Employee benefits are a crucial aspect of compensation packages offered by employers. These benefits can include health insurance, retirement plans, and other perks designed to attract and retain talent. A common question among employees is whether these benefits are deducted before tax, which can significantly impact their take-home pay and overall financial planning. Understanding the tax implications of employee benefits is essential for both employees and employers to ensure compliance with tax laws and to make informed decisions about compensation structures.

| Characteristics | Values |

|---|---|

| Deduction Type | Pre-tax |

| Impact on Taxable Income | Reduces taxable income |

| Examples | Health insurance premiums, retirement plan contributions |

| Effect on Take-Home Pay | Lower take-home pay due to reduced taxable income |

| Employer's Role | Employer may contribute or deduct benefits |

| Employee's Role | Employee may contribute or have benefits deducted |

| Tax Advantage | Contributions are tax-deductible |

| Common Benefits Included | Health, dental, vision, retirement plans |

| Less Common Benefits | Life insurance, disability insurance, commuter benefits |

| Legal Requirements | Governed by tax laws and regulations |

Explore related products

What You'll Learn

- Taxable Benefits: Understand which benefits are taxable and how they impact an employee's gross income

- Pre-Tax Deductions: Explore common pre-tax deductions like 401(k) contributions and health insurance premiums

- After-Tax Deductions: Learn about deductions taken after taxes, such as Roth IRA contributions and certain insurance premiums

- Benefits and Income Tax: Discover how different benefits affect taxable income and overall tax liability

- Employer Contributions: Find out how employer contributions to benefits like retirement plans and health insurance are treated for tax purposes

![]()

Taxable Benefits: Understand which benefits are taxable and how they impact an employee's gross income

Understanding taxable benefits is crucial for both employers and employees. Taxable benefits are those that the Internal Revenue Service (IRS) considers part of an employee's gross income, and therefore, subject to federal income tax. These benefits can include health insurance premiums, life insurance, disability insurance, and other perks provided by the employer. It's important to note that not all benefits are taxable; for instance, certain types of employee benefits, such as qualified retirement plan contributions or dependent care assistance, may be excluded from gross income.

The impact of taxable benefits on an employee's gross income can be significant. When an employer provides taxable benefits, it increases the employee's gross income, which in turn can affect their tax liability. This means that employees need to be aware of the tax implications of the benefits they receive and plan accordingly. Employers also have a responsibility to report the value of taxable benefits on the employee's Form W-2, which is used to calculate tax liability.

One common misconception is that all employee benefits are deducted before tax. However, this is not always the case. While some benefits, such as 401(k) contributions, are indeed deducted before tax, others, like health insurance premiums, are often paid with after-tax dollars. This distinction is important because it affects the employee's take-home pay and tax liability.

To navigate the complexities of taxable benefits, employees should consult with a tax professional or use tax preparation software that can help them understand the tax implications of their benefits. Employers should also ensure that they are properly reporting taxable benefits to avoid any potential legal or financial issues.

In conclusion, taxable benefits are a critical aspect of employee compensation that can have a significant impact on gross income and tax liability. By understanding which benefits are taxable and how they are reported, employees and employers can make informed decisions and avoid potential pitfalls.

Employee Meals Tax Deduction: What Businesses Need to Know

You may want to see also

Explore related products

![]()

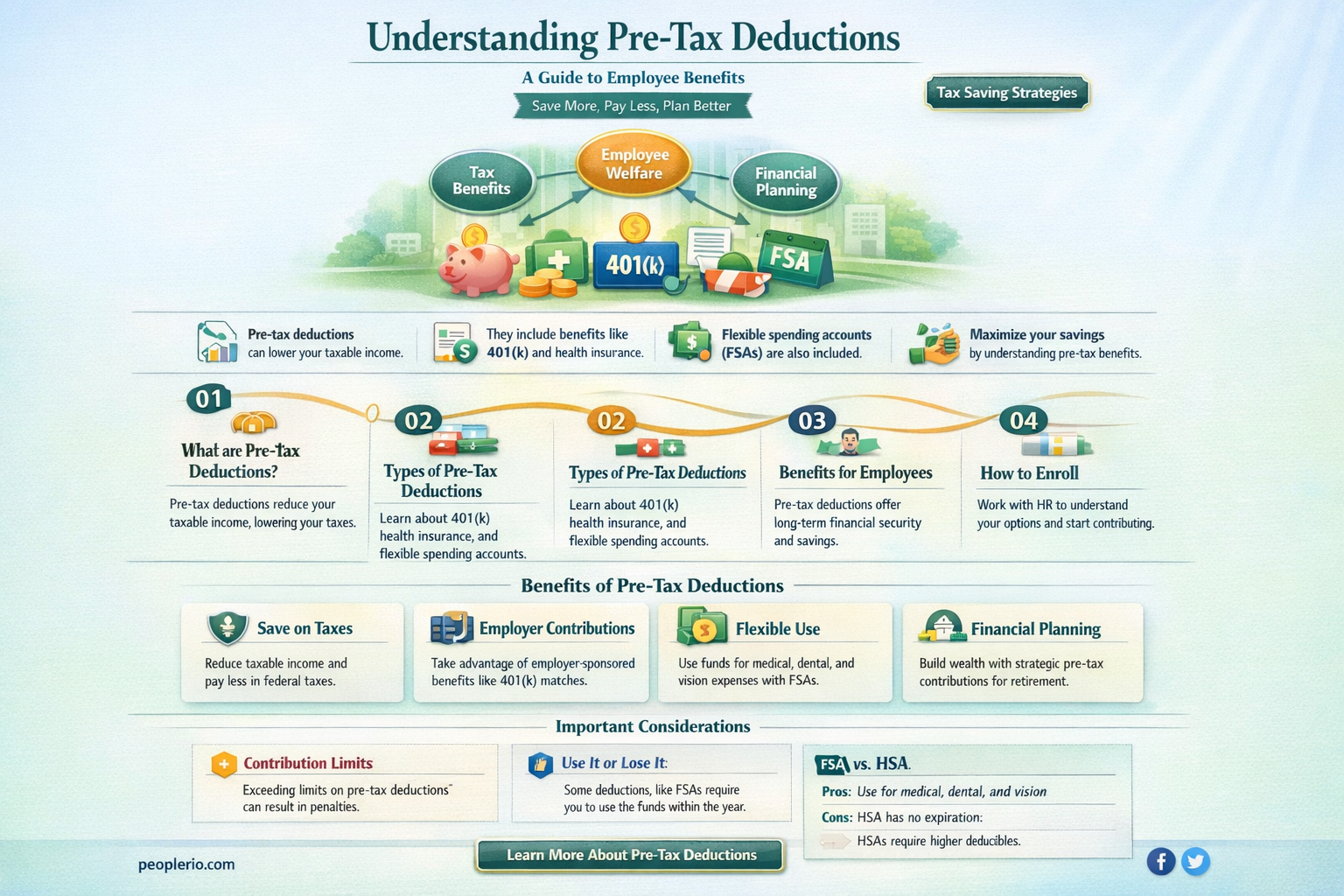

Pre-Tax Deductions: Explore common pre-tax deductions like 401(k) contributions and health insurance premiums

Understanding pre-tax deductions is crucial for employees to optimize their financial planning. Pre-tax deductions, such as contributions to a 401(k) plan or health insurance premiums, are subtracted from an employee's gross income before taxes are calculated. This reduces the taxable income, leading to a lower tax liability. For instance, if an employee contributes $5,000 to their 401(k) plan annually, this amount is deducted from their gross income, saving them from paying taxes on that $5,000.

One of the most common pre-tax deductions is the 401(k) contribution. This retirement savings plan allows employees to set aside a portion of their income for retirement, with the added benefit of reducing their taxable income. The IRS sets annual contribution limits, and employees can choose to contribute a fixed amount or a percentage of their income. For example, an employee earning $50,000 who contributes 10% of their income to a 401(k) plan would save $5,000 in taxes annually, assuming a 20% tax rate.

Health insurance premiums are another significant pre-tax deduction. Many employers offer health insurance plans where the premiums are deducted from employees' paychecks before taxes. This not only helps employees save on taxes but also makes health insurance more affordable. For example, if an employee's health insurance premium is $200 per month, they would save approximately $480 in taxes annually, assuming a 24% tax rate.

Flexible Spending Accounts (FSAs) and Health Savings Accounts (HSAs) are additional pre-tax deductions that can benefit employees. FSAs allow employees to set aside money for qualified medical expenses, while HSAs are available to those with high-deductible health plans and can be used for both medical expenses and retirement savings. Both options reduce taxable income and can lead to significant tax savings.

In conclusion, pre-tax deductions like 401(k) contributions and health insurance premiums offer employees a way to reduce their tax liability while also saving for important expenses like retirement and healthcare. By understanding and maximizing these deductions, employees can take control of their financial future and make the most of their hard-earned money.

Understanding Employee Tax: A Comprehensive Guide for 2023

You may want to see also

Explore related products

![]()

After-Tax Deductions: Learn about deductions taken after taxes, such as Roth IRA contributions and certain insurance premiums

Roth IRA contributions are a prime example of after-tax deductions that offer significant benefits for retirement savings. Unlike traditional IRAs or 401(k) plans, Roth IRAs are funded with after-tax dollars, which means you've already paid income tax on the money you contribute. The advantage lies in the tax-free growth and withdrawals in retirement, provided certain conditions are met. This makes Roth IRAs an attractive option for those who expect to be in a higher tax bracket during retirement or want to diversify their retirement income sources.

Certain insurance premiums, such as those for long-term care insurance or supplemental health insurance, may also qualify as after-tax deductions. These deductions can help reduce your taxable income, potentially lowering your overall tax liability. However, it's crucial to understand the specific rules and limitations associated with these deductions, as they can vary based on factors like your income level, the type of insurance, and whether the premiums are paid through payroll deductions or directly by you.

Another aspect of after-tax deductions to consider is the impact on your take-home pay. While these deductions can provide long-term benefits, they may also reduce the amount of money you receive in each paycheck. It's essential to balance the potential long-term advantages with your current financial needs and budget constraints.

To maximize the benefits of after-tax deductions, it's important to plan strategically. This may involve consulting with a financial advisor or tax professional to determine the optimal contribution amounts and to ensure you're taking advantage of all available deductions. Additionally, staying informed about changes in tax laws and regulations can help you adapt your strategy as needed to maintain the most favorable tax position.

In summary, after-tax deductions like Roth IRA contributions and certain insurance premiums can be valuable tools for managing your taxes and saving for the future. By understanding the rules and limitations associated with these deductions and planning accordingly, you can make the most of these opportunities to enhance your financial well-being.

Understanding AFLC Payments: Pre-Tax or Post-Tax?

You may want to see also

Explore related products

![]()

Benefits and Income Tax: Discover how different benefits affect taxable income and overall tax liability

Understanding the interplay between benefits and income tax is crucial for both employees and employers. Benefits can significantly impact an individual's taxable income and, consequently, their overall tax liability. This section delves into the specifics of how different types of benefits are treated for tax purposes, providing insights that can help optimize tax planning and compliance.

Taxable Benefits:

Certain benefits provided by employers are considered taxable and must be included in an employee's gross income. These include, but are not limited to, bonuses, commissions, and certain types of fringe benefits such as company cars, housing allowances, and meals. The fair market value of these benefits is added to the employee's taxable income, increasing the amount subject to income tax.

Non-Taxable Benefits:

On the other hand, some benefits are not taxable and do not need to be included in gross income. Examples of non-taxable benefits include health insurance premiums paid by the employer, certain retirement plan contributions, and educational assistance programs. These benefits can provide significant value to employees without increasing their tax burden.

Impact on Tax Liability:

The distinction between taxable and non-taxable benefits has a direct impact on an individual's tax liability. Taxable benefits increase the amount of income subject to tax, potentially pushing an individual into a higher tax bracket. Conversely, non-taxable benefits can help reduce taxable income, leading to a lower tax liability. Understanding this distinction is essential for effective tax planning.

Strategies for Optimization:

Employees and employers can employ various strategies to optimize the tax treatment of benefits. For example, employers may choose to provide more non-taxable benefits or structure taxable benefits in a way that minimizes their impact on taxable income. Employees can also take advantage of tax-saving opportunities, such as contributing to tax-deferred retirement plans or using flexible spending accounts for eligible expenses.

In conclusion, the relationship between benefits and income tax is complex and multifaceted. By understanding how different types of benefits are treated for tax purposes, individuals can make informed decisions that can help minimize their tax liability and maximize their overall financial well-being. This knowledge is particularly valuable during tax season, when careful planning can lead to significant savings.

Railroad Employee Tax Filing Guide: Simplify Your Tax Process

You may want to see also

Explore related products

![]()

Employer Contributions: Find out how employer contributions to benefits like retirement plans and health insurance are treated for tax purposes

Employer contributions to employee benefits, such as retirement plans and health insurance, are generally not deductible by the employee for tax purposes. This is because these contributions are typically made with pre-tax dollars, reducing the employee's taxable income. For example, if an employer contributes $5,000 to an employee's 401(k) plan, that amount is not included in the employee's gross income, thus lowering their tax liability.

However, there are some exceptions and nuances to this rule. For instance, employer contributions to health savings accounts (HSAs) are deductible by the employee, even if they are made with pre-tax dollars. This is because HSA contributions are considered tax-deductible contributions, similar to those made to a traditional IRA. Additionally, employer contributions to certain types of retirement plans, such as a SEP IRA or a SIMPLE IRA, may be deductible by the employee, depending on the specific circumstances.

It's also important to note that employer contributions to employee benefits can have a significant impact on the employee's overall compensation package. While these contributions may not be directly deductible for tax purposes, they can still provide substantial financial benefits to the employee. For example, an employer's contribution to a retirement plan can help the employee save for the future, while contributions to health insurance can help reduce the employee's out-of-pocket healthcare costs.

In conclusion, while employer contributions to employee benefits are generally not deductible by the employee for tax purposes, there are some exceptions and nuances to this rule. Employees should consult with a tax professional to fully understand the tax implications of their employer's contributions to their benefits package.

Mastering Payroll: A Step-by-Step Guide to Calculating Employee Taxes

You may want to see also

Frequently asked questions

Yes, certain employee benefits are deducted before tax, which can lower your taxable income and potentially reduce your tax liability.

Common pretax deductions include contributions to retirement plans like 401(k)s, health insurance premiums, and flexible spending accounts (FSAs) for health care and dependent care expenses.

Pretax deductions reduce your taxable income, which can lower your tax withholding and increase your take-home pay. However, it's important to note that these deductions are subject to certain limits and eligibility requirements.