitting it to the IRS.

It's important to note that the Taxable Wage Base is adjusted annually for inflation, which means that employers must stay up-to-date with the latest figures to ensure compliance with tax laws. Failure to correctly calculate and remit Social Security taxes can result in penalties and fines for employers. Additionally, employees who earn above the Taxable Wage Base may need to make estimated tax payments to cover their Social Security tax liability.

In summary, understanding the Taxable Wage Base is essential for accurate payroll processing and tax compliance. Employers must carefully review employee earnings and apply the correct tax rates to ensure that they are meeting their legal obligations. By staying informed about changes to the Taxable Wage Base and other tax laws, employers can avoid costly mistakes and ensure that their payroll processes are running smoothly.

Mastering Bi-Monthly Payroll Calculations: A Step-by-Step Guide for Employers

You may want to see also

Explore related products

![]()

Benefit Calculation: How lifetime earnings determine retirement, disability, and survivor benefits

The calculation of Social Security benefits is a complex process that takes into account an individual's lifetime earnings. This is because the amount of money one earns throughout their working life directly impacts the amount of retirement, disability, and survivor benefits they are eligible to receive. The Social Security Administration (SSA) uses a formula to calculate these benefits, which involves averaging an individual's highest 35 years of earnings and then applying a percentage to this average to determine the monthly benefit amount.

One unique aspect of this calculation is the indexing of earnings to account for inflation. This means that the SSA adjusts an individual's earnings history to reflect the changes in the cost of living over time. This ensures that the benefits received are based on the purchasing power of the earnings at the time of retirement, disability, or death.

Another important factor in the calculation of benefits is the age at which an individual chooses to retire. The SSA has a full retirement age, which is currently 67 for those born in 1960 or later. If an individual chooses to retire before this age, their benefits will be reduced. Conversely, if they retire after this age, their benefits will be increased.

In addition to retirement benefits, the SSA also provides disability and survivor benefits. Disability benefits are calculated based on an individual's earnings history and the severity of their disability. Survivor benefits are calculated based on the earnings history of the deceased individual and the relationship of the survivor to the deceased.

It is important to note that the calculation of Social Security benefits is subject to change. The SSA periodically reviews and adjusts the formula used to calculate benefits to ensure that it remains fair and accurate. This means that individuals should stay informed about any changes to the Social Security system that may impact their benefits.

Mastering Payroll Hours Calculation in PHP: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Self-Employment Taxes: Special considerations and rates for self-employed individuals

Self-employed individuals face unique considerations when it comes to paying taxes, particularly regarding Social Security. Unlike traditional employees, the self-employed are responsible for both the employer and employee portions of Social Security taxes. This means they must pay a total of 15.3% of their net earnings in Social Security taxes, compared to the 7.65% paid by employees.

One special consideration for the self-employed is the ability to deduct half of their Social Security tax liability from their taxable income. This deduction helps to offset the higher tax burden and is available only to self-employed individuals. Additionally, self-employed individuals may be eligible for a lower Social Security tax rate if their net earnings are below a certain threshold. For example, in 2022, the Social Security tax rate for self-employed individuals with net earnings below $142,800 is 12.4%.

Another important aspect of self-employment taxes is the requirement to make estimated tax payments throughout the year. Self-employed individuals must pay estimated taxes on a quarterly basis to avoid penalties and interest. These payments are based on the individual's expected tax liability for the year and must be made using Form 1040-ES.

Self-employed individuals may also be eligible for certain tax credits, such as the Earned Income Tax Credit (EITC) and the Child Tax Credit. These credits can help to reduce the overall tax burden and are based on factors such as income, family size, and filing status.

In conclusion, self-employed individuals face unique challenges when it comes to paying taxes, particularly regarding Social Security. However, by understanding the special considerations and rates available to them, they can minimize their tax burden and ensure compliance with the IRS.

Calculating Hourly Rates for Semi-Monthly Payroll: A Step-by-Step Guide

You may want to see also

Frequently asked questions

The social security tax rate is typically set by the government and can change annually. Employers and employees each pay a percentage of the employee's wages.

There is a wage base limit that caps the amount of an employee's earnings subject to social security tax. This limit is adjusted annually for inflation.

To calculate the social security tax, multiply the employee's wages by the social security tax rate. The result is the amount withheld from the employee's paycheck for social security.

If an employee's earnings exceed the wage base limit, no additional social security tax is withheld on the excess amount.

Certain types of income and certain individuals may be exempt from paying social security tax. For example, some religious organizations and their members may qualify for an exemption.