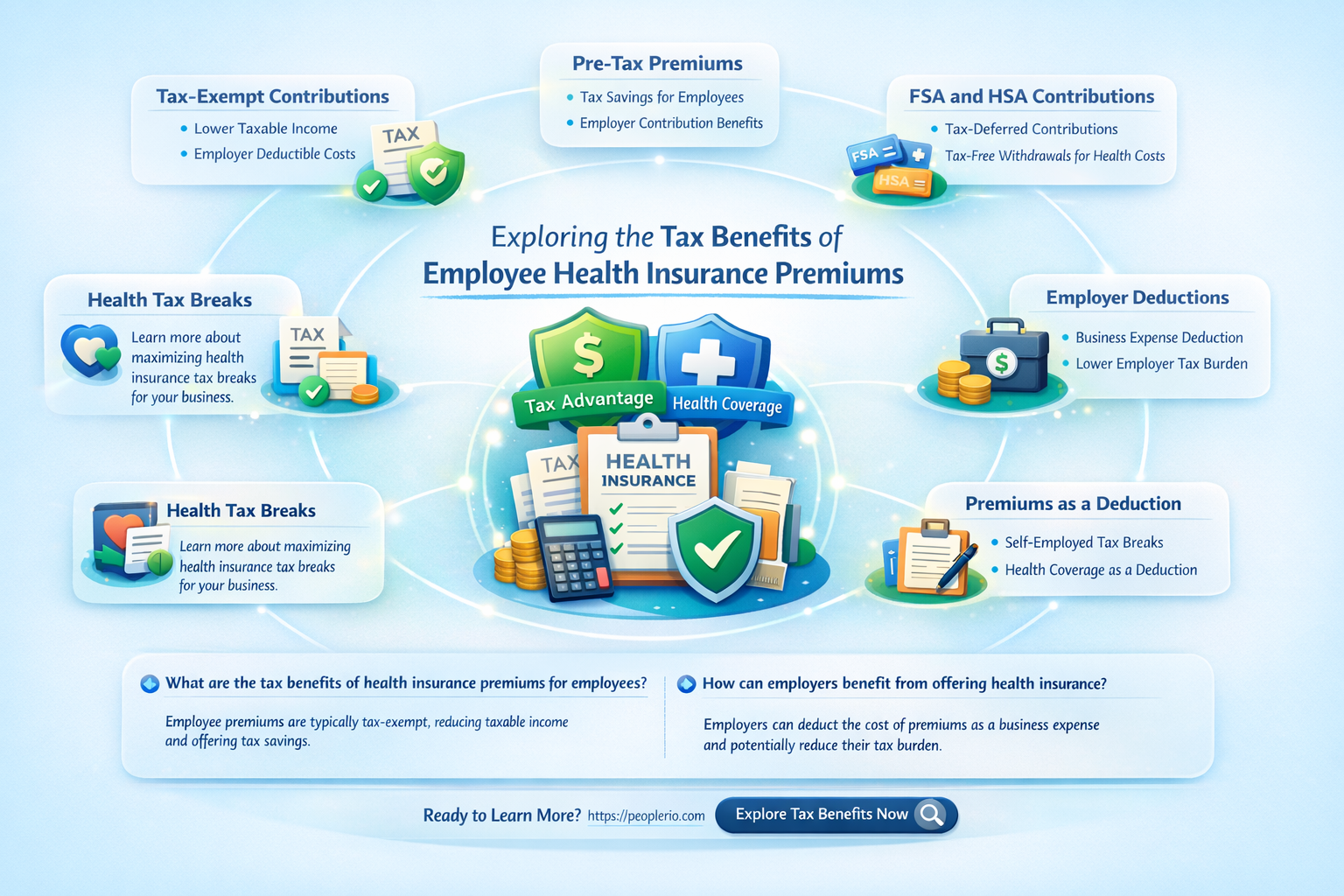

Employee health insurance premiums can be a significant expense for many individuals. Understanding whether these premiums are tax-deductible is crucial for managing personal finances and maximizing potential savings. In general, health insurance premiums paid by employees are not deductible on their federal income tax return. However, there are certain circumstances and specific types of health insurance plans where deductions may be possible. For instance, if an employee pays for health insurance out of pocket and itemizes their deductions, they may be able to deduct the premiums if they exceed a certain percentage of their adjusted gross income. Additionally, contributions to Health Savings Accounts (HSAs) or Flexible Spending Accounts (FSAs) can offer tax advantages. It's essential to consult with a tax professional or refer to the latest tax laws to determine the specific rules and limitations regarding the deductibility of employee health insurance premiums.

| Characteristics | Values |

|---|---|

| Deductibility | Generally tax-deductible for businesses |

| Applies to | Employer-sponsored health insurance premiums |

| Limitations | Must be for employees, not for self-employed individuals |

| Documentation | Requires proper documentation and records |

| Tax Form | Reported on Form W-2 |

| Impact on | Reduces taxable income for businesses |

| Eligibility | Depends on the type of health plan and compliance with IRS rules |

| Contribution Limits | No specific limits, but must be reasonable and customary |

Explore related products

What You'll Learn

- General Rule: Employee health insurance premiums are generally not tax-deductible for individuals

- Exceptions: Certain exceptions apply, such as if the premiums are part of a Health Savings Account (HSA)

- Employer Deductions: Employers can deduct health insurance premiums paid for employees as a business expense

- Self-Employed Individuals: Self-employed individuals may be able to deduct health insurance premiums as a business expense

- Tax Credits: Individuals may be eligible for tax credits to help offset the cost of health insurance premiums

![]()

General Rule: Employee health insurance premiums are generally not tax-deductible for individuals

Employee health insurance premiums are generally not tax-deductible for individuals, which means that the money you pay for your health insurance coverage is not eligible for a tax deduction. This is because the premiums are considered a personal expense, rather than a business expense. However, there are some exceptions to this general rule.

One exception is if you are self-employed. In this case, you may be able to deduct your health insurance premiums as a business expense. This is because you are responsible for providing your own health insurance coverage, and the premiums are a necessary cost of doing business. Another exception is if you are enrolled in a health savings account (HSA) or a flexible spending account (FSA). In this case, you may be able to deduct your health insurance premiums as a contribution to these accounts.

It's important to note that the rules surrounding employee health insurance premiums and tax deductions can be complex. It's always a good idea to consult with a tax professional or your employer's benefits department to determine your specific situation. They can help you understand the rules and regulations that apply to you and ensure that you are taking advantage of any available tax benefits.

In summary, while employee health insurance premiums are generally not tax-deductible for individuals, there are some exceptions to this rule. Self-employed individuals and those enrolled in HSAs or FSAs may be able to deduct their premiums as a business expense or a contribution to these accounts. It's important to consult with a tax professional or your employer's benefits department to determine your specific situation and ensure that you are taking advantage of any available tax benefits.

Understanding the Tax Implications of Non-Employee Compensation

You may want to see also

Explore related products

![]()

Exceptions: Certain exceptions apply, such as if the premiums are part of a Health Savings Account (HSA)

In the realm of tax deductions, employee health insurance premiums often come with certain exceptions. One such exception is when these premiums are part of a Health Savings Account (HSA). HSAs are tax-advantaged accounts used for saving and paying for qualified medical expenses. Contributions to an HSA are tax-deductible, and the earnings grow tax-free. When an employee's health insurance premiums are paid through an HSA, they may not be eligible for the standard tax deduction.

To navigate this exception, it's crucial to understand the specifics of HSA eligibility and contribution limits. For instance, in 2023, the annual contribution limit for an individual with self-only coverage is $3,850, while for family coverage, it's $7,750. Employees aged 55 or older can make additional "catch-up" contributions of up to $1,000. These limits are subject to change, so it's essential to stay informed about any updates.

Another key aspect to consider is the impact of HSA contributions on other tax credits or deductions. For example, if an employee is also eligible for the Premium Tax Credit (PTC), they must carefully evaluate whether contributing to an HSA would affect their PTC eligibility. In some cases, it may be more beneficial to forego HSA contributions to maintain PTC eligibility, depending on the individual's specific circumstances.

Employers also play a role in this exception. They must ensure that their employees are aware of the tax implications of paying health insurance premiums through an HSA. This includes providing clear communication about HSA eligibility, contribution limits, and any potential impacts on other tax benefits. Employers may also need to adjust their payroll systems to accommodate HSA contributions and ensure accurate tax reporting.

In conclusion, while employee health insurance premiums are generally tax-deductible, exceptions like those related to HSAs require careful consideration. Employees and employers alike must understand the intricacies of HSA eligibility, contribution limits, and potential impacts on other tax benefits to make informed decisions and maximize their tax advantages.

Maximizing Tax Benefits: A Guide to Reporting Employee Retention Credit

You may want to see also

Explore related products

$59.99 $74.99

![]()

Employer Deductions: Employers can deduct health insurance premiums paid for employees as a business expense

Employers can deduct health insurance premiums paid for employees as a business expense, which is a significant benefit for both the employer and the employee. This deduction is allowed under the Internal Revenue Code (IRC) Section 162, which states that businesses can deduct ordinary and necessary expenses related to their operations. Health insurance premiums for employees fall under this category, as they are considered a necessary expense for attracting and retaining talent.

To qualify for this deduction, the health insurance plan must meet certain requirements. First, it must be a qualified health plan, which means it must provide minimum essential coverage and meet the affordability and eligibility requirements under the Affordable Care Act (ACA). Second, the employer must pay the premiums directly to the insurance provider or reimburse the employee for the premiums paid. If the employer reimburses the employee, it must do so through a formal reimbursement arrangement, such as a health reimbursement arrangement (HRA) or a health savings account (HSA).

The deduction for health insurance premiums is not limited to a specific dollar amount, but it is subject to certain rules and limitations. For example, the employer cannot deduct the portion of the premium that is paid with pre-tax dollars from the employee's salary. Additionally, the employer cannot deduct the cost of health insurance premiums for employees who are covered under a government-sponsored health plan, such as Medicare or Medicaid.

Employers can also deduct the cost of health insurance premiums for their employees' spouses and dependents, as long as the plan meets the requirements for qualified health coverage. This can be a valuable benefit for employees, as it can help them save money on their health insurance costs.

In conclusion, the ability to deduct health insurance premiums as a business expense is a valuable benefit for employers and employees alike. It can help employers attract and retain talent, while also providing employees with affordable health coverage. However, it is important for employers to understand the rules and limitations surrounding this deduction to ensure they are in compliance with the law.

Smart Tax Strategies: How a W2 Employee Reduced His Taxes

You may want to see also

Explore related products

![]()

Self-Employed Individuals: Self-employed individuals may be able to deduct health insurance premiums as a business expense

Self-employed individuals often face unique challenges when it comes to managing their finances and tax obligations. One area where they may be able to benefit is by deducting health insurance premiums as a business expense. This can be a significant advantage, as health insurance costs can be substantial, and being able to deduct these expenses can help reduce their overall tax liability.

To qualify for this deduction, self-employed individuals must meet certain criteria. Firstly, they must be self-employed and not an employee of another company. This means that they are responsible for paying their own health insurance premiums, rather than having them paid by an employer. Additionally, the health insurance plan must be established under the business name, and the premiums must be paid directly by the business.

The deduction for health insurance premiums is available to self-employed individuals who file Form 1040 with Schedule C. The amount of the deduction is limited to the actual cost of the health insurance premiums paid during the tax year, and it cannot exceed the net profit of the business. This means that self-employed individuals cannot deduct more than they earn from their business.

It is important to note that this deduction is only available for health insurance premiums paid for the self-employed individual and their dependents. Premiums paid for employees of the business are not eligible for this deduction, as they are considered a separate business expense.

Self-employed individuals should keep accurate records of their health insurance premiums paid throughout the year, as well as any other relevant documentation, such as the health insurance policy and proof of payment. This will help ensure that they are able to take advantage of this valuable tax deduction when filing their taxes.

In conclusion, self-employed individuals may be able to deduct health insurance premiums as a business expense, which can help reduce their overall tax liability. However, it is important to meet the specific criteria and keep accurate records to ensure eligibility for this deduction.

Are Employee Bonuses Tax Deductible? A Comprehensive Guide for Employers

You may want to see also

Explore related products

![]()

Tax Credits: Individuals may be eligible for tax credits to help offset the cost of health insurance premiums

Individuals may be eligible for tax credits to help offset the cost of health insurance premiums, providing a significant financial benefit. These tax credits are typically designed to assist lower and middle-income individuals and families in affording health coverage. The amount of the tax credit varies based on factors such as income level, family size, and the cost of premiums in the area.

To qualify for these tax credits, individuals must meet certain criteria. For instance, they must not be eligible for employer-sponsored health insurance or Medicaid. Additionally, they must purchase health insurance through a designated marketplace or exchange. The tax credit can be applied directly to the monthly premium, reducing the out-of-pocket cost for the insured.

One of the key aspects of these tax credits is that they are refundable. This means that if the credit exceeds the amount of taxes owed, the individual can receive the difference as a refund. This feature makes the tax credit particularly valuable for those with limited tax liability.

It's important to note that the availability and specifics of these tax credits can vary by location. Some states have their own tax credit programs in addition to federal options. Individuals should consult with a tax professional or use online resources to determine their eligibility and the best way to claim these credits.

In summary, tax credits for health insurance premiums can significantly reduce the financial burden of obtaining health coverage. By understanding the eligibility requirements and application process, individuals can take advantage of these valuable financial incentives.

Understanding Household Employees: Tax Implications and Responsibilities Explained

You may want to see also

Frequently asked questions

Yes, employee health insurance premiums are generally tax deductible for the employer as a business expense. This deduction helps reduce the employer's taxable income, providing a financial benefit for offering health insurance to employees.

In most cases, employee health insurance premiums are not tax deductible for the employee. However, if an employee pays for health insurance out-of-pocket and itemizes their deductions on their tax return, they may be able to deduct the premiums if they exceed a certain percentage of their adjusted gross income.

Employer-paid health insurance premiums are considered a tax-free benefit for employees. This means that the premiums are not included in the employee's taxable income, reducing their overall tax liability. Additionally, the employer can deduct the premiums as a business expense, which lowers their taxable income as well.

The Affordable Care Act (ACA) introduced several changes to the tax deductibility of health insurance premiums. For example, it increased the percentage of adjusted gross income that medical expenses, including health insurance premiums, must exceed to be deductible for individuals. Additionally, the ACA implemented new rules for employer-sponsored health insurance, such as the requirement for employers to provide a certain level of coverage or face penalties. These changes have affected how both employers and employees approach health insurance premiums and tax deductions.