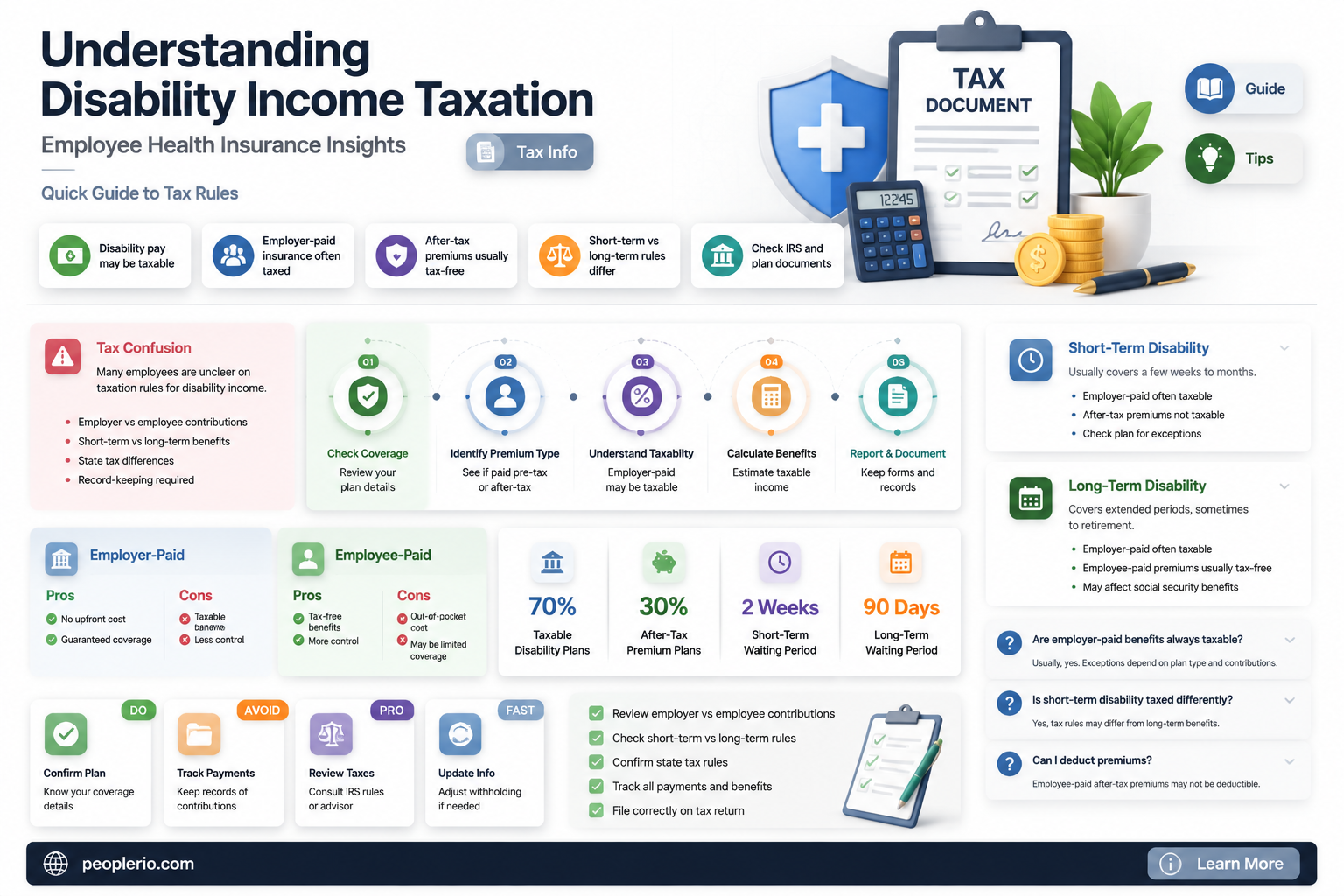

Disability income received through health insurance plans can have significant tax implications for employees. Generally, if the premiums for the disability insurance are paid by the employer, the benefits received by the employee are considered taxable income. This is because the premiums are typically tax-deductible for the employer, and as a result, the benefits are taxed as ordinary income to the employee when received. However, if the employee pays the premiums themselves, the benefits may be tax-free. It's important for employees to understand these tax implications to properly plan for their financial situation in the event of a disability. Consulting with a tax professional or financial advisor can help clarify these complexities and ensure compliance with tax laws.

| Characteristics | Values |

|---|---|

| Taxation Status | Generally taxable |

| Tax Code Section | Section 105(c) of the Internal Revenue Code |

| Employee Contribution | Contributions are made on a pre-tax basis |

| Employer Contribution | Contributions are generally tax-deductible to the employer |

| Benefit Payout | Benefits received are taxable as ordinary income |

| Exceptions | Certain exceptions apply, such as for permanent disability |

| Reporting Requirements | Reported on Form W-2, Box 1 |

| State Tax Implications | May vary by state; some states have additional taxes or exemptions |

| Impact on Other Benefits | May affect eligibility for other government benefits |

| Planning Considerations | Employees should consider tax implications when electing disability coverage |

| Compliance | Employers must comply with federal and state tax laws |

| Documentation | Proper documentation is required to substantiate disability status |

| Appeals Process | Employees can appeal tax determinations if they believe an error has occurred |

| Changes in Tax Law | Tax laws are subject to change, impacting the taxability of disability income |

| Consultation | Employees should consult with a tax professional for personalized advice |

Explore related products

$14.99

What You'll Learn

- General Taxability: Disability income is generally taxable to the employee as it's considered compensation

- Exceptions: Certain conditions or policies might exempt disability income from taxation

- Tax Code: Specific sections of the tax code address the taxation of disability income

- Reporting Requirements: Employers must report disability income on tax forms like W-2

- State Variations: State tax laws may differ from federal laws regarding disability income taxation

![]()

General Taxability: Disability income is generally taxable to the employee as it's considered compensation

Disability income, as a form of compensation, is generally subject to taxation. This principle stems from the fact that disability benefits are considered a replacement for regular wages or salary, which are taxable. Therefore, when an employee receives disability income, it is treated similarly to their regular earnings for tax purposes.

The taxation of disability income can vary based on the source of the benefits. If the disability income is provided through an employer-sponsored plan, it is typically taxable to the employee. This is because the employer is responsible for withholding taxes from the employee's wages, and disability benefits are considered part of those wages. However, if the disability income comes from a private insurance policy that the employee has purchased individually, it may not be taxable, as the premiums for such policies are usually paid with after-tax dollars.

It is important to note that there are some exceptions and nuances to the general rule of disability income taxability. For instance, if the disability benefits are received as a result of a work-related injury or illness, they may be exempt from taxation under certain circumstances. Additionally, the tax treatment of disability income can differ depending on whether the benefits are short-term or long-term, and whether they are paid in a lump sum or as periodic payments.

Employees who receive disability income should consult with a tax professional to understand their specific tax obligations. It is crucial to report all taxable disability income on their tax return to avoid potential penalties and interest. Furthermore, understanding the tax implications of disability benefits can help employees make informed decisions about their financial planning and budgeting during periods of disability.

In summary, while disability income is generally taxable as compensation, the specific tax treatment can depend on various factors, including the source of the benefits, the reason for the disability, and the duration and form of the payments. Employees should seek professional tax advice to ensure compliance with tax laws and to optimize their financial situation while receiving disability benefits.

Understanding the Tax Implications of Employee Health Insurance Reimbursements

You may want to see also

Explore related products

![]()

Exceptions: Certain conditions or policies might exempt disability income from taxation

Under certain circumstances, disability income received through health insurance may be exempt from taxation. One such exception is if the disability income is considered a return of premiums. This occurs when an individual has paid premiums for a disability insurance policy and later receives benefits; in this case, the benefits are generally not taxable as they are seen as a return of the individual's own money.

Another exception is if the disability income is received as a result of an injury or sickness that occurred while the individual was working. In this scenario, the benefits may be exempt from taxation if they are paid by the employer or the employer's insurance carrier, as they are considered a form of workers' compensation.

Additionally, disability income may be exempt from taxation if it is received under a government-sponsored program, such as Social Security Disability Insurance (SSDI) or Supplemental Security Income (SSI). These programs have specific eligibility requirements and are designed to provide financial assistance to individuals who are unable to work due to a disability.

It is important to note that the taxability of disability income can vary depending on the specific circumstances and the jurisdiction in which the individual resides. In some cases, disability income may be partially taxable, while in others it may be fully exempt. It is recommended that individuals consult with a tax professional to determine the taxability of their disability income.

Tax Implications of Health Insurance for Contract Employees Explained

You may want to see also

Explore related products

![]()

Tax Code: Specific sections of the tax code address the taxation of disability income

The tax code contains specific sections that address the taxation of disability income, which is an important consideration for employees receiving such benefits. Section 105 of the Internal Revenue Code, for example, provides tax-free treatment for disability income received under certain conditions. To qualify, the disability income must be received under a plan that is sponsored by the employer and must be used to replace wages lost due to the employee's inability to work. Additionally, the employee must be considered disabled under the terms of the plan, and the disability must be expected to last for at least one year or result in death.

Another relevant section of the tax code is Section 72, which deals with the taxation of distributions from retirement plans, including disability benefits. Under this section, disability benefits received before the employee reaches age 59½ may be subject to a 10% early withdrawal penalty, unless the employee is considered disabled under the terms of the plan. To avoid this penalty, the employee must provide proof of disability to the plan administrator.

It is also important to note that the tax treatment of disability income may vary depending on the type of plan under which it is received. For example, disability income received under a self-insured plan may be taxable to the employee, while disability income received under an insured plan may be tax-free. Additionally, the tax treatment of disability income may be affected by other factors, such as the employee's age, the length of time they have been receiving benefits, and the amount of benefits they are receiving.

In conclusion, the tax code contains specific sections that address the taxation of disability income, and it is important for employees receiving such benefits to understand these provisions in order to minimize their tax liability. By consulting with a tax professional and carefully reviewing the terms of their disability plan, employees can ensure that they are taking advantage of all available tax benefits and avoiding potential penalties.

Exploring Haven Health: Insider Perspectives on Employee Satisfaction

You may want to see also

Explore related products

![]()

Reporting Requirements: Employers must report disability income on tax forms like W-2

Employers have a critical responsibility when it comes to reporting disability income on tax forms. Specifically, they must accurately report such income on forms like the W-2, which is a requirement mandated by the Internal Revenue Service (IRS). This process is integral to ensuring that both the employer and the employee are in compliance with tax laws and regulations.

The W-2 form is a standard tax document that employers must provide to their employees at the end of each year. It details the employee's earnings, tax withholdings, and other relevant information. When disability income is involved, it's essential that this amount is correctly reported on the W-2 to avoid any discrepancies or potential tax liabilities.

One important aspect to note is that disability income reported on the W-2 is generally considered taxable to the employee. This means that the employee will need to report this income on their individual tax return and pay any applicable taxes. However, there are certain circumstances where disability income may be tax-free, such as if it's paid under a government program or if the employee has a specific type of disability insurance policy.

To ensure accurate reporting, employers should carefully review the IRS guidelines and consult with a tax professional if necessary. They should also maintain detailed records of all disability income payments made to employees, including the amounts paid and the dates of payment. This documentation will be crucial in the event of an audit or if there are any questions about the accuracy of the reported information.

In summary, employers play a vital role in reporting disability income on tax forms like the W-2. By understanding their responsibilities and following the appropriate guidelines, they can help ensure that both they and their employees remain in compliance with tax laws and avoid potential penalties or liabilities.

Understanding W-2 Reporting Requirements for Employee Health Insurance

You may want to see also

Explore related products

$49.17 $233.95

![]()

State Variations: State tax laws may differ from federal laws regarding disability income taxation

State tax laws can significantly vary when it comes to the taxation of disability income, creating a complex landscape for employees and employers alike. While federal laws provide a baseline for how disability income is taxed, individual states have the authority to enact their own tax laws, which can differ substantially from federal guidelines. This means that employees receiving disability income may face different tax implications depending on the state in which they reside.

For instance, some states may exempt disability income from state taxes, while others may tax it at a different rate than regular income. Additionally, the definitions of what constitutes disability income can vary from state to state, potentially affecting how much income is subject to taxation. These variations can have a significant impact on the financial planning and tax preparation of individuals receiving disability benefits.

To navigate these complexities, employees should consult with a tax professional who is knowledgeable about both federal and state tax laws. This can help ensure that they are in compliance with all applicable tax regulations and can take advantage of any available tax benefits or exemptions. Employers should also be aware of these state variations, as they may need to adjust their payroll and tax withholding processes accordingly.

In conclusion, understanding the state-specific nuances of disability income taxation is crucial for both employees and employers. By staying informed about these variations and seeking professional guidance when needed, individuals can better manage their tax obligations and financial planning related to disability income.

Navigating Your Employee Health Policy Agreement: A Step-by-Step Guide

You may want to see also

Frequently asked questions

Generally, disability income received through health insurance is not taxable to the employee if the premiums were paid with after-tax dollars. This is because the employee has already paid taxes on the money used to purchase the insurance.

If the employer pays for the disability insurance premiums, the disability income may be taxable to the employee. This is considered a fringe benefit, and the value of the benefit is included in the employee's gross income.

Yes, there are exceptions. For example, if the disability income is received under a governmental disability program, such as Social Security Disability Insurance (SSDI), it is generally not taxable. Additionally, if the employee is permanently and totally disabled, certain types of disability income may be tax-free.