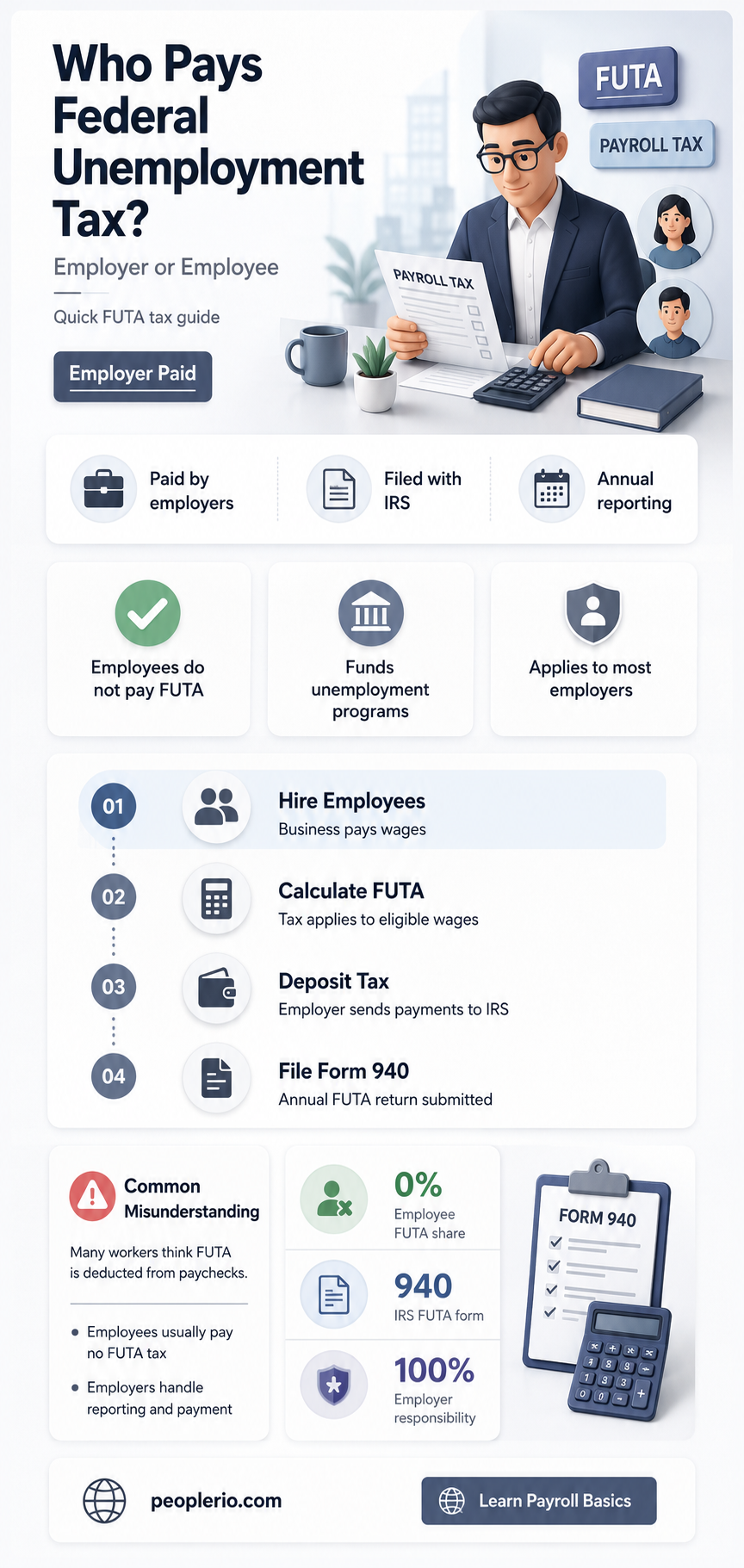

Federal unemployment tax, also known as FUTA, is a payroll tax imposed by the federal government on employers to fund unemployment insurance programs. Generally, this tax is paid solely by employers and is not deducted from an employee's wages. However, in certain circumstances, such as when an employer fails to pay the required FUTA taxes, the Internal Revenue Service (IRS) may hold employees liable for the unpaid taxes. This can lead to a situation where employees are required to pay back the FUTA taxes that their employer failed to remit. It's important for employees to understand their rights and responsibilities regarding FUTA taxes and to be aware of the potential consequences if their employer does not comply with federal tax laws.

| Characteristics | Values |

|---|---|

| Tax Type | Federal Unemployment Tax |

| Taxpayer | Employer |

| Payment Responsibility | Employer |

| Employee Contribution | None |

| Tax Rate | 6% on the first $7,000 of each employee's wages |

| Wage Base | $7,000 per employee |

| Filing Frequency | Quarterly |

| Filing Deadline | End of the quarter following the payment of wages |

| Payment Method | Electronic Federal Tax Payment System (EFTPS) or check |

| Reporting Requirements | Form 940 (Employer's Annual Federal Unemployment Tax Return) |

| Recordkeeping | Maintain records of wages paid and tax withheld for at least 4 years |

| Penalties | Late payment and late filing penalties apply |

| Interest | Interest accrues on late payments |

| Refund | Overpayments can be refunded upon request |

| Amendments | Changes to tax rates or wage bases are updated annually |

| Compliance | Regular audits may be conducted to ensure compliance |

| Additional Requirements | State unemployment tax may also be required |

Explore related products

$8.95 $8.95

What You'll Learn

- Definition of Federal Unemployment Tax: Explanation of what federal unemployment tax is and its purpose

- Employer vs. Employee Responsibility: Clarification on who is responsible for paying federal unemployment tax

- Tax Rate and Calculation: Information on the current tax rate and how it's calculated

- Payment Methods: Description of the different methods available for employers to pay federal unemployment tax

- Consequences of Non-Payment: Details on the penalties and consequences for employers who fail to pay federal unemployment tax

![]()

Definition of Federal Unemployment Tax: Explanation of what federal unemployment tax is and its purpose

Federal unemployment tax is a payroll tax imposed by the federal government on employers to fund unemployment insurance programs. This tax is a crucial component of the social safety net, providing financial support to workers who have lost their jobs through no fault of their own. The tax rate and wage base for federal unemployment tax are set by the Federal Unemployment Tax Act (FUTA).

The purpose of federal unemployment tax is to ensure that workers who are unemployed have access to temporary financial assistance while they search for new employment. This assistance is designed to help workers maintain their standard of living and avoid financial hardship during periods of unemployment. The tax also helps to stabilize the economy by providing a source of funding for unemployment insurance programs, which can help to mitigate the negative impacts of job losses on consumer spending and economic growth.

Federal unemployment tax is typically paid by employers, not employees. Employers are required to pay the tax on the wages they pay to their employees, up to a certain wage base. The tax rate and wage base are subject to change, but as of 2023, the federal unemployment tax rate is 6% on the first $7,000 of wages paid to each employee per year. Employers are required to file annual returns with the Internal Revenue Service (IRS) to report their unemployment tax liability and make payments.

In some cases, employers may be eligible for credits against their federal unemployment tax liability. These credits are typically available to employers who pay state unemployment taxes and have a lower-than-average unemployment insurance claim rate. The credits are designed to incentivize employers to maintain stable employment practices and reduce the number of unemployment claims filed against them.

Federal unemployment tax is an important component of the overall payroll tax system in the United States. It plays a critical role in funding unemployment insurance programs, which provide essential financial support to workers who have lost their jobs. By understanding the definition and purpose of federal unemployment tax, employers and employees can better appreciate the importance of this tax and its role in maintaining economic stability and supporting workers during periods of unemployment.

Understanding Medicare Employee Additional Tax: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Employer vs. Employee Responsibility: Clarification on who is responsible for paying federal unemployment tax

The responsibility for paying federal unemployment tax falls squarely on the shoulders of employers. This tax, which is part of the Federal Unemployment Tax Act (FUTA), is designed to fund state unemployment insurance programs and provide a safety net for workers who lose their jobs. Employers are required to pay this tax on a quarterly basis, and it is calculated as a percentage of the first $7,000 of each employee's wages.

Employees, on the other hand, do not contribute to FUTA. Their role in the unemployment insurance system is limited to receiving benefits if they become unemployed, provided they meet certain eligibility criteria. This distinction is important, as it ensures that the financial burden of maintaining the unemployment insurance system is distributed fairly and that workers are not penalized for job loss.

One common misconception is that employees can opt to pay FUTA themselves, either through payroll deductions or direct payments to the IRS. However, this is not the case. The law explicitly states that FUTA is an employer tax, and there are no provisions for employee contributions. Employers who fail to pay FUTA may face penalties and interest, and employees who are improperly classified as independent contractors may also be liable for unpaid taxes.

In some cases, employers may attempt to shift the cost of FUTA to employees by reducing their wages or benefits. This practice is generally illegal and can result in penalties for the employer. Employees who suspect that their employer is not paying FUTA or is retaliating against them for reporting non-compliance should contact the IRS or their state's unemployment insurance agency for assistance.

In conclusion, the responsibility for paying federal unemployment tax lies with employers, not employees. This system is designed to protect workers and ensure that they have access to unemployment benefits if they lose their jobs. Employers who fail to comply with FUTA requirements may face legal consequences, and employees should be aware of their rights and responsibilities under the law.

Exploring the Tax Benefits of Group Life Insurance Premiums for Employees

You may want to see also

Explore related products

$7.99

![]()

Tax Rate and Calculation: Information on the current tax rate and how it's calculated

The federal unemployment tax rate is a critical component in understanding how unemployment taxes are calculated and who bears the responsibility of payment. Currently, the federal unemployment tax rate stands at 6%, which is applied to the first $7,000 of an employee's wages. This rate is subject to change based on economic conditions and legislative decisions.

The calculation of federal unemployment tax involves multiplying the employee's wages by the tax rate, up to the wage base limit. For example, if an employee earns $5,000 in a year, the federal unemployment tax would be calculated as $5,000 x 6% = $300. However, if the employee earns $8,000, the tax would only be calculated on the first $7,000, resulting in $7,000 x 6% = $420.

It's important to note that the federal unemployment tax is typically paid by employers, not employees. Employers are responsible for withholding the tax from their employees' wages and remitting it to the federal government. In some cases, employees may be required to pay the tax if their employer fails to do so, but this is generally not the norm.

The federal unemployment tax rate and calculation method are designed to provide a safety net for workers who lose their jobs through no fault of their own. The tax funds the federal unemployment insurance program, which provides temporary financial assistance to unemployed workers while they search for new employment.

In summary, the federal unemployment tax rate is currently 6%, and it is applied to the first $7,000 of an employee's wages. The tax is calculated by multiplying the wages by the tax rate, and it is typically paid by employers rather than employees. This tax plays a crucial role in funding the federal unemployment insurance program, which supports workers during periods of unemployment.

Decoding Employee Federal Tax Withholdings: A Business Expense?

You may want to see also

Explore related products

![]()

Payment Methods: Description of the different methods available for employers to pay federal unemployment tax

Employers have several options when it comes to paying federal unemployment tax. One common method is through the Electronic Federal Tax Payment System (EFTPS), which allows for secure online payments. To use EFTPS, employers must enroll in the system and schedule their tax payments in advance. This method is efficient and reduces the risk of late payments or penalties.

Another option is to pay by check or money order, which can be mailed to the IRS along with Form 940, the Employer's Quarterly Federal Unemployment Tax Return. Employers should ensure that their payment is postmarked by the due date to avoid penalties. It's important to note that paying by check may take longer to process compared to electronic payments.

Employers can also choose to pay their federal unemployment tax through a payroll service provider. These providers often handle all aspects of payroll processing, including tax payments, which can save employers time and effort. However, it's crucial to ensure that the payroll provider is reputable and has a good track record of making timely and accurate tax payments.

In some cases, employers may be eligible to pay their federal unemployment tax annually instead of quarterly. This option is available to employers who have consistently paid their taxes on time and have a good compliance history with the IRS. Annual payment can simplify the tax payment process and reduce the administrative burden on employers.

Regardless of the payment method chosen, it's essential for employers to keep accurate records of their tax payments. This includes maintaining copies of payment receipts, bank statements, and any correspondence with the IRS. Proper record-keeping can help employers avoid penalties and interest charges in case of an audit or payment discrepancy.

In conclusion, employers have multiple options for paying federal unemployment tax, including electronic payments through EFTPS, mailing checks or money orders, using payroll service providers, and in some cases, making annual payments. Each method has its own advantages and considerations, and employers should choose the option that best suits their needs and ensures timely and accurate tax payments.

Navigating Mid-Year Tax Withholding Changes: A Guide for Employees

You may want to see also

Explore related products

![]()

Consequences of Non-Payment: Details on the penalties and consequences for employers who fail to pay federal unemployment tax

Employers who fail to pay federal unemployment tax can face severe penalties and consequences. The Internal Revenue Service (IRS) imposes a penalty of 0.5% per month on the unpaid tax amount, up to a maximum of 25%. Additionally, interest accrues on the unpaid tax and penalties, further increasing the amount owed. If the employer continues to neglect their tax obligations, the IRS may take more drastic measures, such as seizing assets or placing a lien on the business.

In addition to financial penalties, employers who fail to pay federal unemployment tax may also face legal consequences. The IRS may pursue criminal charges against the employer, which can result in fines and even imprisonment. Furthermore, the employer may be held liable for any unemployment benefits paid out to employees, as well as any additional administrative costs incurred by the government.

The consequences of non-payment can also extend to the employer's reputation and relationships with employees. A business that fails to pay federal unemployment tax may be viewed as irresponsible or untrustworthy, potentially damaging its reputation in the community. Employees may also lose trust in their employer, leading to decreased morale and productivity.

To avoid these penalties and consequences, employers should ensure that they are paying their federal unemployment tax on time and in full. This can be done by setting up a payment plan with the IRS or by making estimated tax payments throughout the year. Employers should also keep accurate records of their tax payments and any correspondence with the IRS to avoid any potential disputes or misunderstandings.

In conclusion, the consequences of non-payment of federal unemployment tax can be severe and far-reaching. Employers should take their tax obligations seriously and make every effort to pay their taxes on time and in full to avoid these penalties and protect their business and reputation.

Understanding FUTA Taxes: What's Withheld from Your Paycheck?

You may want to see also

Frequently asked questions

No, federal unemployment tax (FUTA) is typically paid by employers, not employees. It is a payroll tax that funds the federal unemployment insurance program.

The federal unemployment tax funds the federal unemployment insurance program, which provides temporary financial assistance to workers who have lost their jobs through no fault of their own.

The FUTA tax rate is 6.0% on the first $7,000 of wages paid to each employee during a calendar year. However, employers may be eligible for a credit of up to 5.4% if they pay state unemployment taxes.

In general, employees do not pay federal unemployment tax. However, in some cases, such as when an employer misclassifies an employee as an independent contractor, the employee may be responsible for paying the tax.

Federal unemployment tax is paid by employers to fund the federal unemployment insurance program, while state unemployment taxes are paid by both employers and employees to fund state unemployment insurance programs. The rates and wage bases for state unemployment taxes vary by state.