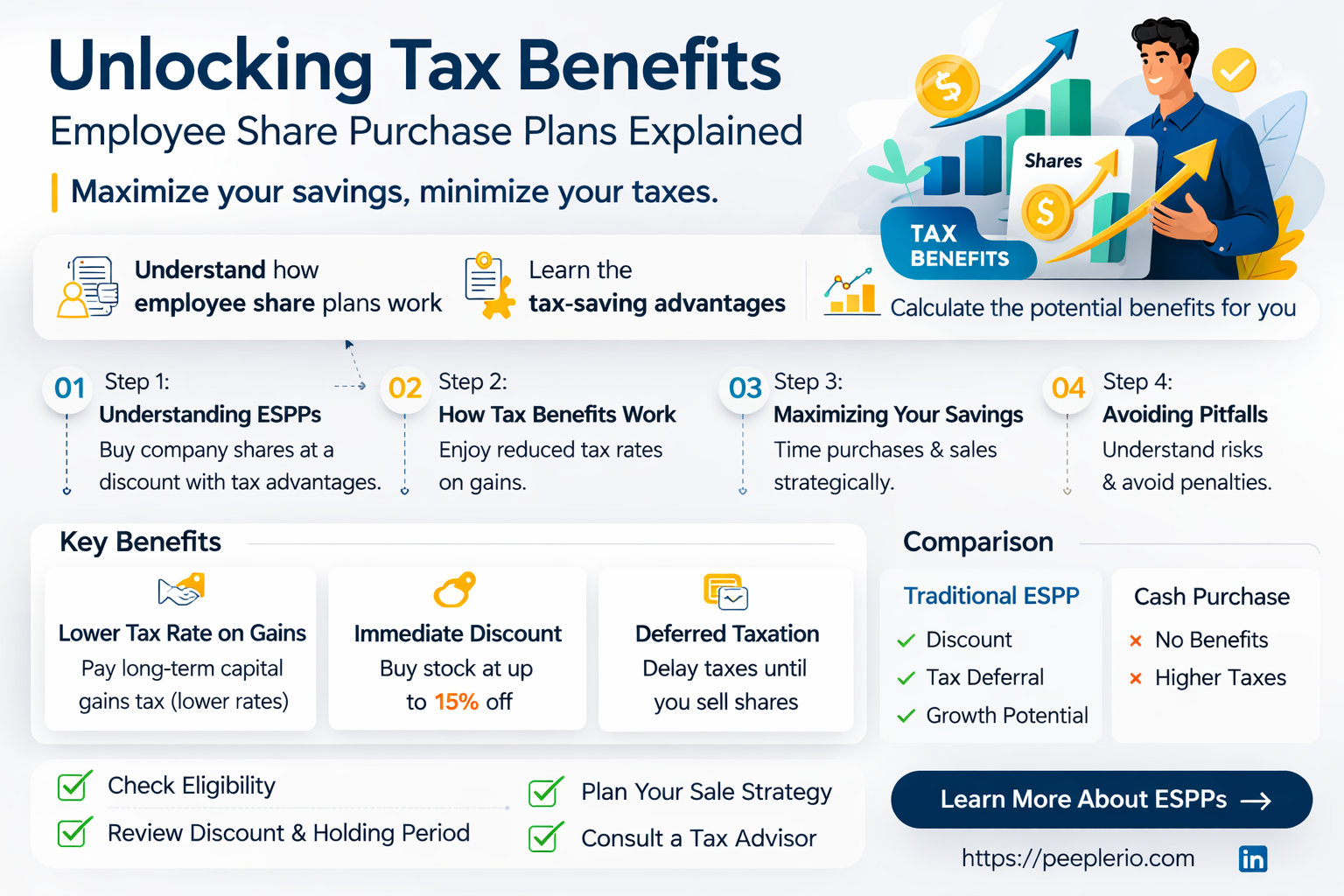

Employee share purchase plans (ESPPs) are a popular benefit offered by many companies, allowing employees to purchase company stock at a discounted rate. One of the key advantages of ESPPs is their tax efficiency. Contributions to an ESPP are typically made through payroll deductions, which can reduce an employee's taxable income. Additionally, the gains realized from the sale of ESPP shares are often subject to favorable tax treatment, such as capital gains rates or even tax-free growth in some cases. However, the specific tax implications of ESPPs can vary depending on the country and its tax laws, as well as the terms of the individual plan. It is essential for employees to understand the tax consequences of participating in an ESPP to make informed decisions about their investments.

| Characteristics | Values |

|---|---|

| Tax Deductibility | Employee share purchase plans are generally tax-deductible, but the specifics can vary by country and plan type. |

| Country-Specific Rules | In the United States, contributions to ESPPs (Employee Stock Purchase Plans) are not tax-deductible, but the earnings grow tax-free until withdrawal. |

| Plan Type | Different types of employee share purchase plans, such as ESPPs and 401(k) plans with company stock options, have varying tax implications. |

| Contribution Limits | There are often limits on how much an employee can contribute to these plans annually, which can affect the overall tax benefit. |

| Holding Period | Some plans require a certain holding period before the shares can be sold, which may impact the tax treatment of any gains. |

| Tax Treatment of Gains | Gains from the sale of shares purchased through these plans are typically subject to capital gains tax, but the rate can vary depending on the holding period. |

| Impact on Income Tax | Contributions to some plans may reduce an employee's taxable income, while others may not have this benefit. |

| Employer Contributions | If an employer matches contributions, these may also be tax-deductible for the employer and tax-free for the employee. |

| Withdrawal Rules | The rules for withdrawing funds or shares from the plan can affect the tax implications, with some plans allowing for penalty-free withdrawals under certain conditions. |

| Reporting Requirements | Employees and employers may need to report contributions and withdrawals on tax forms, ensuring compliance with tax regulations. |

| Potential Penalties | Non-compliance with contribution limits or withdrawal rules can result in tax penalties or loss of tax benefits. |

| Consultation with Tax Advisor | Due to the complexity of tax laws, it is advisable for employees and employers to consult with a tax advisor to understand the specific implications of their share purchase plan. |

Explore related products

What You'll Learn

- General Overview: Employee share purchase plans: definition, types, and their role in employee compensation

- Tax Deductibility: Conditions under which employee share purchase plans are considered tax-deductible

- Benefits to Employees: How tax-deductible share purchase plans benefit employees financially

- Employer Considerations: What employers need to consider when implementing tax-deductible share purchase plans

- Regulatory Compliance: Legal and regulatory requirements for tax-deductible employee share purchase plans

![]()

General Overview: Employee share purchase plans: definition, types, and their role in employee compensation

Employee share purchase plans (ESPPs) are a type of employee benefit that allows workers to purchase company stock at a discounted rate. These plans are designed to incentivize employees to invest in their employer's success and to align their interests with those of the company's shareholders. ESPPs can take various forms, but they generally involve the company offering shares to employees at a price below the market value, often through payroll deductions.

There are two primary types of ESPPs: qualified and non-qualified. Qualified ESPPs meet specific criteria set by the Internal Revenue Service (IRS) and offer certain tax advantages. Non-qualified ESPPs do not meet these criteria and may not provide the same tax benefits. Qualified ESPPs are more common and are typically structured to comply with IRS regulations, which can include restrictions on the amount of stock that can be purchased and the length of time employees must hold the stock before selling.

ESPPs play a significant role in employee compensation by providing workers with an opportunity to share in the company's growth and profitability. They can also serve as a retention tool, encouraging employees to stay with the company long enough to vest in their stock options. Additionally, ESPPs can help to foster a sense of ownership and engagement among employees, as they become partial owners of the company.

When considering whether ESPPs are tax-deductible, it's important to distinguish between the tax treatment of qualified and non-qualified plans. Qualified ESPPs offer tax advantages because they meet IRS criteria, which can include tax deductions for the company and favorable tax treatment for employees when they sell their stock. Non-qualified ESPPs, on the other hand, may not provide the same tax benefits and could be subject to different tax rules.

In summary, ESPPs are a valuable employee benefit that can align workers' interests with those of the company and provide an opportunity for investment and growth. The tax deductibility of ESPPs depends on whether the plan is qualified or non-qualified, with qualified plans offering more favorable tax treatment.

Unlocking the Benefits: Are Employee Roth 401(k) Contributions Tax-Free?

You may want to see also

Explore related products

![]()

Tax Deductibility: Conditions under which employee share purchase plans are considered tax-deductible

Employee share purchase plans can indeed be tax-deductible under certain conditions. To qualify for tax deductions, these plans must meet specific criteria set by the tax authorities. One key condition is that the plan must be offered to all employees, not just a select few. This ensures fairness and equal opportunity for all staff members to participate in the tax benefits.

Another important criterion is that the shares purchased through the plan must be held for a minimum period, typically at least five years. This holding period requirement prevents employees from quickly selling the shares and taking advantage of short-term tax benefits. Additionally, the plan must not provide any immediate financial benefit to the employees, such as dividends or interest, until the shares are sold.

The tax deductibility of employee share purchase plans also depends on the type of shares being purchased. Generally, the shares must be in a company that is listed on a recognized stock exchange. This ensures that the shares have a fair market value and are subject to market fluctuations, which is important for tax purposes.

Furthermore, the plan must be structured in a way that it does not provide any guaranteed returns or protection against losses. This means that employees must bear the full risk of the investment, which aligns with the principles of fair taxation. Any contributions made by the employer towards the plan may also be subject to tax deductions, provided they are not excessive and are in line with the overall remuneration package of the employee.

In conclusion, while employee share purchase plans can offer tax benefits, they must meet strict conditions to ensure fairness and compliance with tax regulations. Employers and employees should carefully consider these conditions before implementing or participating in such plans to maximize their tax advantages while minimizing potential risks.

Unlocking the Perks: Are Employee Benefits Tax Deferred?

You may want to see also

Explore related products

$14.99 $25

![]()

Benefits to Employees: How tax-deductible share purchase plans benefit employees financially

Tax-deductible share purchase plans offer significant financial benefits to employees, primarily through the reduction of taxable income. When employees participate in these plans, they are often allowed to purchase company shares at a discounted rate, which can lead to substantial savings over time. The contributions made by employees towards these share purchases are typically deducted from their gross income, thereby lowering their overall tax liability. This immediate tax benefit can enhance employees' take-home pay, providing them with more disposable income.

Moreover, these plans can foster a sense of ownership and investment among employees, potentially leading to increased job satisfaction and loyalty. As employees accumulate shares, they may also benefit from dividends, which can serve as an additional source of income. Over the long term, the appreciation of these shares can contribute to employees' wealth accumulation, offering a valuable component to their retirement savings.

Another key advantage is the potential for employees to benefit from capital gains tax rates, which are often lower than ordinary income tax rates. If employees hold their shares for a certain period, typically more than a year, any gains realized upon the sale of these shares may be taxed at a reduced rate. This can result in further tax savings and increase the overall financial benefit of participating in the share purchase plan.

Furthermore, tax-deductible share purchase plans can provide employees with a disciplined approach to saving and investing. By automatically deducting contributions from their paychecks, employees are more likely to maintain consistent savings habits. This can help them build a substantial investment portfolio over time, which can be particularly beneficial for long-term financial goals such as retirement, education expenses, or major purchases.

In summary, tax-deductible share purchase plans offer employees a range of financial benefits, including reduced taxable income, increased disposable income, potential for dividends and capital gains, and a structured approach to saving and investing. These advantages can contribute to employees' overall financial well-being and security.

Maximize Your Savings: Understanding Pre-Tax SEP Contributions for Employees

You may want to see also

Explore related products

$17.98 $25

![]()

Employer Considerations: What employers need to consider when implementing tax-deductible share purchase plans

When implementing tax-deductible share purchase plans, employers must carefully consider the legal and financial implications to ensure compliance with relevant tax laws and regulations. This involves understanding the specific requirements and limitations imposed by tax authorities, such as the Internal Revenue Service (IRS) in the United States. Employers should consult with tax professionals to determine the eligibility of their plan and to ensure that all necessary documentation and reporting are accurately completed.

One key consideration for employers is the impact of tax-deductible share purchase plans on their financial statements. These plans can affect the company's cash flow, as well as its balance sheet and income statement. Employers must be prepared to account for the costs associated with the plan, including any administrative fees, brokerage commissions, and the potential dilution of existing shareholders' equity. Additionally, employers should consider the potential benefits of tax-deductible share purchase plans, such as increased employee engagement and retention, as well as the potential for improved financial performance through increased employee ownership.

Employers must also consider the communication and education aspects of implementing tax-deductible share purchase plans. It is essential to clearly communicate the terms and conditions of the plan to employees, including the eligibility criteria, contribution limits, and any vesting requirements. Employers should provide employees with the necessary resources and support to make informed decisions about participating in the plan, including access to financial advisors and educational materials.

Another important consideration for employers is the potential impact of tax-deductible share purchase plans on their company culture and employee morale. These plans can foster a sense of ownership and pride among employees, which can lead to increased motivation and productivity. However, employers must be mindful of the potential for inequality or resentment among employees who may not be eligible to participate in the plan or who may not be able to afford to contribute. Employers should strive to create a plan that is fair and equitable, and that promotes a positive and inclusive company culture.

Finally, employers should consider the long-term implications of tax-deductible share purchase plans, including the potential for future changes in tax laws or regulations that could affect the plan's tax-deductible status. Employers should also consider the potential impact of the plan on their company's succession planning and exit strategy. By carefully weighing these considerations, employers can implement tax-deductible share purchase plans that are both beneficial to their employees and aligned with their company's overall goals and objectives.

Unlocking Tax Benefits: Are Employee Insurance Premiums Deductible?

You may want to see also

Explore related products

![]()

Regulatory Compliance: Legal and regulatory requirements for tax-deductible employee share purchase plans

To qualify for tax-deductibility, employee share purchase plans must adhere to a stringent set of legal and regulatory requirements. These requirements vary by jurisdiction but generally include conditions related to the structure of the plan, the eligibility of participants, and the nature of the shares being purchased. For instance, in the United States, plans must comply with the Internal Revenue Code (IRC) Section 423, which outlines specific rules for tax-qualified employee stock purchase plans. These rules include limitations on the amount of stock that can be purchased, the price at which it can be offered, and the holding period required before the stock can be sold tax-free.

In addition to federal tax laws, employee share purchase plans must also comply with state and local tax regulations, which can add an additional layer of complexity. Some states have their own tax incentives for employee stock ownership plans, while others may impose additional taxes or reporting requirements. Employers must carefully consider these varying regulations when designing and implementing their plans to ensure compliance and maximize tax benefits.

Furthermore, regulatory compliance extends beyond tax laws to include securities regulations and corporate governance standards. Employers must ensure that their plans comply with the Securities Act of 1933 and the Securities Exchange Act of 1934, which regulate the offer and sale of securities. This includes providing participants with accurate and timely information about the company and the terms of the plan. Employers must also comply with corporate governance standards, such as those set forth by the Sarbanes-Oxley Act, which require companies to maintain effective internal controls and ensure the accuracy of financial reporting.

Non-compliance with these legal and regulatory requirements can result in significant penalties, including fines, taxes, and even criminal charges. Employers must therefore take a proactive approach to compliance, regularly reviewing and updating their plans to reflect changes in the law and regulatory environment. This may involve working with legal and tax advisors to ensure that the plan is structured correctly and that all necessary filings and disclosures are made in a timely manner.

In conclusion, regulatory compliance is a critical aspect of tax-deductible employee share purchase plans. Employers must navigate a complex web of federal, state, and local tax laws, securities regulations, and corporate governance standards to ensure that their plans are compliant and provide the intended tax benefits. By taking a proactive approach to compliance and seeking expert advice when needed, employers can minimize the risk of penalties and ensure that their plans are effective and efficient.

Understanding Employee Health Plans: Pre-Tax Benefits Explained

You may want to see also

Frequently asked questions

Contributions to an ESPP are generally not tax-deductible for the employee. However, the specific tax treatment can vary depending on the country's tax laws and the structure of the plan.

Unlike 401(k) contributions, which are typically tax-deductible, ESPP contributions are usually made with after-tax dollars. This means that the employee pays taxes on the contribution amount before it is deducted from their paycheck.

Despite the lack of tax deductibility, ESPPs can offer other tax benefits. For example, the growth of the investment within the plan is often tax-deferred, and qualified distributions may be taxed at a lower rate than ordinary income.

Yes, employees should carefully consider the tax implications of participating in an ESPP. While these plans can be a valuable tool for saving and investing, understanding the tax treatment of contributions, growth, and distributions is essential for making informed financial decisions.