The question of whether an employer can take FICA taxes on an employee's gross wages is a common one in the realm of payroll and tax law. FICA, which stands for Federal Insurance Contributions Act, is a federal payroll tax that funds Social Security and Medicare. Employers are required to withhold FICA taxes from their employees' wages and pay them to the Internal Revenue Service (IRS). The amount withheld is based on the employee's gross wages, which include all compensation paid to the employee before any deductions. This can encompass not only the employee's regular salary or hourly wages but also bonuses, overtime pay, and certain other forms of compensation. Understanding the intricacies of FICA tax withholding is crucial for both employers and employees to ensure compliance with federal tax laws and to avoid potential penalties.

| Characteristics | Values |

|---|---|

| Tax Type | FICA (Federal Insurance Contributions Act) |

| Applicability | Applies to all employees earning gross wages |

| Employer Responsibility | Employers are required to withhold FICA taxes from employees' gross wages |

| Employee Contribution | 6.2% of gross wages for Social Security, 1.45% for Medicare |

| Employer Contribution | 6.2% of gross wages for Social Security, 1.45% for Medicare |

| Maximum Taxable Earnings | $147,000 for Social Security in 2023, no limit for Medicare |

| Filing Frequency | Quarterly |

| Payment Method | Employers must deposit FICA taxes electronically or by check |

| Consequences of Non-Compliance | Penalties and interest may be assessed on late or incorrect payments |

| Employee Impact | Reduces take-home pay, but contributes to Social Security and Medicare benefits |

| Employer Impact | Increases cost of hiring, but ensures compliance with federal tax laws |

| Tax Forms | Form 941 for quarterly reporting, Form W-2 for annual reporting to employees |

| Record Keeping | Employers must maintain records of FICA tax withholdings and payments |

| Audits | Employers may be subject to IRS audits to ensure proper FICA tax withholding and payment |

| Refunds | Employees may be eligible for refunds if they overpay FICA taxes |

| Amendments | Employers must correct any errors in FICA tax reporting and payments |

| Compliance Assistance | Employers can seek guidance from the IRS or a tax professional |

Explore related products

What You'll Learn

- FICA Tax Basics: Understanding the Federal Insurance Contributions Act (FICA) and its components: Social Security and Medicare taxes

- Employer Responsibilities: Employers' obligations to withhold FICA taxes from employees' wages and pay their own FICA taxes

- Employee Gross Wages: Defining gross wages, including salary, tips, bonuses, and other compensation subject to FICA taxes

- FICA Tax Rates: Current FICA tax rates for both employers and employees, and how they are applied to gross wages

- FICA Tax Exemptions: Exploring exemptions and exceptions to FICA taxes, such as certain types of income or specific employee groups

![]()

FICA Tax Basics: Understanding the Federal Insurance Contributions Act (FICA) and its components: Social Security and Medicare taxes

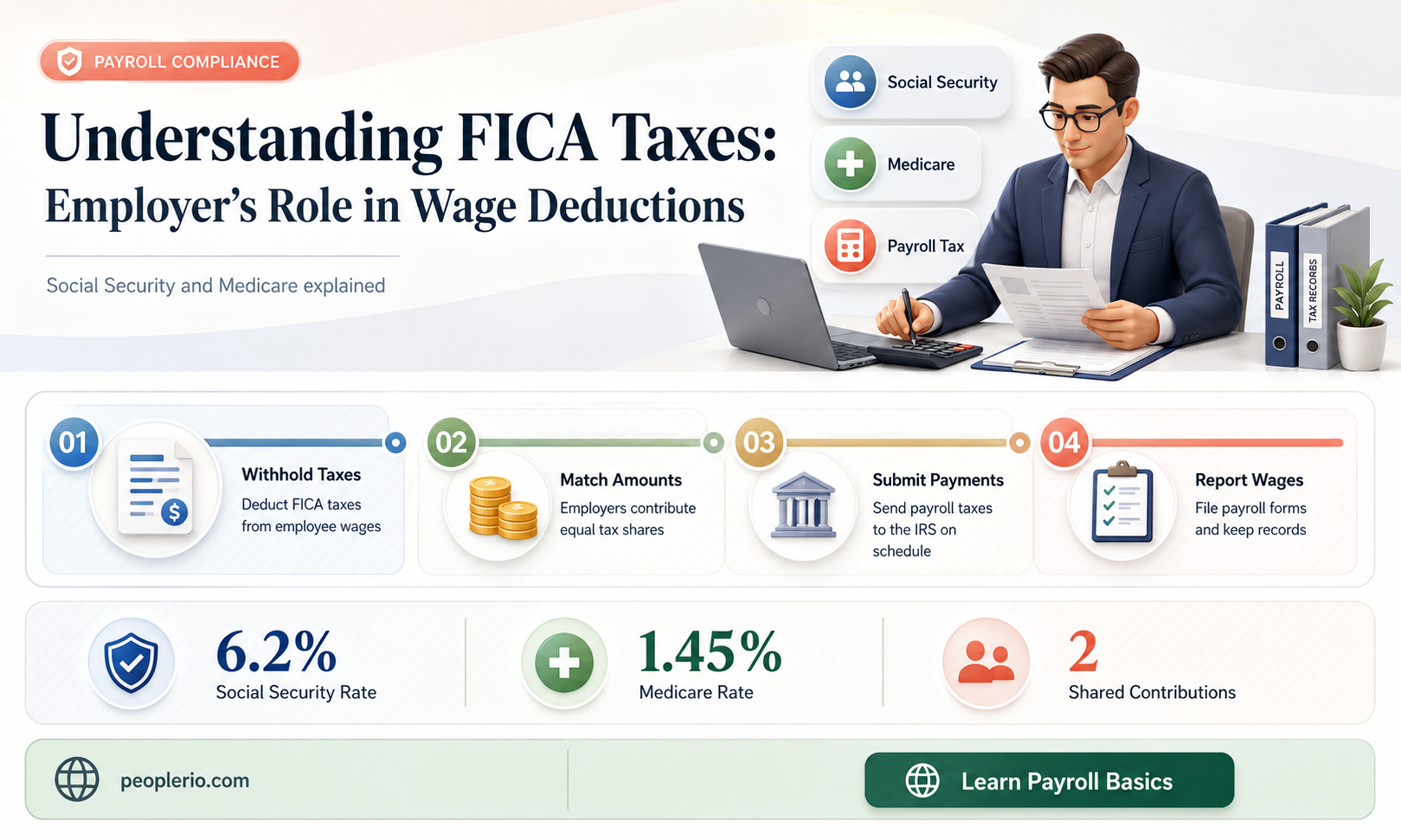

The Federal Insurance Contributions Act (FICA) is a crucial aspect of the U.S. tax system, primarily funding Social Security and Medicare. FICA taxes are levied on both employers and employees, with each party contributing a specific percentage of the employee's gross wages. As of the latest updates, the Social Security tax rate is 6.2% for both employers and employees, while the Medicare tax rate is 1.45% for employees and 1.45% for employers.

Employers are responsible for withholding FICA taxes from their employees' gross wages and submitting these taxes to the IRS. This process involves calculating the tax amounts based on the employee's earnings and ensuring timely payment to avoid penalties. Employers must also match the employee's contributions, which means they pay an equal amount of FICA taxes on top of what is withheld from the employee's paycheck.

One important aspect to note is the wage base limit for Social Security taxes. For 2023, the wage base limit is $147,000, meaning that Social Security taxes are only applied to earnings up to this amount. Any earnings above this limit are not subject to Social Security taxes, although they are still subject to Medicare taxes.

FICA taxes play a significant role in funding the nation's social safety net programs. Social Security provides retirement, disability, and survivor benefits, while Medicare offers health coverage for individuals aged 65 and older, as well as certain younger people with disabilities. By understanding the basics of FICA taxes, both employers and employees can ensure compliance with tax laws and contribute to the sustainability of these vital programs.

In summary, FICA taxes are a mandatory component of the U.S. tax system, with both employers and employees sharing the responsibility of funding Social Security and Medicare. Employers must accurately calculate and withhold FICA taxes from employee wages, match these contributions, and submit the taxes to the IRS to avoid penalties. The wage base limit for Social Security taxes is an important consideration, as it caps the amount of earnings subject to this tax. By comprehending these fundamental aspects of FICA taxes, stakeholders can fulfill their tax obligations and support the nation's social safety net.

Understanding Pre-Tax Employee Health Care Payments: A Comprehensive Guide

You may want to see also

Explore related products

$4.99 $29.99

![]()

Employer Responsibilities: Employers' obligations to withhold FICA taxes from employees' wages and pay their own FICA taxes

Employers have a legal obligation to withhold FICA taxes from their employees' wages. FICA, which stands for Federal Insurance Contributions Act, encompasses both Social Security and Medicare taxes. The current withholding rates are 6.2% for Social Security and 1.45% for Medicare, totaling 7.65% of an employee's gross wages. Employers must deduct these taxes from each paycheck and remit them to the Internal Revenue Service (IRS) on a regular basis.

In addition to withholding FICA taxes from employees, employers are also responsible for paying their own FICA taxes. This means that for every dollar an employer pays an employee, the employer must pay an additional 7.65% in FICA taxes. This can add up quickly, especially for businesses with a large workforce. Employers must ensure that they are accurately calculating and paying these taxes to avoid penalties and interest from the IRS.

One common mistake employers make is failing to withhold FICA taxes from certain types of compensation, such as bonuses, commissions, or overtime pay. It's important for employers to understand that FICA taxes apply to all forms of wages, regardless of how they are classified. Another mistake is failing to pay FICA taxes on time. Employers must remit FICA taxes to the IRS on a quarterly basis, and failure to do so can result in significant penalties.

To avoid these mistakes, employers should consult with a tax professional or use payroll software that can help them accurately calculate and remit FICA taxes. Employers should also stay up-to-date on any changes to FICA tax rates or regulations to ensure compliance. By fulfilling their FICA tax obligations, employers can help ensure that their employees are able to receive Social Security and Medicare benefits when they need them.

Decoding Employee Federal Taxes: Pre-Tax vs. Post-Tax Explained

You may want to see also

Explore related products

![]()

Employee Gross Wages: Defining gross wages, including salary, tips, bonuses, and other compensation subject to FICA taxes

Employee gross wages encompass a broad spectrum of compensation that employees receive from their employers. This includes not only the base salary but also additional forms of remuneration such as tips, bonuses, and other incentives. Gross wages are significant because they form the basis for calculating various taxes, including Federal Insurance Contributions Act (FICA) taxes. FICA taxes are a critical component of the U.S. social security system, funding programs like Social Security and Medicare. Employers are responsible for withholding FICA taxes from employees' gross wages and remitting them to the Internal Revenue Service (IRS).

The calculation of gross wages for FICA tax purposes involves adding up all forms of taxable compensation. This includes wages, salaries, tips, bonuses, and certain other payments that are subject to FICA withholding. It's important to note that not all types of compensation are subject to FICA taxes. For example, certain fringe benefits, such as health insurance premiums paid by the employer, are generally not considered taxable wages for FICA purposes. Additionally, there are wage limits that apply to FICA taxes, meaning that only a certain amount of an employee's wages are subject to these taxes each year.

Employers must accurately determine and report an employee's gross wages to ensure compliance with FICA tax regulations. This involves maintaining detailed records of all payments made to employees and understanding the specific rules that govern what is and isn't considered taxable compensation. Failure to properly calculate and report gross wages can result in penalties and interest charges from the IRS. Moreover, accurate reporting is essential for employees' future social security benefits, as the amount of benefits they receive is based on their lifetime earnings subject to FICA taxes.

In summary, employee gross wages are a comprehensive measure of compensation that includes salary, tips, bonuses, and other taxable payments. Employers have a legal obligation to accurately calculate and report these wages for FICA tax purposes, ensuring that both the employer and employee contribute to the social security system. Understanding the nuances of what constitutes gross wages and the associated tax implications is crucial for compliance with IRS regulations and for the financial well-being of employees.

Exploring the Limits: Can Employees Use Tax-Exempt Status for Personal Gain?

You may want to see also

Explore related products

![]()

FICA Tax Rates: Current FICA tax rates for both employers and employees, and how they are applied to gross wages

The Federal Insurance Contributions Act (FICA) tax rates are a critical component of payroll taxes in the United States. As of the current tax year, the FICA tax rate for employers stands at 6.2% for Social Security and 1.45% for Medicare, totaling 7.65%. Employees pay a slightly lower rate of 6.2% for Social Security and 1.45% for Medicare, amounting to 7.65% as well. These rates are applied to the gross wages of employees, which include all forms of compensation such as salaries, wages, tips, and bonuses.

The application of FICA taxes on gross wages is a straightforward process. Employers are responsible for withholding the employee's share of FICA taxes from their wages and also contributing the employer's share. This is typically done through payroll deductions, where the calculated FICA tax amounts are subtracted from the employee's gross pay. Employers must then remit these taxes to the Internal Revenue Service (IRS) on a regular basis, usually quarterly.

One important aspect to note is the wage base limit for Social Security taxes. For the current tax year, the wage base limit is set at $147,000. This means that Social Security taxes are only applied to wages up to this limit. Any wages earned above this threshold are not subject to Social Security taxes, although they are still subject to Medicare taxes.

Understanding FICA tax rates and their application is crucial for both employers and employees. Employers must ensure they are accurately calculating and remitting FICA taxes to avoid penalties and legal issues. Employees, on the other hand, should be aware of how much FICA tax is being withheld from their wages and how it impacts their overall compensation.

In summary, the current FICA tax rates for both employers and employees are 7.65%, with 6.2% allocated for Social Security and 1.45% for Medicare. These taxes are applied to gross wages, and employers are responsible for withholding and remitting the appropriate amounts to the IRS. The wage base limit for Social Security taxes is an important consideration, as it caps the amount of wages subject to Social Security taxation.

Navigating Tax Withholding: What Companies Need to Know

You may want to see also

Explore related products

![]()

FICA Tax Exemptions: Exploring exemptions and exceptions to FICA taxes, such as certain types of income or specific employee groups

Certain types of income are exempt from FICA taxes, which can significantly impact how employers calculate and withhold these taxes from employee wages. For instance, income earned by students working at their university, certain types of scholarships, and some forms of clergy income may be exempt from FICA taxes. Employers must be aware of these exemptions to ensure they are not over-withholding taxes from their employees.

In addition to income-based exemptions, there are also specific employee groups that may be exempt from FICA taxes. For example, certain government employees, such as those working for state or local governments, may be exempt from FICA taxes if they are covered by a state or local retirement system. Similarly, some foreign workers on certain visa types may be exempt from FICA taxes for a limited period.

Employers must carefully review the tax code and consult with tax professionals to ensure they are correctly identifying and applying FICA tax exemptions. Failure to do so can result in penalties and fines from the IRS. It is also important for employers to communicate with their employees about any applicable exemptions, as this can impact the employees' take-home pay and tax liability.

When it comes to calculating FICA taxes, employers must first determine the employee's gross wages, which includes all forms of compensation, such as salary, tips, and bonuses. However, certain types of compensation, such as employer contributions to retirement plans or health insurance premiums, may be exempt from FICA taxes. Employers must then apply the appropriate FICA tax rates to the employee's gross wages, taking into account any applicable exemptions or exceptions.

In conclusion, understanding FICA tax exemptions is crucial for employers to ensure they are accurately calculating and withholding taxes from their employees' wages. By staying informed about the latest tax laws and regulations, employers can avoid costly mistakes and ensure their employees are not over-taxed.

Maximizing Tax Benefits: Can Employee Salaries Be Written Off?

You may want to see also

Frequently asked questions

Yes, employers are required by law to withhold FICA taxes from their employees' gross wages.

The current FICA tax rate for employers is 6.2% for Social Security and 1.45% for Medicare, totaling 7.65% of the employee's gross wages.

There are certain exceptions to FICA tax withholding requirements, such as for employees who are exempt from Social Security and Medicare taxes due to their religious beliefs or for certain types of non-cash compensation. However, these exceptions are limited and specific, and employers should consult with a tax professional to determine if they apply.