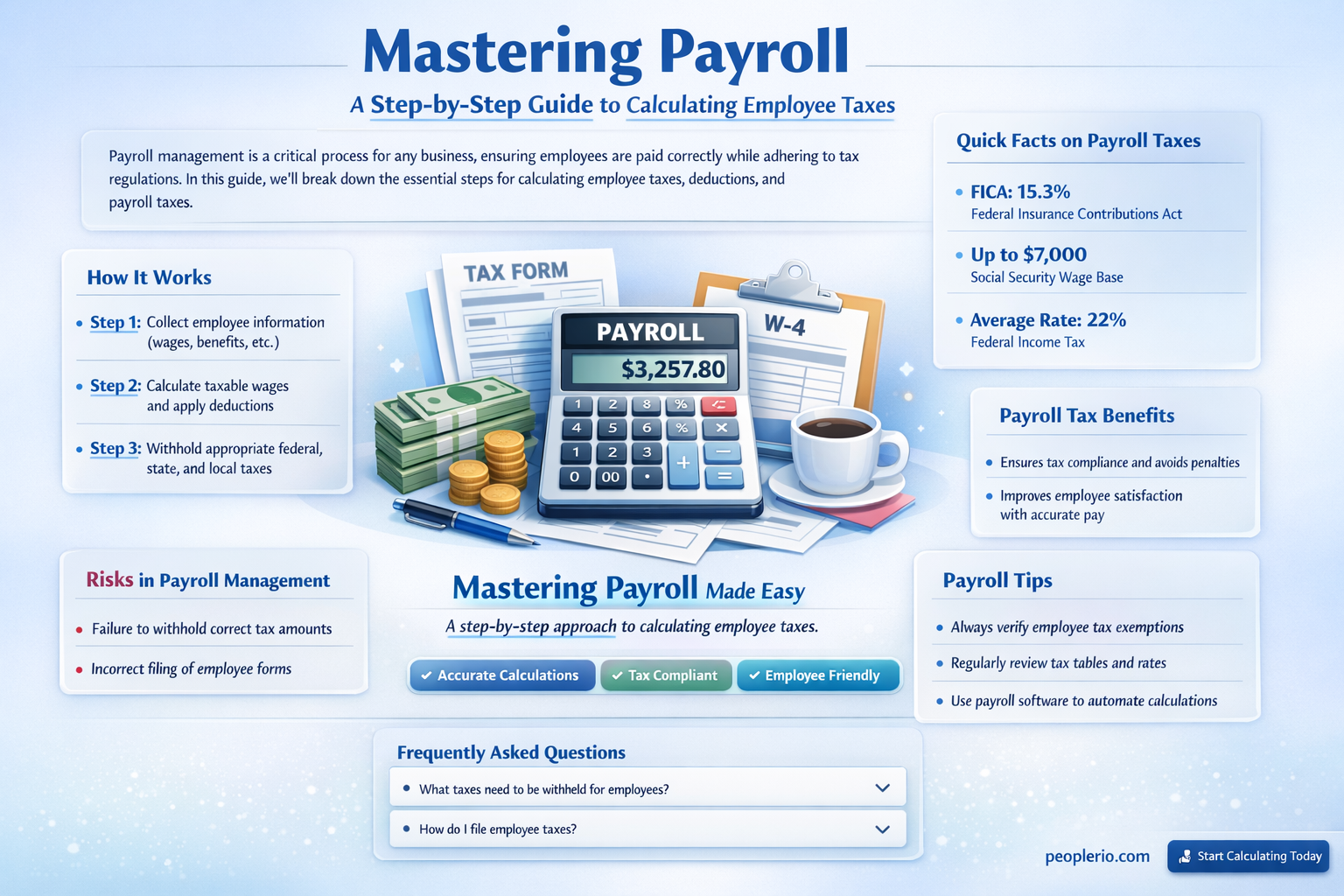

Calculating employee taxes is a crucial aspect of payroll management for any business. It involves understanding various tax regulations and accurately determining the amount of taxes to be withheld from an employee's wages. This process includes federal income tax, Social Security tax, Medicare tax, and potentially state and local taxes, depending on the jurisdiction. Employers must also consider factors such as tax brackets, deductions, and exemptions when calculating these taxes. Accurate tax calculations are essential to ensure compliance with tax laws and to avoid penalties for both the employer and the employee.

| Characteristics | Values |

|---|---|

| Federal Income Tax | Calculate based on federal tax brackets and withholding rates |

| State Income Tax | Varies by state, calculate based on state tax rates |

| Social Security Tax | 6.2% of gross wages, up to annual wage base limit |

| Medicare Tax | 1.45% of gross wages, no wage base limit |

| Additional Medicare Tax | 0.9% of gross wages over $200,000 |

| Unemployment Tax | Varies by state, calculate based on state unemployment tax rates |

| Workers' Compensation Insurance | Varies by state, calculate based on state workers' compensation insurance rates |

| Health Insurance Premiums | Deduct employee portion of health insurance premiums |

| Retirement Contributions | Deduct employee contributions to retirement plans |

| Other Deductions | May include deductions for dependent care, transportation, and other expenses |

| Tax Filing Frequency | Typically quarterly or annually, depending on employer's preference |

| Tax Payment Methods | Electronic payment, check, or other methods accepted by tax authorities |

Explore related products

What You'll Learn

- Understanding Tax Brackets: Learn how different income levels are taxed at varying rates

- Calculating Federal Income Tax: Use IRS tables or software to compute federal tax withholdings

- State and Local Taxes: Account for additional taxes based on state and locality

- Social Security and Medicare: Calculate contributions for these programs based on gross income

- Tax Deductions and Credits: Adjust taxable income with standard or itemized deductions and applicable tax credits

![]()

Understanding Tax Brackets: Learn how different income levels are taxed at varying rates

Tax brackets are a fundamental concept in understanding how employee taxes are calculated. Essentially, tax brackets are ranges of income that are taxed at different rates. As an employee's income increases, they move into higher tax brackets, which means a larger portion of their income is subject to taxation.

For instance, let's consider the federal income tax brackets in the United States for a single filer in 2023. The first tax bracket is 10% and applies to incomes up to $10,275. The second bracket is 12% and applies to incomes between $10,276 and $41,775. As income rises, the tax rate increases, with the highest bracket being 37% for incomes above $539,900.

To calculate employee taxes, it's crucial to understand which tax bracket the employee falls into based on their income. This will determine the percentage of their income that is withheld for federal income tax. Additionally, employees may also be subject to state and local income taxes, which have their own tax brackets and rates.

One common mistake employees make is not adjusting their tax withholdings when their income changes. If an employee receives a raise or a bonus, they may need to adjust their withholdings to ensure they are paying the correct amount of taxes. Failure to do so could result in owing a large sum of money to the IRS at tax time.

In conclusion, understanding tax brackets is essential for employees to accurately calculate their taxes and avoid potential financial penalties. By familiarizing themselves with the tax brackets and rates, employees can make informed decisions about their tax withholdings and ensure they are paying the correct amount of taxes throughout the year.

Understanding the I-9 Tax Form: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Calculating Federal Income Tax: Use IRS tables or software to compute federal tax withholdings

To calculate federal income tax withholdings, employers must use the IRS tables or software, which provide a systematic approach to determining the correct amount of tax to withhold from an employee's wages. The first step is to obtain the necessary information from the employee, including their social security number, filing status, and number of allowances claimed on their W-4 form. This information is crucial for accurately calculating the tax withholdings.

Once the employer has the required information, they can use the IRS tables to determine the tax withholding amount based on the employee's wages and the tax rate applicable to their income bracket. The tables are updated annually by the IRS to reflect changes in tax laws and rates. Employers must use the most current tables to ensure accurate tax withholdings.

Alternatively, employers can use tax withholding software, which automates the calculation process and reduces the risk of errors. These software programs are designed to comply with IRS regulations and can handle complex tax scenarios, such as employees with multiple jobs or those who are subject to additional tax withholdings.

It is important to note that employers are responsible for accurately calculating and withholding federal income tax from their employees' wages. Failure to do so can result in penalties and fines from the IRS. Therefore, it is essential to stay up-to-date with the latest tax laws and regulations and to use the appropriate tools and resources to ensure accurate tax withholdings.

In addition to federal income tax withholdings, employers must also consider other types of tax withholdings, such as state and local income tax, social security tax, and Medicare tax. Each of these taxes has its own set of rules and regulations, and employers must be familiar with them to ensure compliance.

Overall, calculating federal income tax withholdings is a critical aspect of payroll management. Employers must use the IRS tables or software to accurately determine the tax withholding amount and ensure compliance with federal tax laws. By doing so, they can avoid penalties and fines and provide their employees with accurate tax information.

Understanding Social Security Employee Tax: A Comprehensive Guide

You may want to see also

Explore related products

![]()

State and Local Taxes: Account for additional taxes based on state and locality

Calculating employee taxes involves more than just federal taxes; it also requires careful consideration of state and local taxes. These additional taxes can vary significantly depending on the employee's location, making it essential for employers to understand and account for them accurately.

To begin with, employers must identify which state and local taxes apply to their employees. This typically includes income taxes, but may also encompass other levies such as sales taxes, property taxes, or even local service charges. Once the applicable taxes are determined, the next step is to calculate the amount owed. This process can be complex, as tax rates and rules differ widely between jurisdictions. Employers may need to consult state and local tax codes or seek guidance from tax professionals to ensure accurate calculations.

One common approach to managing state and local taxes is to use a tax withholding system. This involves deducting the estimated tax amount from the employee's paycheck and remitting it to the appropriate tax authority. Employers must be cautious when setting up withholding systems, as they need to account for varying tax rates, exemptions, and deductions that may apply to different employees.

In addition to withholding, employers may also need to consider other tax-related responsibilities, such as reporting and filing requirements. These can include submitting tax returns, providing employees with tax forms, and maintaining accurate records of tax payments and deductions. Failure to comply with these requirements can result in penalties and fines, so it's crucial for employers to stay on top of their tax obligations.

To simplify the process of calculating and managing state and local taxes, many employers turn to tax software or outsourcing services. These tools can help automate tax calculations, ensure compliance with tax laws, and reduce the risk of errors or penalties. However, it's important for employers to carefully evaluate these options and choose a solution that meets their specific needs and budget.

In conclusion, accounting for state and local taxes is a critical component of calculating employee taxes. Employers must be diligent in understanding and complying with the tax laws of their employees' jurisdictions, and should consider using tax software or outsourcing services to streamline the process and minimize errors. By taking a proactive approach to managing state and local taxes, employers can ensure accurate tax calculations and avoid potential legal and financial issues.

Understanding Employee Stock Options: Tax Implications and Strategies

You may want to see also

Explore related products

![]()

Social Security and Medicare: Calculate contributions for these programs based on gross income

To calculate contributions for Social Security and Medicare based on gross income, you need to apply specific tax rates to the employee's earnings. For Social Security, the tax rate is 6.2% of gross income, up to a certain wage base limit which changes annually. For Medicare, the tax rate is 1.45% of gross income, with no wage base limit.

First, determine the employee's gross income for the pay period. This includes all earnings before any deductions or taxes are taken out. Next, apply the Social Security tax rate of 6.2% to the gross income, but only up to the wage base limit. For example, if the wage base limit is $147,000 and the employee earns $150,000, you would only apply the Social Security tax to the first $147,000.

After calculating the Social Security contribution, apply the Medicare tax rate of 1.45% to the entire gross income. There is no wage base limit for Medicare, so the tax is applied to all earnings. For instance, if an employee earns $50,000, the Medicare contribution would be $725 ($50,000 x 1.45%).

It's important to note that these rates are subject to change, and there may be additional considerations for certain employees, such as those who are self-employed or who have multiple jobs. Always check the latest IRS guidelines and tax tables for the most up-to-date information.

In summary, calculating Social Security and Medicare contributions involves applying specific tax rates to an employee's gross income, with attention to wage base limits and other special considerations. By following these steps and staying informed about current tax laws, you can ensure accurate and compliant payroll processing.

Understanding Medicare Employee Additional Tax: A Comprehensive Guide

You may want to see also

![]()

Tax Deductions and Credits: Adjust taxable income with standard or itemized deductions and applicable tax credits

To calculate employee taxes accurately, it's crucial to understand how tax deductions and credits adjust taxable income. Tax deductions reduce the amount of income subject to tax, while tax credits directly reduce the tax liability. Employees can choose between standard deductions and itemized deductions, depending on which provides a greater tax benefit.

Standard deductions are a fixed amount set by the tax authority and vary based on filing status, such as single, married filing jointly, or head of household. For example, in the United States, the standard deduction for a single filer in 2022 is $12,950. Itemized deductions, on the other hand, require detailed record-keeping and include expenses such as mortgage interest, property taxes, medical expenses, and charitable contributions. Employees should compare their total itemized deductions to the standard deduction to determine which is more advantageous.

Tax credits are another important aspect of adjusting taxable income. Credits such as the Earned Income Tax Credit (EITC), Child Tax Credit, and Dependent Care Credit can significantly reduce tax liability. For instance, the EITC is a refundable credit for low- to moderate-income workers and can be substantial, depending on income and family size. To claim these credits, employees must meet specific eligibility criteria and provide necessary documentation.

When calculating employee taxes, it's essential to consider the impact of deductions and credits on overall tax liability. By understanding and applying these adjustments correctly, employees can minimize their tax burden and potentially receive a larger refund. It's recommended to consult with a tax professional or use reputable tax software to ensure accurate calculations and compliance with tax laws.

Understanding California Disability Employee Tax: A Comprehensive Guide

You may want to see also

Frequently asked questions

The different types of taxes that need to be calculated for employees include federal income tax, state income tax, local income tax, Social Security tax, and Medicare tax.

Federal income tax is calculated based on the employee's gross income, filing status, and the number of allowances claimed on their W-4 form. You can use the IRS's withholding tables to determine the amount of federal income tax to withhold from each paycheck.

The W-4 form is used to determine the amount of federal income tax to withhold from an employee's paycheck. It takes into account the employee's filing status, the number of allowances they claim, and any additional withholding they request.

Employee taxes need to be calculated and remitted on a regular basis, typically with each paycheck. The frequency of paychecks can vary depending on the company's pay schedule, but common frequencies include weekly, bi-weekly, semi-monthly, and monthly.