If you've recently received a payroll check, you might be eager to cash it and access your hard-earned money. However, you may have noticed that there's a stipulation on the check stating that it can't be cashed until after a certain time or date. This restriction is typically put in place by the employer or the bank to ensure that the funds are available in the account before the check is cashed. It's important to understand the reasons behind this policy and what your options are if you need to cash the check earlier.

Explore related products

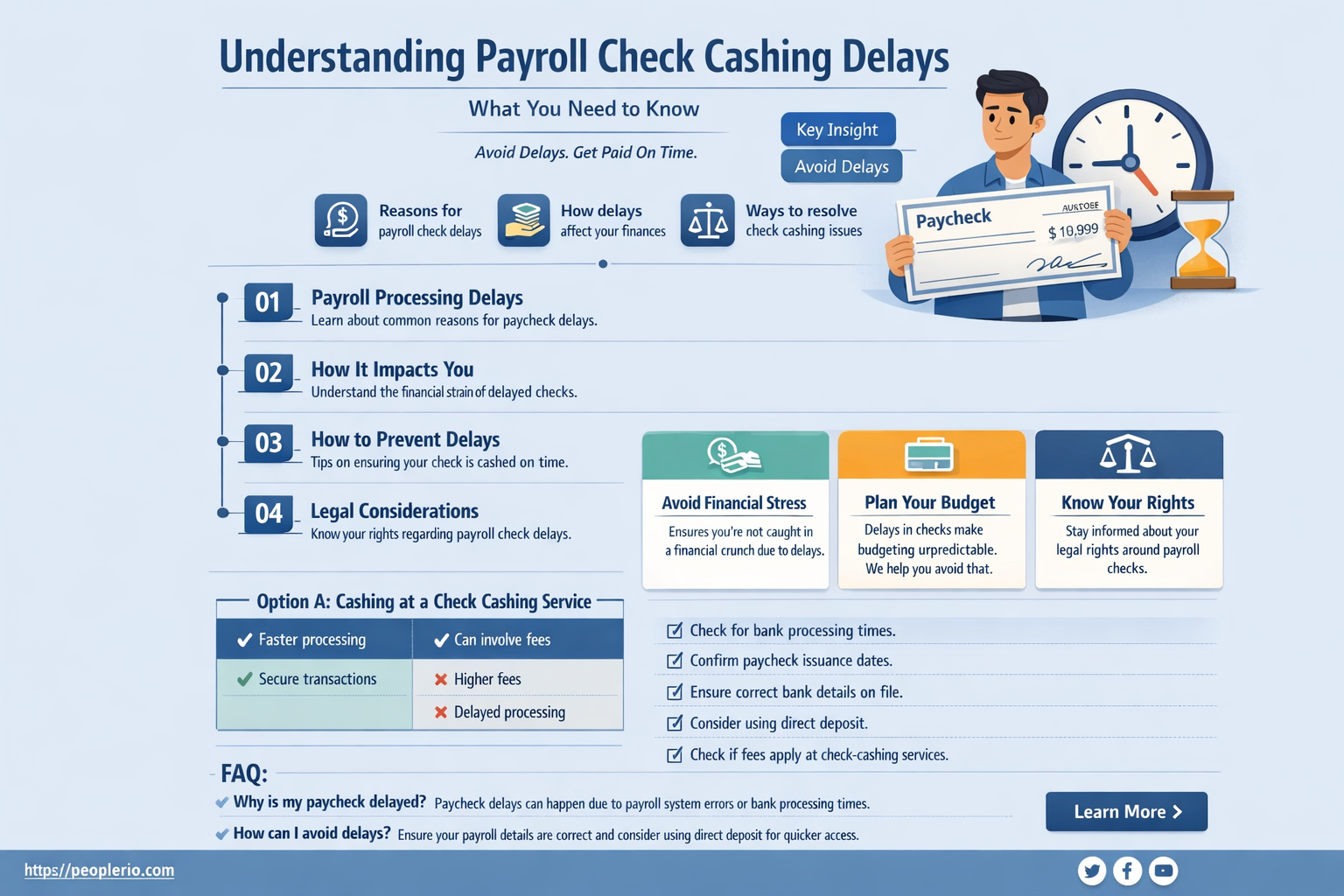

What You'll Learn

- Reasons for Check Holds: Banks may place holds on payroll checks to verify funds or due to suspicious activity

- Check Clearing Process: Understand how checks are processed and cleared by banks, affecting availability of funds

- Employee Communication: Inform employees about check hold policies to manage expectations and avoid confusion

- Alternative Payment Methods: Consider offering direct deposit or other electronic payment options to bypass check holds

- Legal and Regulatory Compliance: Ensure payroll practices comply with banking regulations and employment laws regarding check issuance

![]()

Reasons for Check Holds: Banks may place holds on payroll checks to verify funds or due to suspicious activity

Banks may place holds on payroll checks for several reasons, primarily to ensure the security and integrity of the financial transaction. One common reason is to verify the availability of funds in the employer's account. This is a standard procedure to prevent overdrafts and ensure that the check can be cashed without any issues. The bank may also place a hold if there is any suspicious activity detected, such as an unusual pattern of transactions or if the check details do not match the employer's usual payroll practices. This is done to protect both the bank and the account holder from potential fraud.

Another reason for a check hold could be related to the employee's account status. If the employee's account is new or has a history of overdrafts or bounced checks, the bank may place a hold to mitigate risk. Additionally, if the check is being deposited into an account that is not the primary account associated with the employee's payroll, the bank may place a hold to verify the legitimacy of the transaction.

It's also important to note that banks have different policies and procedures when it comes to check holds. Some banks may have more stringent criteria for placing holds, while others may be more lenient. The duration of the hold can also vary depending on the bank's policies and the reason for the hold. Typically, holds are placed for a few business days, but in some cases, they can last longer if additional verification is required.

To avoid check holds, employers can ensure that they have sufficient funds in their account before issuing payroll checks. They can also work with their bank to establish a payroll processing system that minimizes the risk of fraud and errors. Employees can also take steps to avoid check holds by maintaining a good account standing and depositing checks into their primary account.

In conclusion, check holds are a common practice in the banking industry to ensure the security and integrity of payroll transactions. While they can be inconvenient, they are necessary to protect both the bank and the account holder from potential fraud and financial losses. By understanding the reasons for check holds and taking steps to minimize risk, employers and employees can help ensure a smooth and efficient payroll process.

Efficient Payroll Check Deposits: A Guide to Electronic Banking

You may want to see also

Explore related products

![]()

Check Clearing Process: Understand how checks are processed and cleared by banks, affecting availability of funds

The check clearing process is a critical aspect of banking operations that determines when funds from a deposited check become available for withdrawal. This process involves several steps, starting from the moment a check is deposited into an account. Initially, the bank verifies the check's authenticity, ensuring that the signature is valid and the check is not fraudulent. This verification step is crucial as it prevents the bank from processing a check that could potentially lead to financial losses.

Once the check is verified, the bank then contacts the drawee bank, which is the bank from which the funds will be drawn. This communication is typically done electronically through a network that facilitates the exchange of check information and funds. The drawee bank then confirms whether the account holder has sufficient funds to cover the check amount. If the funds are available, the drawee bank will transfer the money to the depositing bank.

However, the availability of funds for withdrawal is not immediate. Banks often place a hold on the funds for a certain period, known as the clearing time. This hold is in place to ensure that the check does not bounce due to insufficient funds or other issues. The clearing time can vary depending on the bank's policies and the type of check deposited. For instance, payroll checks may have a shorter clearing time compared to personal checks due to their regular and predictable nature.

During the clearing period, the depositor may not be able to access the full amount of the check. This can be inconvenient, especially if the depositor needs the funds urgently. To mitigate this, some banks offer services that allow for immediate access to a portion of the check amount, with the remaining balance becoming available once the check is fully cleared.

Understanding the check clearing process is essential for managing finances effectively. It helps individuals and businesses plan their cash flow and avoid potential overdrafts or bounced checks. By knowing when funds will be available, depositors can make informed decisions about when to withdraw or transfer money, ensuring that they have sufficient funds to meet their financial obligations.

Exploring Payroll Check Usage: Can You Make Purchases?

You may want to see also

Explore related products

![]()

Employee Communication: Inform employees about check hold policies to manage expectations and avoid confusion

To effectively manage employee expectations and prevent confusion regarding check hold policies, it is crucial to establish clear and transparent communication channels. This involves proactively informing employees about the specific timeframes within which they can expect their payroll checks to be available for cashing. By doing so, you can mitigate potential misunderstandings and ensure that employees are well-informed about the policies in place.

One approach to achieving this is by conducting regular training sessions or workshops to educate employees about the check hold policies. These sessions can be used to explain the reasons behind the policies, the expected waiting periods, and any exceptions that may apply. Additionally, providing employees with written documentation, such as an employee handbook or a dedicated section on the company intranet, can serve as a valuable reference point for employees to access information at their convenience.

Another effective strategy is to leverage technology to streamline communication. For instance, implementing a payroll management system that sends automated notifications to employees about the status of their checks can help keep them informed in real-time. This can be particularly beneficial for employees who may not have easy access to traditional communication channels or who prefer digital interactions.

Furthermore, it is essential to address any concerns or questions that employees may have about the check hold policies. Encouraging open dialogue and providing prompt responses to employee inquiries can help build trust and foster a positive work environment. This can be facilitated through regular town hall meetings, anonymous feedback mechanisms, or one-on-one discussions with HR representatives.

In conclusion, effective employee communication is key to managing expectations and avoiding confusion regarding check hold policies. By implementing a combination of training sessions, written documentation, technological solutions, and open dialogue, organizations can ensure that their employees are well-informed and equipped to navigate the payroll process with ease.

Can Handwritten Payroll Checks Be Tracked by the IRS?

You may want to see also

Explore related products

![]()

Alternative Payment Methods: Consider offering direct deposit or other electronic payment options to bypass check holds

Direct deposit has become an increasingly popular alternative to traditional paper checks, and for good reason. By offering direct deposit, employers can bypass the check hold process entirely, allowing employees to access their funds more quickly and conveniently. This method also reduces the risk of lost or stolen checks, and can save both employers and employees money on check cashing fees. To implement direct deposit, employers will need to work with their payroll provider and bank to set up the necessary systems and processes.

Another electronic payment option to consider is prepaid debit cards. These cards can be loaded with an employee's wages and used like a regular debit card, without the need for a bank account. This can be a particularly useful option for employees who do not have access to traditional banking services. Prepaid debit cards can also help employers reduce the administrative burden of managing paper checks, and can provide employees with the convenience of being able to use their card at any ATM or retail location.

Mobile payment apps, such as Venmo or Zelle, are another alternative payment method that can be used to bypass check holds. These apps allow employers to send payments directly to an employee's mobile device, which can then be transferred to a bank account or used to make purchases. This method can be particularly useful for gig workers or contractors who may not have access to traditional payroll systems.

When considering alternative payment methods, it is important for employers to weigh the benefits and drawbacks of each option. Factors to consider include the cost of implementation, the convenience for employees, and the security of the payment method. Employers should also be aware of any legal or regulatory requirements that may apply to different payment methods.

In conclusion, alternative payment methods such as direct deposit, prepaid debit cards, and mobile payment apps can provide a convenient and efficient way for employers to bypass check holds and provide employees with quicker access to their wages. By carefully considering the options and implementing the best solution for their business, employers can improve employee satisfaction and reduce the administrative burden of managing paper checks.

Exploring Mobile Deposit Options for Payroll Checks: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Legal and Regulatory Compliance: Ensure payroll practices comply with banking regulations and employment laws regarding check issuance

To ensure legal and regulatory compliance in payroll practices, it is crucial to understand the banking regulations and employment laws that govern check issuance. This includes adhering to guidelines set by financial regulatory bodies such as the Federal Reserve in the United States, which mandates that banks must make funds from deposited checks available within a specific timeframe. Employers must also comply with state and federal laws regarding minimum wage, overtime pay, and tax withholdings, all of which can impact the timing and amount of payroll checks.

One key aspect of compliance is verifying the identity and employment status of workers before issuing payroll checks. This involves maintaining accurate records of employee information, including social security numbers, addresses, and dates of employment. Employers should also implement secure processes for distributing payroll checks, such as using tamper-evident envelopes or requiring photo identification for check pickup.

Another important consideration is the timing of payroll check issuance. Employers must ensure that checks are issued on a regular schedule and that employees are informed of any changes to this schedule. Additionally, employers should be aware of laws that require prompt payment of wages, such as California's requirement that wages be paid within 15 days of the end of the pay period.

To avoid legal issues, employers should also be cautious about deductions from payroll checks. While certain deductions, such as taxes and social security, are mandatory, others, such as garnishments and child support payments, require specific legal procedures. Employers must ensure that all deductions are authorized and comply with applicable laws and regulations.

Finally, employers should stay informed about changes to banking regulations and employment laws that may impact payroll practices. This includes monitoring updates from regulatory bodies and consulting with legal and financial advisors as needed. By staying proactive and informed, employers can ensure that their payroll practices remain compliant and avoid costly legal penalties.

Unlocking Payroll Funds: How Soon Can You Access Your Money?

You may want to see also

Frequently asked questions

Payroll checks often have a specified date after which they can be cashed. This is to ensure that the funds are available in the employer's account and to prevent fraudulent activities.

If you attempt to cash your check before the designated time, it may be returned unpaid by the bank. This could result in fees for both you and your employer, and may affect your future paychecks.

Your employer should provide you with information about when your check will be available for cashing. This may be communicated through a pay stub, email, or other notification methods.

Yes, some employers offer direct deposit options, which allow your paycheck to be automatically deposited into your bank account on the designated pay date. This eliminates the need to wait for a physical check to clear.