Employee SEP (Simplified Employee Pension) contributions are indeed pre-tax. This means that the money an employee contributes to their SEP plan is deducted from their gross income before taxes are calculated. As a result, these contributions lower the employee's taxable income, which can lead to a reduction in their overall tax liability. This pre-tax treatment is a significant benefit of SEP plans, as it allows employees to save for retirement while also reducing their current tax burden.

Explore related products

![[ { FIGHTING ARMIES: ANTAGONISTS IN THE MIDDLE EAST: A COMBAT ASSESSMENT (CONTRIBUTIONS IN MILITARY HISTORY) } ] by Unknown (AUTHOR) Sep-27-1983 [ Hardcover ]](https://m.media-amazon.com/images/I/31KbkxZCs-L._AC_UY218_.jpg)

![{ [ VOTING IN REVOLUTIONARY AMERICA: A STUDY OF ELECTIONS IN THE ORIGINAL THIRTEEN STATES, 1776-1789 (CONTRIBUTIONS TO THE STUDY OF RELIGION, #99) ] } Dinkin, Robert J ( AUTHOR ) Sep-29-1982 Hardcover](https://m.media-amazon.com/images/I/41zj1crF4mL._AC_UY218_.jpg)

What You'll Learn

- Definition of SEP Contributions: Understand what SEP (Simplified Employee Pension) contributions are and how they work

- Tax Advantages: Explore the tax benefits of making SEP contributions, including their pre-tax nature

- Eligibility Criteria: Learn who is eligible to make SEP contributions and the requirements for participation

- Contribution Limits: Discover the maximum amount that can be contributed to a SEP plan annually

- Impact on Retirement: Analyze how SEP contributions can affect retirement savings and future financial planning

![]()

Definition of SEP Contributions: Understand what SEP (Simplified Employee Pension) contributions are and how they work

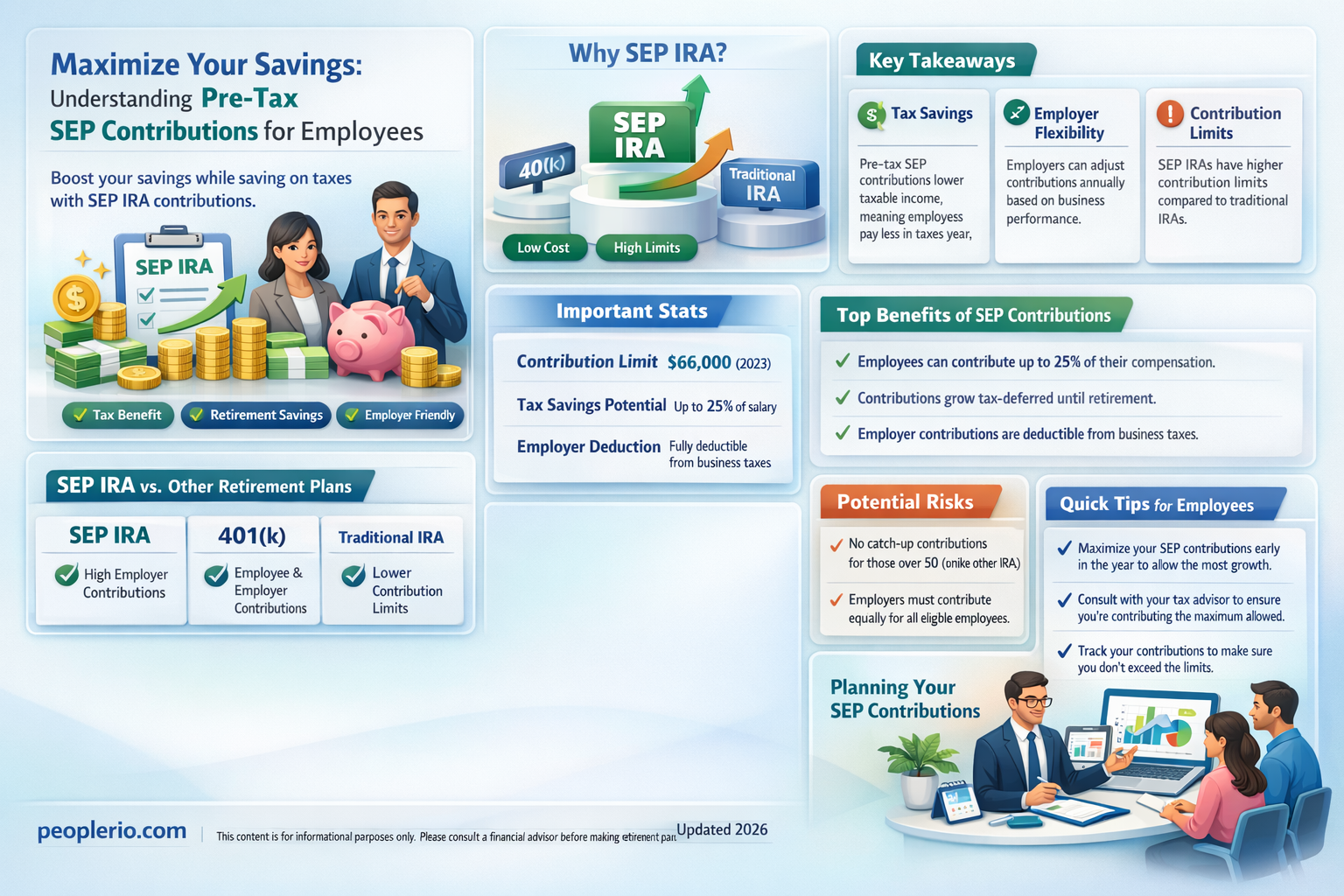

SEP contributions refer to the payments made into a Simplified Employee Pension plan, a type of retirement savings plan available to self-employed individuals and small business owners. These contributions are a crucial aspect of the plan, as they determine the amount of money that will be available for retirement. The contributions are made on a pre-tax basis, which means that the money is deducted from the contributor's taxable income before taxes are calculated. This can provide a significant tax advantage, as it reduces the amount of income that is subject to taxation.

The amount that can be contributed to an SEP plan is based on a percentage of the contributor's net earnings from self-employment. The maximum contribution limit is set by the IRS and can change from year to year. It's important to note that the contributions are not mandatory, but they are highly recommended to ensure a comfortable retirement. The funds contributed to an SEP plan can be invested in a variety of assets, such as stocks, bonds, and mutual funds, allowing the account to grow over time.

One of the key benefits of SEP contributions is that they are tax-deductible. This means that the amount contributed can be subtracted from the contributor's taxable income, reducing the overall tax liability. Additionally, the earnings on the contributions grow on a tax-deferred basis, meaning that taxes are not paid on the investment gains until the money is withdrawn from the plan. This can lead to significant tax savings over time.

It's also important to understand that SEP contributions are not the same as other types of retirement plan contributions, such as those made to a 401(k) or IRA. SEP plans are specifically designed for self-employed individuals and small business owners, and they offer unique benefits and contribution limits. When making SEP contributions, it's essential to work with a financial advisor or tax professional to ensure that the contributions are made correctly and in accordance with IRS regulations.

In summary, SEP contributions are a vital component of a Simplified Employee Pension plan, offering tax advantages and a way to save for retirement. By understanding how these contributions work and the benefits they provide, self-employed individuals and small business owners can make informed decisions about their retirement savings.

Tax Savings Guide for 1099 Employees: Smart Strategies for Financial Peace

You may want to see also

Explore related products

![]()

Tax Advantages: Explore the tax benefits of making SEP contributions, including their pre-tax nature

SEP contributions offer significant tax advantages, primarily due to their pre-tax nature. When an employer makes a SEP contribution, it is deducted from their taxable income, reducing the overall tax liability for the business. This deduction is available even if the employer has already contributed to other retirement plans, such as a 401(k).

For employees, SEP contributions are also pre-tax, meaning they are not included in the employee's gross income for the year. This reduces the employee's taxable income, potentially lowering their tax bracket and overall tax burden. Additionally, the earnings on SEP contributions grow tax-deferred, allowing the investment to compound more quickly than if it were subject to annual taxation.

One of the key benefits of SEP plans is their flexibility. Employers can choose to make contributions up to 25% of an employee's compensation, up to a maximum of $66,000 in 2023. This allows businesses to tailor their contributions to fit their financial situation and the needs of their employees. Furthermore, SEP contributions can be made retroactively, giving employers the opportunity to make up for missed contributions in previous years.

SEP plans also offer a unique advantage for self-employed individuals. Unlike traditional retirement plans, SEPs allow self-employed individuals to contribute up to 20% of their net self-employment income, providing a valuable tax-saving opportunity for those who are self-employed or have a side gig.

In summary, the tax advantages of SEP contributions are substantial. By reducing taxable income for both employers and employees, SEP plans offer a powerful tool for tax planning and retirement savings. The flexibility of SEP contributions, combined with their pre-tax nature and tax-deferred growth, make them an attractive option for businesses and individuals looking to maximize their retirement savings while minimizing their tax liability.

Exploring the Tax Benefits of Employee Health Insurance Premiums

You may want to see also

Explore related products

![Sep [Blu-Ray]+[KSIÄĹťKA] (IMPORT) (No English version)](https://m.media-amazon.com/images/I/811IWh9EWWL._AC_UY218_.jpg)

![The Vulture (2013) ( Sep ) [ Blu-Ray, Reg.A/B/C Import - Poland ]](https://m.media-amazon.com/images/I/51WzGnVT1jL._AC_UY218_.jpg)

![]()

Eligibility Criteria: Learn who is eligible to make SEP contributions and the requirements for participation

To contribute to a Simplified Employee Pension (SEP) plan, certain eligibility criteria must be met. Firstly, the employee must be at least 21 years old. This age requirement ensures that participants are likely to have a stable income and are at an appropriate stage in their careers to start saving for retirement. Additionally, the employee must have worked for the employer for at least three years. This tenure requirement helps to ensure that the SEP plan is not overly burdened by frequent turnover and that participants have a vested interest in the company.

Another key criterion is that the employee must have earned at least $650 in compensation from the employer in the previous year. This minimum earnings requirement helps to ensure that participants have sufficient income to make meaningful contributions to the plan. It also helps to prevent the plan from becoming too administratively burdensome by limiting participation to those who are likely to be able to contribute a significant amount.

The employer must also meet certain requirements in order to establish and maintain an SEP plan. Firstly, the employer must have been in business for at least three years. This requirement helps to ensure that the plan is established by a stable and reputable company. Additionally, the employer must have a written SEP plan document that outlines the terms and conditions of the plan, including the eligibility criteria, contribution limits, and vesting schedule. This document must be provided to all eligible employees and must be updated as necessary to reflect any changes to the plan.

In terms of participation, employees who meet the eligibility criteria are automatically enrolled in the SEP plan. However, they do have the option to opt out if they choose. Employers are required to provide eligible employees with a notice explaining the terms and conditions of the plan, as well as their rights and responsibilities as participants. This notice must be provided at least 30 days before the employee's first contribution is made.

Overall, the eligibility criteria for SEP contributions are designed to ensure that the plan is accessible to employees who are likely to benefit from it the most, while also minimizing the administrative burden on the employer. By meeting these criteria, employees can take advantage of a valuable retirement savings opportunity and employers can provide a competitive benefit to attract and retain top talent.

Mastering Employee Tax Filing: A Step-by-Step Guide for Employers

You may want to see also

Explore related products

![(Little Master Tolstoy: Anna Karenina (BabyLit)) [By: Jennifer Adams] [Sep, 2013]](https://m.media-amazon.com/images/I/51nt0zW5WoL._AC_UY218_.jpg)

![[(The Boy Who Cried Wolf: Pink B/Band 01b )] [Author: Saffy Jenkins] [Sep-2013]](https://m.media-amazon.com/images/I/51hE2rcpt2L._AC_UY218_.jpg)

![[(Edmund Campion: Hero of God's Underground * * )] [Author: Harold Gardiner] [Sep-1992]](https://m.media-amazon.com/images/I/51OZQcpSAVL._AC_UY218_.jpg)

![[(I've Just Had a Bright Idea!: Green/Band 05 )] [Author: Scoular Anderson] [Sep-2010]](https://m.media-amazon.com/images/I/518f+VMP-EL._AC_UY218_.jpg)

![]()

Contribution Limits: Discover the maximum amount that can be contributed to a SEP plan annually

The contribution limits for a Simplified Employee Pension (SEP) plan are a critical aspect for both employers and employees to understand. As of the latest IRS guidelines, the maximum annual contribution an employer can make to an employee's SEP plan is the lesser of 25% of the employee's compensation or $66,000 for the year 2023. This limit is subject to change based on annual IRS adjustments for inflation.

For employees, the contribution limit is based on their earned income. They can contribute up to 10% of their compensation, but this percentage can be reduced if their income exceeds certain thresholds. It's important to note that these contributions are made on a pre-tax basis, which means they are deducted from the employee's gross income before taxes are calculated. This can significantly reduce the employee's taxable income, providing a substantial tax benefit.

Employers have the flexibility to contribute different amounts to different employees' SEP plans, allowing them to tailor their contributions based on factors such as employee tenure, salary, or performance. However, they must adhere to the IRS contribution limits and ensure that their contributions do not exceed the maximum allowed amount.

Understanding these contribution limits is essential for maximizing the benefits of a SEP plan. Employers and employees should consult with a financial advisor or tax professional to ensure they are making the most informed decisions regarding their SEP plan contributions. By doing so, they can optimize their retirement savings while also taking advantage of the tax benefits offered by these plans.

Understanding Pre-Tax Employee Health Insurance Contributions

You may want to see also

![]()

Impact on Retirement: Analyze how SEP contributions can affect retirement savings and future financial planning

SEP contributions can have a profound impact on retirement savings and future financial planning. By contributing to a SEP IRA, employees can significantly boost their retirement funds due to the tax advantages and potential for employer matching contributions. The pre-tax nature of SEP contributions allows employees to reduce their taxable income, thereby lowering their tax liability in the contribution year. This can be particularly beneficial for those in higher tax brackets.

Moreover, SEP IRAs offer flexibility in terms of contribution amounts and timing, which can be advantageous for employees with variable incomes or those who want to maximize their retirement savings during peak earning years. The funds within a SEP IRA grow tax-deferred, allowing for compound interest to work its magic over time. This can result in a substantial nest egg by retirement age.

However, it's important to consider the impact of SEP contributions on overall financial planning. While contributing to a SEP IRA can reduce taxable income in the short term, it also means that the funds will be subject to taxation upon withdrawal in retirement. This requires careful planning to ensure that the retiree is prepared for the tax implications of their SEP IRA distributions.

Additionally, employees should be aware of the potential for required minimum distributions (RMDs) from their SEP IRA starting at age 72 (as of 2021). These RMDs can impact the retiree's tax situation and should be factored into their retirement income strategy.

In conclusion, SEP contributions can be a powerful tool for retirement savings, offering tax advantages and flexibility. However, they also require careful consideration in the context of overall financial planning, particularly with regard to future tax liabilities and retirement income strategies.

Unlocking the Tax Benefits of Employee Christmas Bonuses

You may want to see also

Frequently asked questions

Yes, employee contributions to a Simplified Employee Pension (SEP) plan are made on a pre-tax basis. This means that the contributions are deducted from your gross income before taxes are calculated, which can lower your taxable income and potentially reduce your tax liability.

Since SEP contributions are pre-tax, they reduce your gross income, which in turn lowers your taxable income. This can result in a higher take-home pay because less money is withheld for taxes. However, it's important to note that while your take-home pay may be higher, you are also setting aside funds for your retirement.

Yes, there are contribution limits for SEP plans. As of 2023, the maximum contribution is the lesser of 25% of your compensation or $66,000. It's important to check with your plan administrator or a financial advisor to ensure you are contributing within these limits.