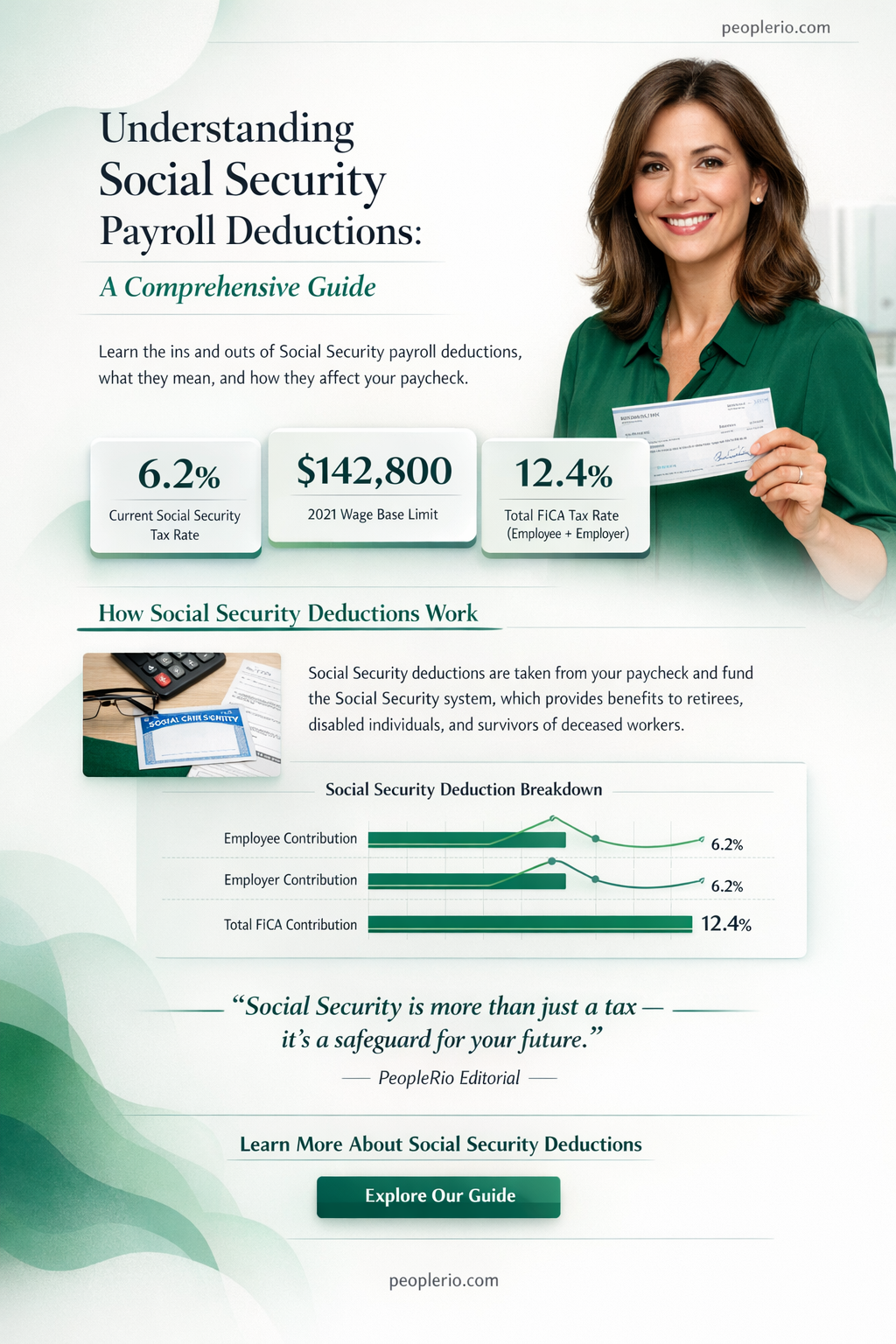

Social Security payroll deductions are calculated based on an employee's gross wages, up to a certain wage base limit. The Social Security Administration (SSA) sets this limit annually, and for 2023, it is $147,000. Employers and employees each pay 6.2% of the employee's gross wages up to this limit. To calculate the deduction, multiply the employee's gross wages by 6.2%. For example, if an employee earns $50,000 per year, their Social Security payroll deduction would be $3,100 (50,000 x 0.062). It's important to note that this calculation is separate from other payroll deductions such as Medicare, federal income tax, and state taxes.

| Characteristics | Values |

|---|---|

| Tax Rate | 6.2% |

| Wage Base Limit | $147,000 (2023) |

| Employer Contribution | 6.2% |

| Employee Contribution | 6.2% |

| Self-Employed Contribution | 15.3% (combined employer and employee rate) |

| Earnings Threshold | $42,000 (2023) for receiving benefits |

| Maximum Monthly Benefit | $3,627 (2023) at full retirement age |

| Full Retirement Age | 66-67 years old (varies by birth year) |

| Early Retirement Age | 62 years old |

| Late Retirement Age | 70 years old |

| Cost-of-Living Adjustments | Annually, based on CPI-W |

| Disability Benefits | Available for workers with qualifying disabilities |

| Survivor Benefits | Available for spouses and children of deceased workers |

| Medicare Part A Coverage | Included for workers with 40 or more quarters of coverage |

Explore related products

What You'll Learn

- Employee Contributions: Calculating the percentage of an employee's earnings subject to Social Security tax

- Employer Contributions: Determining the employer's matching contribution based on employee earnings

- Wage Base Limit: Understanding the maximum earnings subject to Social Security tax annually

- Tax Rate: Applying the current Social Security tax rate to calculate deductions

- Self-Employed Individuals: Calculating Social Security contributions for self-employed individuals based on net earnings

![]()

Employee Contributions: Calculating the percentage of an employee's earnings subject to Social Security tax

To calculate the percentage of an employee's earnings subject to Social Security tax, you need to understand the wage base limit and the tax rate. As of 2023, the Social Security tax rate is 6.2% for both employees and employers. The wage base limit, which is the maximum amount of earnings subject to Social Security tax, is $147,000. This means that any earnings above this limit are not subject to Social Security tax.

For example, if an employee earns $100,000 in a year, the entire amount is subject to Social Security tax. However, if an employee earns $150,000, only $147,000 is subject to tax. To calculate the tax, you would multiply the taxable earnings by the tax rate: $147,000 x 6.2% = $9,114.

It's important to note that the wage base limit is adjusted annually for inflation. In addition, there is a separate Medicare tax that is also deducted from an employee's earnings, which is not subject to the same wage base limit as Social Security tax.

When calculating the percentage of an employee's earnings subject to Social Security tax, it's also important to consider any other factors that may affect their earnings, such as bonuses, overtime, or tips. These types of earnings may be subject to Social Security tax, even if they are not included in the employee's regular salary.

In summary, calculating the percentage of an employee's earnings subject to Social Security tax involves understanding the wage base limit and the tax rate, as well as considering any other factors that may affect their earnings. By following these guidelines, you can ensure that you are accurately calculating the amount of Social Security tax that should be deducted from an employee's earnings.

Calculating Overtime for Semi-Monthly Payroll: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Employer Contributions: Determining the employer's matching contribution based on employee earnings

Employers play a crucial role in the social security system by making matching contributions based on their employees' earnings. This process is integral to funding social security benefits and ensuring the system's sustainability. To determine the employer's matching contribution, a specific formula is applied to the employee's gross wages.

The first step involves identifying the employee's gross earnings for the pay period. Gross earnings include all forms of compensation, such as wages, salaries, bonuses, and tips, before any deductions are made. Once the gross earnings are established, the employer applies the social security tax rate to calculate the matching contribution.

The social security tax rate is set by law and is subject to change. As of the current date, the tax rate is 6.2% for both employers and employees. However, it's essential to verify the current rate, as it may be adjusted periodically. The employer multiplies the employee's gross earnings by the tax rate to determine the amount of the matching contribution.

For example, if an employee earns $1,000 in a pay period, the employer's matching contribution would be $62 (calculated as $1,000 x 0.062). This amount is in addition to the employee's own social security deduction, which would also be $62, resulting in a total social security contribution of $124 for that pay period.

It's important to note that there is a wage base limit for social security contributions. This means that only a certain amount of an employee's earnings are subject to social security tax. The wage base limit is adjusted annually for inflation. Employers must ensure that they are using the correct wage base limit when calculating their matching contributions.

In summary, employers determine their matching social security contribution by applying the current tax rate to their employees' gross earnings, up to the wage base limit. This process is a critical component of the social security system, ensuring that both employers and employees contribute to the funding of benefits.

Calculating Payroll for 30 Minutes: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Wage Base Limit: Understanding the maximum earnings subject to Social Security tax annually

The Wage Base Limit is a critical component in the calculation of Social Security payroll deductions. It represents the maximum amount of an employee's earnings that are subject to Social Security tax each year. As of 2023, this limit is set at $147,000, meaning that any income earned above this threshold is not taxed for Social Security purposes. This limit is adjusted annually for inflation, ensuring that it keeps pace with changes in the cost of living.

Understanding the Wage Base Limit is essential for both employers and employees. For employers, it affects how much they need to withhold from their employees' paychecks and remit to the Social Security Administration. For employees, it impacts the amount of tax they pay and, consequently, the benefits they may receive upon retirement or disability. High earners, in particular, need to be aware of this limit as it can significantly influence their tax liabilities and benefit calculations.

One common misconception is that the Wage Base Limit applies to the total income earned from all sources. However, it specifically pertains to wages, salaries, and tips from employment. Other forms of income, such as investment earnings or self-employment income, are subject to different tax rules and limits. It's also important to note that the Wage Base Limit does not affect the calculation of Medicare taxes, which have their own set of rules and limits.

To illustrate the impact of the Wage Base Limit, consider an employee who earns $150,000 per year. Only the first $147,000 of their earnings would be subject to Social Security tax. This means that the employee would pay Social Security tax on $147,000, while the remaining $3,000 would be exempt from this tax. Employers must ensure that they correctly calculate and withhold the appropriate amount of Social Security tax based on this limit.

In conclusion, the Wage Base Limit is a key factor in determining the amount of Social Security tax that is withheld from an employee's paycheck. It is essential for both employers and employees to understand this limit and how it applies to their specific situations to ensure accurate tax calculations and compliance with Social Security regulations.

Calculating Average Monthly Payroll for PPP: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Tax Rate: Applying the current Social Security tax rate to calculate deductions

To calculate Social Security payroll deductions, the current tax rate is a critical component. As of 2023, the Social Security tax rate stands at 6.2% for both employees and employers. This rate is applied to an employee's gross wages to determine the amount withheld for Social Security purposes. For example, if an employee earns $1,000 in a pay period, the Social Security deduction would be $62 ($1,000 x 0.062).

It's important to note that there is a wage base limit for Social Security taxes. In 2023, this limit is $147,000. This means that once an employee's earnings reach this threshold, no further Social Security taxes are withheld for that year. For high-income earners, this can result in a significant reduction in their overall tax burden.

When calculating deductions, it's also essential to consider any changes to the tax rate or wage base limit that may occur from year to year. These adjustments are typically made to account for inflation and changes in the Social Security system's financial health. Staying up-to-date on these changes is crucial for accurate payroll processing.

In addition to the employee's contribution, employers are also responsible for paying a matching Social Security tax. This means that the total Social Security tax rate for a given pay period is effectively doubled, with both the employee and employer contributing 6.2% each. For self-employed individuals, this rate is even higher, as they are responsible for paying both the employee and employer portions of the tax.

Understanding how the Social Security tax rate is applied to calculate deductions is essential for both employees and employers. It ensures that the correct amount is withheld and paid into the system, helping to maintain the financial stability of the Social Security program and providing workers with the retirement benefits they've earned.

Healthcare Costs: Should They Be Factored into Gross Payroll?

You may want to see also

Explore related products

![]()

Self-Employed Individuals: Calculating Social Security contributions for self-employed individuals based on net earnings

Self-employed individuals face a unique set of challenges when it comes to calculating their Social Security contributions. Unlike employees who have their payroll taxes deducted automatically, self-employed individuals must take on the responsibility of calculating and paying their own Social Security taxes. This process begins with determining net earnings, which is the total income from self-employment activities minus any allowable business deductions.

To calculate Social Security contributions, self-employed individuals must first determine their net earnings for the year. This involves keeping accurate records of all income and expenses related to their self-employment activities. Once net earnings are calculated, the individual must apply the current Social Security tax rate to determine the amount of tax owed. For 2023, the Social Security tax rate for self-employed individuals is 15.3% of net earnings up to $147,000. Any earnings above this threshold are not subject to Social Security tax.

One important consideration for self-employed individuals is the potential for underpaying or overpaying their Social Security taxes. Underpaying can lead to penalties and interest, while overpaying may result in a larger tax refund. To avoid these issues, self-employed individuals should make estimated tax payments throughout the year based on their projected net earnings. These payments can be made quarterly using Form 1040-ES, which helps to ensure that the individual is paying the correct amount of tax as their earnings fluctuate throughout the year.

Another factor that self-employed individuals should be aware of is the impact of their business structure on their Social Security contributions. For example, if an individual is operating as a sole proprietor, all of their net earnings are subject to Social Security tax. However, if they are operating as an S corporation, only the wages they pay themselves are subject to Social Security tax, while any additional profits are not. This can provide a significant tax advantage for self-employed individuals who are able to structure their business in this way.

In conclusion, calculating Social Security contributions for self-employed individuals requires careful attention to detail and an understanding of the relevant tax laws and regulations. By keeping accurate records, making estimated tax payments, and considering the impact of their business structure, self-employed individuals can ensure that they are paying the correct amount of Social Security tax and avoiding potential penalties and interest.

Calculating Sales-to-Payroll Percentage: A Comprehensive Guide

You may want to see also

Frequently asked questions

The Social Security payroll deduction rate for employees is 6.2% of their gross wages.

Yes, there is a maximum amount of earnings subject to Social Security tax, known as the wage base. For 2023, the wage base is $147,000.

The Social Security payroll deduction is calculated by multiplying the employee's gross wages by the Social Security tax rate (6.2%). For example, if an employee earns $1,000, the Social Security deduction would be $62.

Yes, employers also pay Social Security taxes. The employer's Social Security tax rate is 6.2% of the employee's gross wages, up to the wage base. This means that for every $1,000 an employee earns, the employer also pays $62 in Social Security taxes.