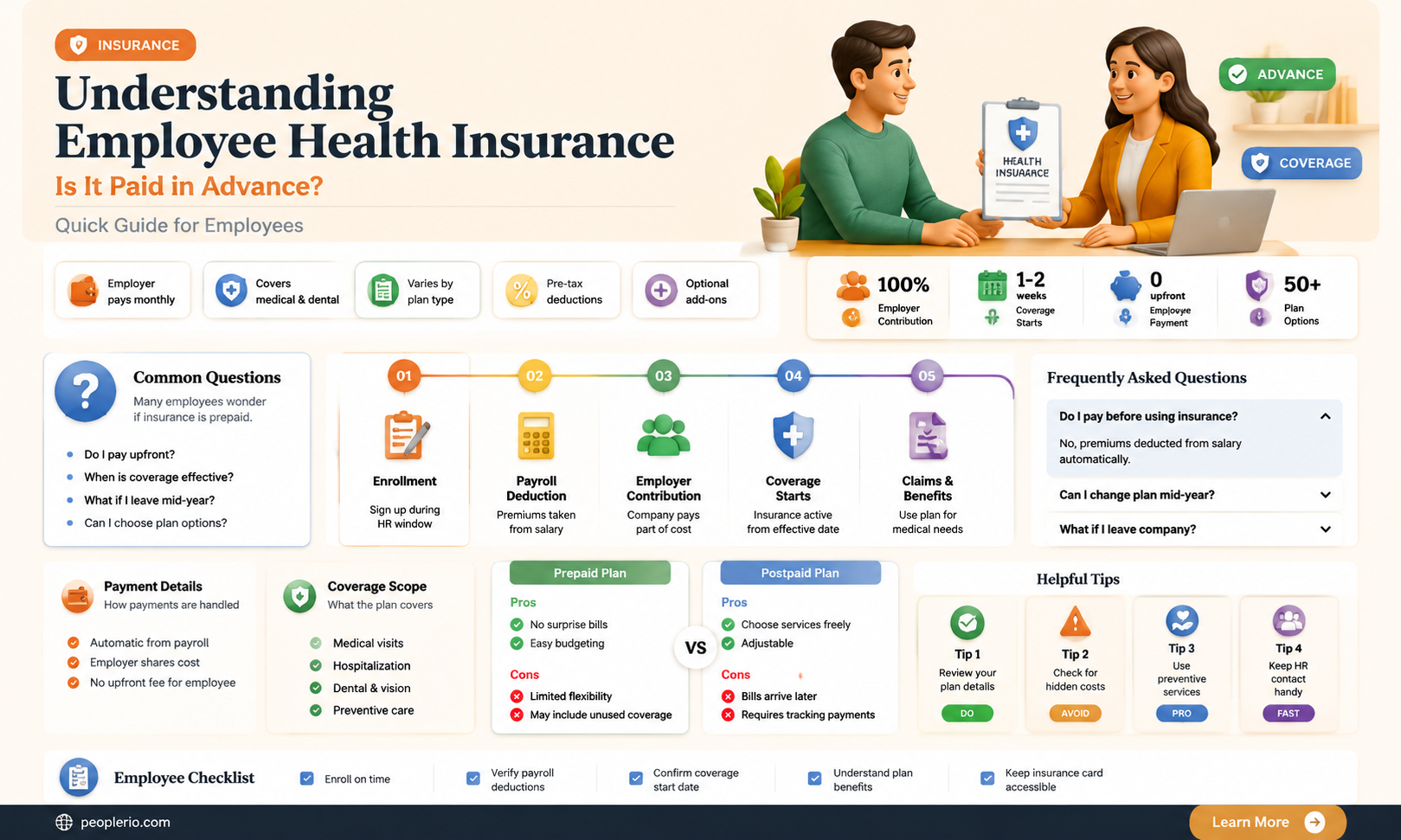

Employee health insurance is a critical component of compensation packages offered by many employers. One common question that arises is whether employee health insurance is paid in advance. Typically, health insurance premiums are paid on a monthly basis, with the employer often contributing a significant portion of the cost. However, the specifics can vary widely depending on the employer's policies, the type of insurance plan, and the regulations in the relevant jurisdiction. Some employers may choose to pay premiums annually or quarterly, while others might offer more flexible payment options. Understanding the payment structure for health insurance is essential for both employers and employees to ensure proper budgeting and financial planning.

Explore related products

$13.11 $19.95

What You'll Learn

- Premium Payment Timing: When are employee health insurance premiums paid Monthly, quarterly, or annually

- Employer vs. Employee Contributions: What portions of the health insurance costs do employers and employees cover respectively

- Types of Health Insurance Plans: Which plans require advance payment HMO, PPO, HSA, or FSA

- Grace Periods and Late Payments: Are there any grace periods for late payments What are the consequences of missing a payment deadline

- Tax Implications: How do advance payments for employee health insurance affect tax deductions and credits for both employers and employees

![]()

Premium Payment Timing: When are employee health insurance premiums paid? Monthly, quarterly, or annually?

Employee health insurance premiums are typically paid in advance, but the specific timing can vary depending on the employer's plan and the insurance provider's requirements. In most cases, premiums are paid on a monthly basis, with the payment due before the start of the new month. This ensures that employees have continuous coverage without any lapses.

Some employers may choose to pay premiums quarterly or annually, which can help reduce administrative costs and streamline the payment process. However, this may also require employees to pay a larger lump sum upfront, which could be a financial burden for some.

It's important for employees to understand their employer's premium payment schedule and to make sure they have the necessary funds available to cover their share of the premiums. Failure to pay premiums on time can result in a loss of coverage, which can have serious consequences in the event of an unexpected illness or injury.

Employers should also be aware of the potential impact of premium payment timing on their employees' financial well-being. Offering flexible payment options or providing advance notice of any changes to the payment schedule can help employees better manage their finances and avoid any disruptions to their coverage.

In conclusion, while employee health insurance premiums are generally paid in advance, the specific timing and frequency of payments can vary depending on the employer's plan and the insurance provider's requirements. It's essential for both employers and employees to understand the payment schedule and to communicate openly about any changes or concerns to ensure continuous coverage and financial stability.

Nurturing Workforce Wellness: Strategies for Optimal Employee Health

You may want to see also

Explore related products

![]()

Employer vs. Employee Contributions: What portions of the health insurance costs do employers and employees cover respectively?

Employers typically cover a significant portion of health insurance costs for their employees. On average, employers pay around 70-80% of the premium for individual coverage and 50-60% for family coverage. This means that employees are responsible for the remaining 20-30% of the premium for individual coverage and 40-50% for family coverage. However, the exact split can vary depending on the employer's policy and the type of plan chosen.

In addition to the premium, employees may also be responsible for other out-of-pocket costs, such as deductibles, copays, and coinsurance. These costs can add up quickly, so it's important for employees to understand their plan's coverage and limitations. Employers may also offer additional benefits, such as dental and vision coverage, which may be paid for entirely by the employee.

One unique aspect of employer-sponsored health insurance is that the employer's contribution is often tax-deductible as a business expense. This can provide a significant benefit to the employer, as it reduces their taxable income. However, employees should be aware that their portion of the premium may be taxed as income.

Another important consideration is that employer-sponsored health insurance is not always guaranteed. Employers may choose to terminate their health insurance plans at any time, which can leave employees scrambling to find new coverage. Additionally, if an employee loses their job, they may lose their health insurance coverage as well.

Overall, while employer-sponsored health insurance can provide valuable coverage, it's important for employees to understand their plan's details and limitations. By doing so, they can make informed decisions about their healthcare and financial well-being.

Understanding 1099 Forms: Do They Cover Employee Health Care Expenses?

You may want to see also

Explore related products

![]()

Types of Health Insurance Plans: Which plans require advance payment? HMO, PPO, HSA, or FSA?

Health Maintenance Organizations (HMOs) typically require advance payment in the form of premiums. These premiums are often paid monthly or annually, depending on the plan and the employer's arrangement. HMOs are known for their managed care approach, where they coordinate healthcare services and often require referrals from a primary care physician to see specialists. The advance payment helps cover the costs of these coordinated services and ensures that members have access to a network of healthcare providers.

Preferred Provider Organizations (PPOs) also usually involve advance payment of premiums. However, PPOs offer more flexibility than HMOs, allowing members to see both in-network and out-of-network providers without the need for referrals. The advance payment for PPOs helps to subsidize the costs of healthcare services, but members may still be responsible for a portion of the expenses, such as deductibles and copays, at the time of service.

Health Savings Accounts (HSAs) are a type of health insurance plan that combines a high-deductible health plan (HDHP) with a tax-advantaged savings account. HSAs do not require advance payment in the traditional sense, as members are responsible for paying their healthcare expenses out-of-pocket until they meet their deductible. However, they can use funds from their HSA to cover these costs, and the account can be funded through payroll deductions or personal contributions.

Flexible Spending Accounts (FSAs) are another type of health insurance plan that allows members to set aside pre-tax dollars to pay for qualified healthcare expenses. FSAs do require advance payment, as members must elect to have a certain amount deducted from their paycheck each year to fund the account. These funds can then be used to cover a variety of healthcare costs, such as deductibles, copays, and prescription medications.

In summary, HMOs and PPOs typically require advance payment in the form of premiums, while HSAs and FSAs involve different payment structures. HSAs do not require traditional advance payment but involve out-of-pocket expenses until the deductible is met, while FSAs require members to set aside funds in advance through payroll deductions. Understanding these differences can help employees make informed decisions about their health insurance options and how they prefer to pay for their healthcare expenses.

Navigating Employee Health Insurance Stipends: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Grace Periods and Late Payments: Are there any grace periods for late payments? What are the consequences of missing a payment deadline?

In the realm of employee health insurance, understanding grace periods and the repercussions of late payments is crucial for maintaining continuous coverage. A grace period is a specified timeframe during which an employee can make a payment without incurring penalties or losing coverage. This period typically follows the due date for premiums and varies depending on the insurance provider and the terms of the policy.

The consequences of missing a payment deadline can be severe. If an employee fails to make a payment within the grace period, they may face penalties such as late fees or interest charges. More significantly, there is a risk of losing health insurance coverage, which can leave the employee vulnerable to high medical costs. In some cases, the employee may be required to undergo a medical underwriting process to reinstate coverage, which could result in higher premiums or even denial of coverage if they have pre-existing conditions.

To avoid these negative outcomes, employees should be aware of their payment due dates and the length of any grace periods. They should also understand the specific consequences outlined in their policy for late payments. Setting up automatic payments or reminders can be helpful strategies to ensure timely payments and maintain uninterrupted health insurance coverage.

In summary, grace periods and late payments are critical aspects of employee health insurance that require careful attention. By understanding the terms and potential consequences, employees can take proactive steps to manage their payments effectively and safeguard their health coverage.

Strategic Steps to Crafting a Comprehensive Employee Health Plan

You may want to see also

Explore related products

![]()

Tax Implications: How do advance payments for employee health insurance affect tax deductions and credits for both employers and employees?

Advance payments for employee health insurance can have significant tax implications for both employers and employees. From an employer's perspective, making advance payments may affect the timing of tax deductions. Generally, employers can deduct the cost of health insurance premiums paid for employees in the year the payments are made. However, if advance payments are made for future years, the deductions may need to be deferred until the corresponding years when the insurance coverage is actually provided.

For employees, advance payments for health insurance may impact their tax credits. The Affordable Care Act (ACA) provides premium tax credits to eligible individuals who purchase health insurance through a health insurance exchange. If an employer makes advance payments for an employee's health insurance, it may reduce the employee's eligibility for these tax credits. This is because the advance payments are considered when calculating the employee's modified adjusted gross income (MAGI), which is used to determine eligibility for the premium tax credits.

Furthermore, advance payments may also affect the taxability of benefits received by employees. If an employer pays for health insurance coverage that extends beyond the current year, the value of the coverage provided in future years may be considered taxable income to the employee when received. This is because the employee is receiving a benefit that has a monetary value, which is generally subject to taxation.

To mitigate these tax implications, employers and employees should carefully consider the timing and structure of advance payments for health insurance. Employers may want to consult with tax professionals to ensure that their advance payment strategies align with current tax laws and regulations. Employees should also be aware of how advance payments may impact their tax credits and taxable income, and plan accordingly.

In conclusion, advance payments for employee health insurance can have complex tax implications that require careful consideration. By understanding these implications, employers and employees can make informed decisions about their health insurance arrangements and minimize potential tax liabilities.

Understanding Pretax Employee Health Insurance Contributions

You may want to see also

Frequently asked questions

No, employee health insurance is not always paid in advance. The payment structure can vary depending on the employer's policy and the insurance provider's requirements. Some employers may pay the premiums monthly, quarterly, or annually, while others might deduct the cost from employees' paychecks.

Paying employee health insurance in advance can offer several benefits. It can help employers manage their cash flow more effectively by spreading out the cost of premiums over time. Additionally, it may simplify the administration process and reduce the risk of missed payments. For employees, advance payment can provide a sense of security, knowing that their health coverage is taken care of.

Paying employee health insurance in advance can have tax implications for both employers and employees. Employers may be able to deduct the cost of premiums as a business expense, potentially reducing their taxable income. For employees, the advance payment of health insurance premiums may be considered a form of imputed income, which could affect their tax liability. It's essential to consult with a tax professional to understand the specific tax implications in your situation.

![NatureWise Curcumin Turmeric 2250mg - 95% Curcuminoids & BioPerine Black Pepper Extract for Advanced Absorption - Daily Joint and Immune Health Support - Vegan, Non-GMO, 180 Count[60-Day Supply]](https://m.media-amazon.com/images/I/714UFxWRUFL._AC_UL320_.jpg)