Employee federal taxes are indeed paid post-tax. This means that the taxes are deducted from an employee's gross income, and the remaining amount—the net income or take-home pay—is what the employee receives. The federal taxes withheld include income tax, Social Security tax, and Medicare tax. These taxes are calculated based on the employee's earnings and tax filing status. Employers are responsible for withholding these taxes and submitting them to the federal government on behalf of their employees. Understanding how these taxes are paid and calculated is crucial for both employees and employers to ensure compliance with tax laws and regulations.

| Characteristics | Values |

|---|---|

| Tax Type | Federal |

| Payment Timing | Post-tax |

| Employee Status | Yes |

| Tax Category | Income tax, Social Security tax, Medicare tax |

| Deduction Type | Withheld from employee's paycheck |

| Payment Frequency | Regularly scheduled (e.g., bi-weekly, monthly) |

| Reporting Requirements | Reported on Form W-2 |

Explore related products

What You'll Learn

- Understanding Federal Taxes: Explanation of federal income tax, Social Security, and Medicare taxes

- Tax Withholding: How employers deduct taxes from employees' paychecks before paying them

- Post-Tax Deductions: Instances where taxes might be deducted after an employee receives their paycheck

- Tax Filing Requirements: Employees' obligations to file tax returns and pay any owed taxes

- Tax Credits and Refunds: Overview of tax credits employees might claim and how refunds are processed

![]()

Understanding Federal Taxes: Explanation of federal income tax, Social Security, and Medicare taxes

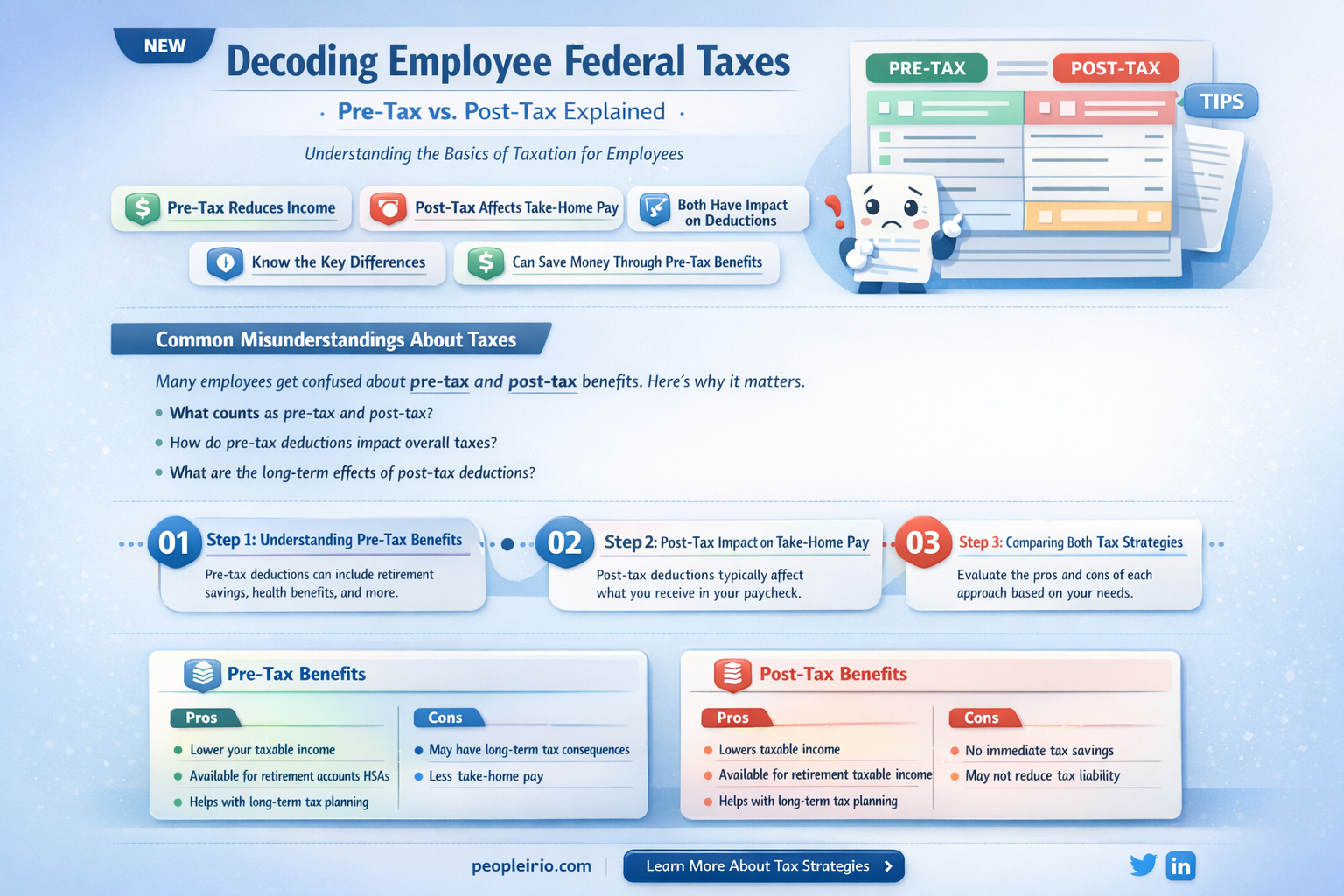

Federal taxes are a critical component of the U.S. tax system, and understanding them is essential for every taxpayer. The three main types of federal taxes that employees typically pay are federal income tax, Social Security tax, and Medicare tax. These taxes are generally withheld from an employee's paycheck before they receive it, which means they are paid pre-tax, not post-tax.

Federal income tax is based on an individual's income and is used to fund various government programs and services. The amount of federal income tax an employee pays depends on their income level and tax filing status. Social Security tax, on the other hand, is used to fund the Social Security program, which provides retirement, disability, and survivor benefits. In 2023, the Social Security tax rate is 6.2% for both employees and employers, and it is applied to the first $147,000 of an employee's earnings.

Medicare tax is used to fund the Medicare program, which provides health insurance for individuals aged 65 and older, as well as certain younger people with disabilities. The Medicare tax rate is 1.45% for both employees and employers, and it is applied to all of an employee's earnings. Additionally, there is an extra 0.9% Medicare tax for employees who earn more than $200,000 per year ($250,000 for married couples filing jointly).

It's important to note that while these taxes are generally paid pre-tax, there are some situations where employees may need to pay federal taxes post-tax. For example, if an employee's employer does not withhold enough federal income tax from their paycheck, they may need to make estimated tax payments throughout the year to avoid owing a large amount of money when they file their tax return. Additionally, if an employee receives a bonus or other supplemental income that is not subject to withholding, they may need to pay federal taxes on that income when they file their tax return.

In conclusion, understanding federal taxes is crucial for every employee, and it's important to know how much is being withheld from your paycheck and whether you may need to make additional tax payments throughout the year. By staying informed about federal tax laws and regulations, employees can avoid unexpected tax bills and ensure they are in compliance with the IRS.

Understanding 401k Deferrals: Are They Subject to Payroll Taxes?

You may want to see also

Explore related products

![]()

Tax Withholding: How employers deduct taxes from employees' paychecks before paying them

Employers are responsible for deducting federal taxes from their employees' paychecks before issuing payment. This process, known as tax withholding, is a critical component of the U.S. tax system. It ensures that employees pay their fair share of federal taxes throughout the year, rather than facing a large tax bill at the end of the year.

The amount of federal tax withheld from an employee's paycheck is determined by several factors, including their gross income, marital status, and the number of allowances they claim on their W-4 form. Employers use the information provided on the W-4 form to calculate the amount of federal tax to withhold from each paycheck.

Federal tax withholding is typically calculated using a percentage-based system. For example, in 2022, the federal tax withholding rate for single individuals with a gross income of $50,000 per year is 12%. This means that $600 would be withheld from their monthly paycheck ($50,000 x 0.12 ÷ 12).

Employers are required to remit the withheld federal taxes to the Internal Revenue Service (IRS) on a regular basis, typically quarterly. They must also provide employees with a Form W-2 at the end of the year, which shows the total amount of federal tax withheld from their paychecks throughout the year.

It's important to note that tax withholding is not a one-size-fits-all process. Employers must take into account various factors, such as state and local tax laws, when calculating the amount of tax to withhold from an employee's paycheck. Additionally, employees may need to adjust their W-4 form if their personal or financial situation changes during the year.

In conclusion, tax withholding is a crucial aspect of the U.S. tax system that ensures employees pay their federal taxes throughout the year. Employers play a vital role in this process by deducting the appropriate amount of tax from their employees' paychecks and remitting it to the IRS.

Maximizing Your 401(k): Understanding Tax Deductibility of Contributions

You may want to see also

Explore related products

![]()

Post-Tax Deductions: Instances where taxes might be deducted after an employee receives their paycheck

In certain circumstances, taxes may be deducted from an employee's paycheck after they have already received it. This is known as post-tax deductions. One common instance of this occurs when an employee has multiple jobs and their combined income exceeds the tax withholding thresholds set by the IRS. In this case, the employee may need to pay additional taxes on their second job's income, which would be deducted post-tax.

Another scenario where post-tax deductions might occur is when an employee receives a bonus or commission that pushes their income into a higher tax bracket. If the employer has already withheld taxes based on the employee's regular salary, the additional income may require further tax deductions. This can also happen if an employee's tax filing status changes during the year, such as getting married or having a child, and they need to adjust their tax withholdings accordingly.

Post-tax deductions can also be made for other reasons, such as repayment of a 401(k) loan or contributions to a flexible spending account (FSA). In these cases, the deductions are typically made on a post-tax basis, as they are considered voluntary contributions or repayments rather than mandatory tax withholdings.

It's important for employees to be aware of these situations and plan accordingly. If they expect to have post-tax deductions, they should set aside the necessary funds to avoid any surprises when their paycheck arrives. Employers should also communicate clearly with their employees about any post-tax deductions that will be made, to ensure transparency and avoid confusion.

In summary, post-tax deductions are instances where taxes or other amounts are deducted from an employee's paycheck after they have already received it. This can occur due to multiple jobs, bonuses, changes in tax filing status, or voluntary contributions or repayments. Employees should be aware of these situations and plan accordingly, while employers should communicate clearly with their employees about any post-tax deductions.

Are Employee Benefits Tax Deductible? A Comprehensive Guide for Employers

You may want to see also

Explore related products

$18.95

![]()

Tax Filing Requirements: Employees' obligations to file tax returns and pay any owed taxes

Employees are generally required to file tax returns annually to report their income and calculate any taxes owed. This obligation applies regardless of whether taxes are withheld from their paychecks. The specific requirements can vary based on factors such as income level, filing status, and whether the employee has multiple jobs or sources of income.

The process of filing taxes involves gathering necessary documents, such as W-2 forms from employers, and using these to complete a tax return form. Employees must report all income, including wages, salaries, tips, and any other compensation received during the year. They must also calculate their tax liability based on the applicable tax rates and deductions.

If an employee owes taxes, they are typically required to pay the amount due by the tax filing deadline, which is usually April 15th in the United States. Failure to pay owed taxes can result in penalties and interest charges. Employees can make payments electronically or by mail, and they may also be able to set up a payment plan if they are unable to pay the full amount at once.

It is important for employees to understand their tax filing obligations and to take steps to ensure they are in compliance with the law. This may involve seeking assistance from a tax professional or using tax preparation software to help with the filing process. By meeting their tax obligations, employees can avoid potential legal and financial consequences.

Understanding Employee Tax Deductions: A Comprehensive Guide for Workers

You may want to see also

Explore related products

$19.99

![]()

Tax Credits and Refunds: Overview of tax credits employees might claim and how refunds are processed

Tax credits are a crucial aspect of the tax system that employees should understand to maximize their financial benefits. These credits can reduce the amount of tax owed, and in some cases, result in a refund. There are various types of tax credits available to employees, including the Earned Income Tax Credit (EITC), Child Tax Credit, and Education Credits. To claim these credits, employees must meet specific eligibility criteria and provide necessary documentation when filing their tax returns.

The process of claiming tax credits and receiving refunds involves several steps. First, employees must accurately calculate their tax liability and determine which credits they are eligible for. This may require consulting tax forms, instructions, or seeking professional advice. Once the credits are claimed on the tax return, the IRS will review the information and process the refund if approved. Refunds can be issued through direct deposit, paper check, or applied to future tax payments.

One common mistake employees make is failing to claim all the credits they are eligible for, resulting in a lower refund or higher tax liability. To avoid this, it's essential to stay informed about available credits and understand the eligibility requirements. Additionally, employees should keep accurate records of their income, expenses, and tax-related documents throughout the year to facilitate the tax filing process and ensure they receive the maximum refund possible.

In recent years, the IRS has implemented various measures to streamline the tax filing process and improve refund processing times. These include the use of electronic filing systems, automated refund processing, and enhanced security measures to prevent fraud. As a result, most refunds are processed within a few weeks of filing, although some cases may require additional review or documentation.

Understanding tax credits and refunds is an essential part of financial planning for employees. By staying informed and taking advantage of available credits, employees can reduce their tax burden and potentially receive a significant refund. This knowledge can also help employees make informed decisions about their finances throughout the year, such as adjusting their withholding or making tax-advantaged investments.

Are Employee Pension Contributions Tax Deductible? A Comprehensive Guide

You may want to see also

Frequently asked questions

"Post-tax" refers to the amount of money that remains after taxes have been deducted. In the context of employee federal taxes, it means the taxes are paid after the employee's gross income has been reduced by the tax amount.

Employee federal taxes are typically paid pre-tax. This means that the tax amount is deducted from the employee's gross income before they receive their paycheck.

Some examples of post-tax deductions include certain types of retirement contributions, such as Roth IRA contributions, and some types of insurance premiums, such as long-term care insurance.

Paying employee federal taxes post-tax would increase an employee's take-home pay because the tax amount would not be deducted from their gross income before they receive their paycheck. However, this could also result in a larger tax bill at the end of the year, depending on the employee's income and tax bracket.