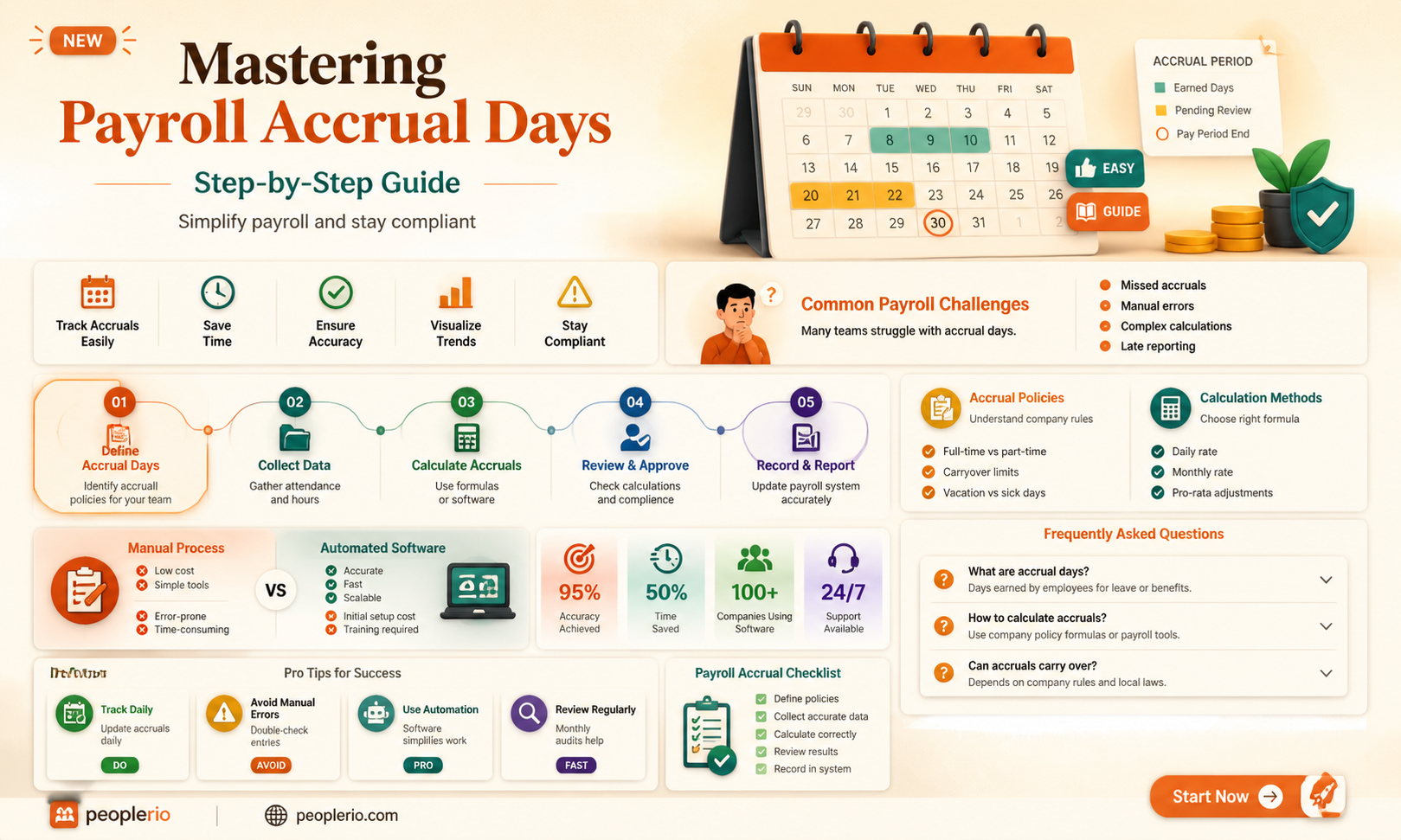

Calculating payroll accrual days is an essential task for businesses to ensure accurate compensation for their employees. Payroll accrual refers to the amount of wages or salaries that have been earned by employees but not yet paid out. Accrual days represent the number of days for which an employee has earned wages that are pending payment. To calculate these days, you need to understand the pay period, the employee's work schedule, and any applicable overtime or leave policies. This involves determining the start and end dates of the pay period, counting the number of days worked, and adjusting for any partial days or unpaid leave. By accurately calculating payroll accrual days, businesses can maintain proper financial records, comply with labor laws, and avoid discrepancies in employee compensation.

Explore related products

What You'll Learn

- Understanding Payroll Accrual: Definition and importance of payroll accrual in accounting

- Identifying Accrual Period: Determining the time frame for which payroll is accrued

- Calculating Daily Accrual: Method to compute the daily payroll accrual amount

- Factors Affecting Accrual: Considerations like overtime, bonuses, and deductions that impact accrual

- Recording Accrual in Books: Proper bookkeeping practices to record payroll accruals accurately

![]()

Understanding Payroll Accrual: Definition and importance of payroll accrual in accounting

Payroll accrual is a fundamental concept in accounting that refers to the expenses incurred by a company for employee wages and salaries that have not yet been paid. This accrual is typically recorded at the end of an accounting period, such as a month or quarter, to ensure that the financial statements accurately reflect the company's liabilities and expenses. Understanding payroll accrual is crucial for businesses to maintain accurate financial records, comply with tax regulations, and effectively manage their cash flow.

The importance of payroll accrual lies in its ability to provide a more accurate picture of a company's financial health. By recognizing the wages and salaries that have been earned but not yet paid, companies can better assess their current liabilities and make informed decisions about their financial planning and budgeting. Payroll accrual also helps in smoothing out fluctuations in cash flow, as it ensures that employee compensation is accounted for consistently across different accounting periods.

To calculate payroll accrual, companies need to determine the amount of wages and salaries that have been earned by employees but not yet paid. This can be done by tracking the number of hours worked by employees and multiplying it by their hourly rates, or by using a salary accrual method for salaried employees. The accrual amount is then recorded as an expense on the income statement and as a liability on the balance sheet.

One common mistake that businesses make when calculating payroll accrual is failing to account for all the components of employee compensation, such as overtime, bonuses, and benefits. It is essential to include all these elements in the accrual calculation to ensure accuracy and compliance with accounting standards. Additionally, companies should regularly review and adjust their payroll accrual processes to reflect any changes in employee compensation or company policies.

In conclusion, understanding payroll accrual is vital for businesses to maintain accurate financial records, comply with tax regulations, and effectively manage their cash flow. By recognizing the wages and salaries that have been earned but not yet paid, companies can better assess their current liabilities and make informed decisions about their financial planning and budgeting.

Calculating Average Monthly Payroll for PPP: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Identifying Accrual Period: Determining the time frame for which payroll is accrued

To accurately calculate payroll accrual days, it is essential to first identify the accrual period. This is the specific time frame for which payroll is accrued, and it can vary depending on the company's payroll schedule and policies. The accrual period is typically a month, but it could also be a week, bi-week, or any other defined period.

The accrual period is determined by the company's payroll cycle and the frequency of employee payments. For example, if a company has a bi-weekly payroll schedule, the accrual period would be two weeks. This means that payroll is accrued for the two-week period ending on the payroll date.

It is important to note that the accrual period is not necessarily the same as the pay period. The pay period is the time frame for which employees are paid, while the accrual period is the time frame for which payroll is accrued. For example, if a company has a bi-weekly pay period, the accrual period could still be a month.

To determine the accrual period, companies should review their payroll policies and procedures. This information is typically outlined in the employee handbook or payroll manual. If the accrual period is not clearly defined, it may be necessary to consult with a payroll specialist or accountant to ensure accurate calculations.

Once the accrual period is identified, it is used to calculate the number of payroll accrual days. This is done by counting the number of days in the accrual period and then dividing by the number of days in the pay period. For example, if the accrual period is a month and the pay period is bi-weekly, there would be approximately 15 payroll accrual days (30 days in the month divided by 2 days in the pay period).

In conclusion, identifying the accrual period is a critical step in calculating payroll accrual days. By understanding the company's payroll schedule and policies, and by clearly defining the accrual period, companies can ensure accurate and efficient payroll processing.

Mastering Payroll Expense Calculations: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Calculating Daily Accrual: Method to compute the daily payroll accrual amount

To calculate the daily payroll accrual amount, you need to understand the concept of accrual accounting. This method recognizes expenses and revenues when they are incurred, regardless of when the cash transaction occurs. In the context of payroll, daily accrual involves determining the portion of an employee's salary or wages that is earned each day.

The first step in calculating daily accrual is to determine the total number of working days in a pay period. This could be weekly, bi-weekly, or monthly, depending on your company's payroll schedule. For example, if you have a weekly pay period, there are typically 5 working days.

Next, you need to calculate the daily rate of pay for each employee. This is done by dividing the total pay for the period by the number of working days. For instance, if an employee earns $1,000 per week, their daily rate of pay would be $1,000 divided by 5, which equals $200 per day.

Once you have the daily rate of pay, you can calculate the daily accrual amount by multiplying this rate by the number of days worked. For example, if an employee works 3 days in a week, their daily accrual amount would be $200 multiplied by 3, resulting in $600.

It's important to note that daily accrual calculations can become more complex when dealing with variable pay rates, overtime, or partial days worked. In such cases, you may need to adjust the calculations accordingly to ensure accurate payroll accrual.

By following these steps, you can effectively calculate the daily payroll accrual amount, which is crucial for maintaining accurate financial records and ensuring timely payment to employees.

Calculating Payroll for Tipped Employees: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Factors Affecting Accrual: Considerations like overtime, bonuses, and deductions that impact accrual

To accurately calculate payroll accrual days, it's crucial to understand the various factors that can affect accrual. These factors include overtime, bonuses, and deductions, which can significantly impact the final accrual amount.

Overtime is a key consideration, as it can increase the total hours worked and, consequently, the accrual amount. Employers must ensure that they are correctly tracking and compensating for overtime hours in accordance with labor laws and regulations. This may involve calculating overtime pay at a higher rate than regular pay, which can affect the overall accrual.

Bonuses can also impact accrual, as they may be considered part of an employee's total compensation. Depending on the bonus structure, it may be necessary to prorate the bonus amount over the accrual period to ensure accurate calculation. This can be particularly complex if the bonus is tied to specific performance metrics or if it varies from year to year.

Deductions, such as taxes, benefits, and garnishments, can reduce the total accrual amount. Employers must ensure that they are correctly withholding and remitting these deductions to avoid penalties and ensure compliance with tax laws. Additionally, some deductions may be voluntary, such as contributions to a retirement plan, which can also affect the accrual calculation.

To effectively manage these factors, employers should maintain accurate and up-to-date records of employee hours, pay, and deductions. This may involve using payroll software or working with a payroll provider to ensure that all calculations are correct and compliant with relevant laws and regulations. By taking these factors into account, employers can ensure that they are accurately calculating payroll accrual days and providing their employees with the correct compensation.

Calculating Overtime for Semi-Monthly Payroll: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Recording Accrual in Books: Proper bookkeeping practices to record payroll accruals accurately

To record payroll accruals accurately, it's essential to understand the accrual basis of accounting. This method recognizes expenses and revenues when they are incurred, regardless of when cash transactions occur. In the context of payroll, this means recording the expense of employee wages and benefits as they are earned, not when they are paid. For example, if an employee works in December but is paid in January, the payroll expense should be recorded in December.

The first step in recording payroll accruals is to determine the amount of wages and benefits earned by employees during the accounting period. This involves calculating the number of hours worked, the hourly rate, and any additional benefits such as overtime, vacation pay, or sick leave. Once these amounts are calculated, they should be recorded in the appropriate accounts. Typically, this would involve debiting a payroll expense account and crediting a payroll liability account.

It's also important to consider the timing of payroll accruals. If an employee is paid bi-weekly, for instance, you may need to record accruals more frequently than if they are paid monthly. This ensures that the financial statements reflect the true financial position of the company at any given time.

Another key aspect of recording payroll accruals is ensuring that the amounts are accurate. This involves double-checking calculations, verifying employee hours, and reconciling any discrepancies. It's also a good practice to review payroll accruals regularly to ensure that they are in line with the company's financial policies and procedures.

Finally, it's important to note that recording payroll accruals can have a significant impact on a company's financial statements. Accrued payroll expenses can affect the income statement, balance sheet, and cash flow statement. Therefore, it's crucial to record these accruals accurately and in a timely manner to ensure that the financial statements are reliable and useful for decision-making.

Mastering Hourly Payroll Calculations: A Step-by-Step Guide for Employers

You may want to see also

Frequently asked questions

Payroll accrual refers to the process of accumulating and recording wages, salaries, and other compensation that employees have earned but have not yet been paid. It is important because it ensures that employees are compensated for their work in a timely and accurate manner, and it also helps businesses to manage their cash flow and financial obligations.

To calculate payroll accrual days, you need to determine the number of days in the pay period that the employee has worked. This can be done by counting the number of days the employee has clocked in or by using a time tracking system. Once you have the number of days worked, you can multiply it by the employee's daily rate of pay to calculate the total amount of wages accrued.

Some common mistakes to avoid when calculating payroll accrual days include forgetting to account for holidays, sick days, or other time off, using an incorrect daily rate of pay, and not properly tracking the number of days worked. It is important to double-check your calculations and ensure that all information is accurate to avoid any discrepancies or errors in employee compensation.