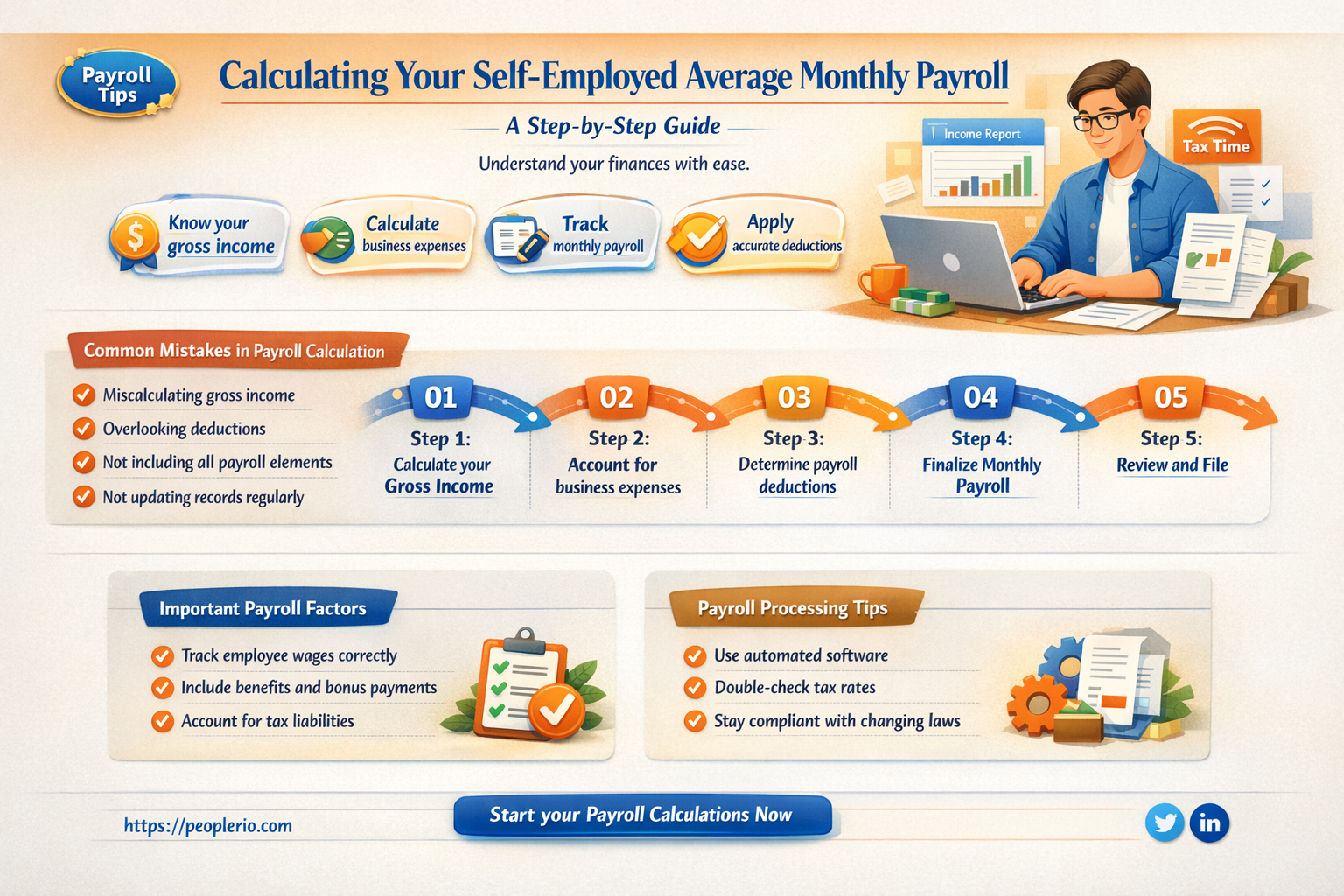

Calculating the average monthly payroll for self-employed individuals involves understanding one's total annual income and dividing it by the number of months in a year. Start by determining your gross income, which includes all earnings before taxes and deductions. This figure can be obtained from your tax returns or by adding up all your monthly earnings over the year. Next, consider any business expenses that can be deducted from your gross income to arrive at your net income. Once you have your net income, divide it by 12 to get your average monthly payroll. It's important to note that this calculation may not account for fluctuations in income or irregular pay periods, so adjustments may be necessary for a more accurate representation.

Explore related products

What You'll Learn

- Determine Monthly Income: Calculate total earnings from all sources before deductions

- Identify Allowable Deductions: Recognize expenses that can be subtracted from gross income

- Calculate Net Income: Subtract deductions from gross income to find net pay

- Account for Taxes: Estimate and set aside funds for self-employment taxes

- Track and Adjust: Regularly review and adjust calculations for accuracy and changes

![]()

Determine Monthly Income: Calculate total earnings from all sources before deductions

To determine your monthly income as a self-employed individual, you must first gather all relevant financial information. This includes earnings from your primary business, any side gigs or freelance work, rental income, investments, and any other sources of revenue. Once you have this information, you can begin to calculate your total earnings before deductions.

Start by listing all of your income sources and the corresponding amounts. For example, if you have a business that generates $5,000 per month, a side gig that earns you $1,000, and rental income of $2,000, your total earnings before deductions would be $8,000. It's important to be thorough and include all sources of income, no matter how small, to get an accurate picture of your monthly earnings.

Next, you'll need to consider the frequency of each income source. If you receive payments weekly, bi-weekly, or quarterly, you'll need to adjust the amounts to reflect a monthly average. For instance, if you earn $2,000 per quarter from a freelance project, you would divide that amount by three to get a monthly average of approximately $667.

Once you have your total monthly earnings, you can begin to plan for deductions such as taxes, health insurance, and retirement savings. It's important to set aside a portion of your income for these expenses to avoid any surprises come tax season or when unexpected medical bills arise.

In summary, determining your monthly income as a self-employed individual requires gathering information from all income sources, calculating the total earnings, and adjusting for the frequency of payments. This process is crucial for accurate financial planning and ensuring you're prepared for deductions and unexpected expenses.

Simplify Payroll Processing: Discover Programs That Calculate Payroll for You

You may want to see also

Explore related products

![]()

Identify Allowable Deductions: Recognize expenses that can be subtracted from gross income

To accurately calculate your average monthly payroll as a self-employed individual, it's crucial to identify allowable deductions that can be subtracted from your gross income. This step is essential because it helps you determine your net income, which is the amount you'll use to calculate your payroll. Allowable deductions are expenses that the tax authorities permit you to deduct from your gross income, reducing your taxable income and potentially lowering your tax liability.

Some common allowable deductions for self-employed individuals include business expenses such as office supplies, equipment, and utilities; travel expenses related to your business; health insurance premiums; and contributions to retirement plans. It's important to keep detailed records of these expenses throughout the year to ensure you can accurately calculate your deductions when it's time to file your taxes.

When identifying allowable deductions, it's also important to be aware of any limitations or restrictions that may apply. For example, some deductions may be subject to caps or may only be allowable if they exceed a certain threshold. Additionally, certain expenses may not be deductible at all, such as personal expenses or expenses that are not directly related to your business.

To ensure you're taking advantage of all the allowable deductions available to you, it's a good idea to consult with a tax professional or use tax preparation software that can help you identify and calculate your deductions. This can help you maximize your tax savings and ensure you're accurately calculating your average monthly payroll.

In summary, identifying allowable deductions is a critical step in calculating your average monthly payroll as a self-employed individual. By understanding what expenses you can deduct from your gross income and keeping accurate records, you can reduce your taxable income, lower your tax liability, and ensure you're accurately calculating your payroll.

Understanding Payroll Withholdings: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Calculate Net Income: Subtract deductions from gross income to find net pay

To calculate net income, the first step is to identify your gross income. This is the total amount of money you've earned before any deductions are taken out. For the self-employed, this can include income from various sources such as client payments, sales, or rental income. Once you have your gross income figure, you're ready to move on to the next step.

The next step in calculating net income is to subtract all applicable deductions from your gross income. These deductions can include taxes, insurance premiums, retirement contributions, and any other expenses that are directly related to your business. It's important to keep accurate records of all your deductions, as this will make it easier to calculate your net income and ensure that you're not overpaying or underpaying your taxes.

One common mistake that self-employed individuals make when calculating their net income is failing to account for all of their deductions. This can lead to an inaccurate net income figure, which can have serious consequences when it comes to tax time. To avoid this mistake, it's a good idea to consult with a tax professional or use accounting software to help you keep track of your deductions.

Another important consideration when calculating net income is the timing of your deductions. Some deductions, such as taxes, may need to be made on a quarterly or monthly basis, while others, such as retirement contributions, may be made annually. It's important to understand the timing of your deductions and factor this into your net income calculations.

Finally, it's important to remember that your net income is not the same as your take-home pay. Your take-home pay is the amount of money you actually receive after all deductions have been taken out. Your net income, on the other hand, is the amount of money you've earned after deductions, but before you've actually received it. This distinction is important because it can affect your budgeting and financial planning.

In conclusion, calculating net income is an essential part of managing your finances as a self-employed individual. By following these steps and avoiding common mistakes, you can ensure that you have an accurate net income figure and make informed financial decisions.

Mastering Fringe Benefits Calculation for Certified Payroll Compliance

You may want to see also

Explore related products

![]()

Account for Taxes: Estimate and set aside funds for self-employment taxes

As a self-employed individual, it's crucial to account for taxes accurately to avoid any surprises during tax season. Estimating and setting aside funds for self-employment taxes is a key component of managing your finances effectively. This involves understanding your tax obligations, calculating the appropriate amounts, and developing a system to ensure timely payments.

To begin, familiarize yourself with the self-employment tax rate, which typically includes Social Security and Medicare taxes. For 2023, the self-employment tax rate is 15.3% of your net earnings. This rate may change over time, so it's essential to stay updated on the current tax laws and rates.

Next, calculate your estimated annual self-employment tax liability based on your projected net income. You can use the IRS's Self-Employment Tax Rate Calculator or consult with a tax professional to get an accurate estimate. Once you have this figure, divide it by 12 to determine your monthly tax obligation.

To ensure you're setting aside enough funds, consider using the estimated monthly tax amount as a benchmark. You can set up a separate savings account specifically for your self-employment taxes and transfer the calculated amount into this account each month. This will help you avoid the temptation to spend the funds on other expenses and ensure that you have the necessary funds available when it's time to file your taxes.

Additionally, consider making quarterly estimated tax payments to the IRS. This can help you avoid underpayment penalties and spread out your tax liability over the course of the year. You can use Form 1040-ES to make these payments and consult with a tax professional to determine the appropriate payment schedule for your specific situation.

In conclusion, accounting for self-employment taxes requires careful planning and attention to detail. By estimating your tax liability, setting aside funds each month, and making quarterly payments, you can avoid financial stress and ensure compliance with tax laws. Remember to stay informed about changes in tax rates and laws, and consider seeking guidance from a tax professional if you're unsure about any aspect of your self-employment taxes.

Understanding Payroll Workers' Comp Reports: A Calculation Guide

You may want to see also

Explore related products

![]()

Track and Adjust: Regularly review and adjust calculations for accuracy and changes

To ensure the accuracy of your average monthly payroll calculations as a self-employed individual, it's crucial to establish a routine for tracking and adjusting your figures. This involves setting aside time each month to review your income and expenses, and making any necessary adjustments to your calculations. By doing so, you can identify and correct any errors or discrepancies, and ensure that your financial records are up-to-date and accurate.

One effective way to track and adjust your calculations is to use a spreadsheet or accounting software. These tools allow you to easily input and organize your financial data, and can automatically calculate your average monthly payroll based on the information you provide. Additionally, they can help you identify trends and patterns in your income and expenses, which can inform your financial planning and decision-making.

When reviewing your calculations, it's important to consider any changes in your business or personal circumstances that may affect your income or expenses. For example, if you've taken on new clients or projects, or if you've experienced a decrease in business, you'll need to adjust your calculations accordingly. Similarly, if you've had any changes in your personal life, such as a move or a change in marital status, these may also impact your financial situation and require adjustments to your payroll calculations.

To avoid errors and ensure accuracy, it's also important to double-check your calculations and verify the information you're using. This may involve reviewing your bank statements, invoices, and receipts to ensure that all of your income and expenses are accounted for. By taking the time to track and adjust your calculations regularly, you can maintain accurate financial records and make informed decisions about your business and personal finances.

Mastering Payroll: A Step-by-Step Guide to Annual Calculations

You may want to see also

Frequently asked questions

To determine your monthly income as a self-employed individual, you'll need to calculate your total earnings from all sources, including any business income, freelance work, or side gigs. This can be done by reviewing your bank statements, invoices, and any other financial records you maintain. Once you have your total earnings, divide that number by 12 to get your average monthly income.

As a self-employed individual, you're eligible to deduct certain business expenses from your income. These can include things like office supplies, equipment purchases, travel expenses, and home office costs. Keep detailed records of all your business-related expenses, and consult with a tax professional to ensure you're taking advantage of all the deductions available to you.

If you have employees, calculating your average monthly payroll is a bit more complex. You'll need to add up the total amount you pay your employees each month, including salaries, wages, and any benefits or bonuses. Then, divide that number by the total number of employees you have to get your average monthly payroll per employee.