Banks are generally required to cash payroll checks as part of their financial services. This is because payroll checks are typically issued by employers to their employees as a means of payment for work performed. As such, banks have an obligation to honor these checks and provide the necessary funds to the account holder. However, there may be certain conditions or limitations that apply, such as the need for proper identification or the verification of the check's authenticity. Additionally, some banks may have specific policies or fees associated with cashing payroll checks, so it's important for individuals to be aware of these details when conducting their banking transactions.

Explore related products

What You'll Learn

- Legal Requirements: Banks must cash payroll checks under certain conditions, ensuring compliance with labor and banking laws

- Verification Process: Banks verify payroll checks to prevent fraud, confirming the employer's account and payment details

- Fees and Policies: Some banks charge fees for cashing payroll checks or have specific policies regarding large transactions

- Benefits for Employers: Offering payroll checks can benefit employers by reducing electronic payment costs and increasing employee satisfaction

- Employee Rights: Employees have the right to receive their wages in a timely and accessible manner, including through payroll checks

![]()

Legal Requirements: Banks must cash payroll checks under certain conditions, ensuring compliance with labor and banking laws

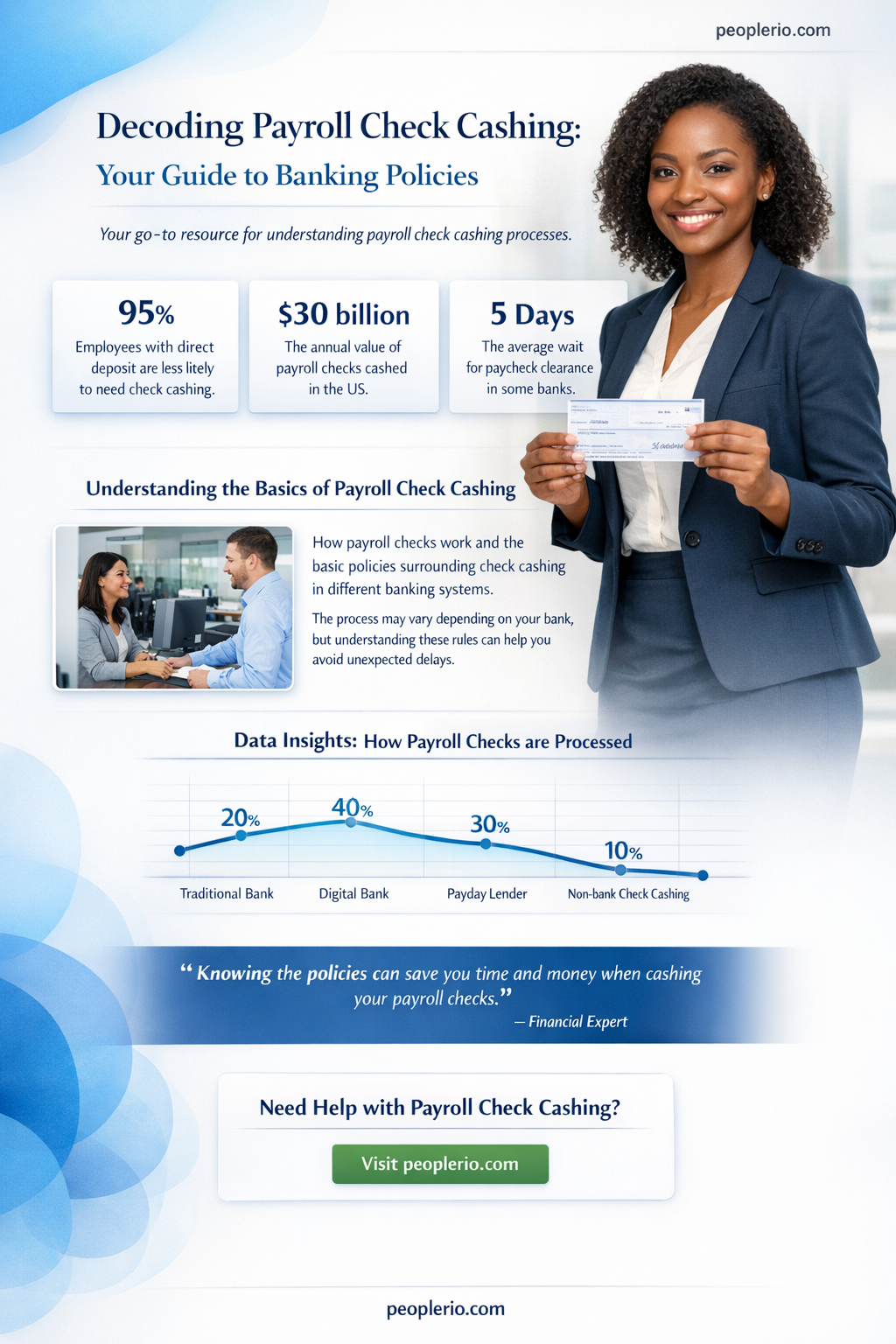

Banks are legally obligated to cash payroll checks under specific conditions to ensure compliance with both labor and banking laws. This requirement is rooted in the understanding that employees have a right to receive their wages in a timely and accessible manner. According to the Fair Labor Standards Act (FLSA), employers must pay their employees at least twice a month, and banks play a crucial role in facilitating this process.

One of the key conditions under which banks must cash payroll checks is the verification of the check's authenticity. This involves confirming that the check is drawn from a valid account with sufficient funds and that the signature on the check matches the authorized signatory for the account. Banks are also required to ensure that the check is not post-dated, as this could potentially lead to fraudulent activities.

In addition to verifying the check's authenticity, banks must also comply with the Bank Secrecy Act (BSA) and the USA PATRIOT Act. These laws require banks to maintain records of all transactions, including payroll checks, and to report any suspicious activities to the appropriate authorities. This helps to prevent money laundering and other financial crimes.

Another important condition is that banks must cash payroll checks without charging any fees to the employee. This is to ensure that employees receive their full wages without any deductions. Banks are allowed to charge fees to the employer for processing payroll checks, but these fees cannot be passed on to the employee.

Finally, banks must also comply with state laws regarding the cashing of payroll checks. Some states have specific requirements, such as the need for a government-issued ID or the limitation on the amount of cash that can be given out. Banks must be aware of these state-specific regulations to ensure compliance.

In conclusion, banks play a vital role in ensuring that employees receive their wages in a timely and accessible manner. By complying with federal and state laws, banks help to maintain the integrity of the payroll system and protect the rights of employees.

Navigating Financial Independence: Can I Cash My Husband's Payroll Check?

You may want to see also

Explore related products

![]()

Verification Process: Banks verify payroll checks to prevent fraud, confirming the employer's account and payment details

Banks employ a meticulous verification process to prevent fraud when it comes to cashing payroll checks. This process involves confirming the employer's account and payment details to ensure the check's legitimacy. The verification typically includes checking the routing number, account number, and the amount of the check against the employer's account records.

The first step in the verification process is to validate the employer's account information. This is done by comparing the routing and account numbers on the check with the bank's records. If the numbers match, the bank proceeds to the next step. If they don't, the check is likely fraudulent, and the bank will not cash it.

Next, the bank verifies the payment details. This involves checking the amount of the check against the employer's account balance. If the employer has sufficient funds to cover the check, the bank will proceed with cashing it. However, if the account balance is insufficient or if there are any discrepancies in the payment details, the bank may flag the check for further review or reject it outright.

In addition to these steps, banks may also use other fraud prevention measures, such as checking the check for watermarks, security features, and signatures. They may also compare the check to previous checks issued by the employer to identify any inconsistencies.

The verification process is crucial in preventing payroll check fraud, which can result in significant financial losses for both the employer and the bank. By confirming the employer's account and payment details, banks can ensure that they are only cashing legitimate checks and protecting their customers from potential fraud.

Streamline Your Finances: How to Deduct Rent from Your Payroll Check

You may want to see also

Explore related products

![]()

Fees and Policies: Some banks charge fees for cashing payroll checks or have specific policies regarding large transactions

Banks often have varying policies and fee structures when it comes to cashing payroll checks, which can significantly impact the accessibility and cost of this service for individuals. While some banks may offer free check cashing services to their customers, others may impose fees, particularly for non-customers or for checks above a certain amount. These fees can range from a flat rate to a percentage of the check amount, and they may be capped or tiered based on the size of the transaction.

In addition to fees, banks may also have specific policies regarding large transactions. For instance, some banks may require additional identification or documentation for checks above a certain threshold, such as $10,000. Others may have limits on the amount of cash that can be withdrawn in a single transaction or per day. These policies are typically in place to prevent fraud and ensure compliance with anti-money laundering regulations.

Individuals who frequently cash payroll checks should be aware of these fees and policies to avoid unexpected costs or complications. It may be beneficial to shop around for a bank that offers favorable terms for check cashing, particularly if one's employer does not offer direct deposit options. Additionally, understanding a bank's policies regarding large transactions can help individuals plan accordingly and avoid any potential issues when cashing sizable checks.

Employers also play a role in this ecosystem, as they may choose to use banks that offer competitive check cashing services for their employees. By doing so, they can help reduce the financial burden on their workers and improve overall satisfaction. Furthermore, employers may consider offering direct deposit options, which can eliminate the need for physical checks and the associated fees and policies.

In conclusion, while banks are generally required to cash payroll checks, their fees and policies can vary widely. It is essential for both individuals and employers to be informed about these aspects to make the most cost-effective and convenient choices for their financial transactions. By understanding the landscape of check cashing services, one can navigate the system more effectively and avoid unnecessary expenses or hassles.

Decoding Payroll Check Cashing: Your Ultimate Guide to Time Limits

You may want to see also

Explore related products

![]()

Benefits for Employers: Offering payroll checks can benefit employers by reducing electronic payment costs and increasing employee satisfaction

Offering payroll checks can indeed provide several benefits to employers. One of the primary advantages is the reduction in electronic payment costs. Employers who opt for direct deposit or other electronic payment methods often incur fees associated with processing and maintaining these systems. By offering payroll checks, employers can potentially lower these expenses, as the cost of printing and distributing checks can be more cost-effective, especially for smaller businesses.

Another significant benefit is the potential increase in employee satisfaction. Some employees prefer receiving physical checks, as it provides them with a tangible record of their earnings and allows them to manage their finances in a way that suits them best. This can be particularly important for employees who do not have easy access to banking services or who prefer to avoid electronic transactions for personal reasons.

Furthermore, offering payroll checks can also help employers attract and retain talent. In a competitive job market, providing flexible payment options can be a valuable perk that sets a company apart from its competitors. Employees who value the ability to receive their pay in a format that aligns with their personal preferences may be more likely to choose and remain with an employer that offers this option.

It is also worth noting that payroll checks can serve as a useful tool for financial education and literacy. Employers can use the opportunity to provide employees with information about budgeting, saving, and managing their finances effectively. This can help employees make the most of their earnings and improve their overall financial well-being.

In conclusion, offering payroll checks can benefit employers in several ways, from reducing electronic payment costs to increasing employee satisfaction and retention. By providing this option, employers can demonstrate their commitment to meeting the diverse needs of their workforce and fostering a positive work environment.

Handwriting Payroll Checks: A Guide for Small Business Owners

You may want to see also

Explore related products

![]()

Employee Rights: Employees have the right to receive their wages in a timely and accessible manner, including through payroll checks

Employees have a fundamental right to receive their wages in a timely and accessible manner, which includes the issuance of payroll checks. This right is enshrined in various labor laws and regulations, ensuring that workers are compensated fairly and promptly for their labor. Payroll checks serve as a tangible representation of an employee's earnings, providing a clear and transparent record of their wages.

In the context of banking practices, the question arises as to whether banks are obligated to cash payroll checks. While banks are not legally required to cash every check presented to them, they do have a responsibility to honor checks drawn on their own accounts. This means that if an employer maintains a payroll account with a particular bank, that bank is generally expected to cash payroll checks issued from that account.

However, banks may impose certain conditions or restrictions on the cashing of payroll checks. For instance, they may require the check to be presented within a specific timeframe, or they may place limits on the amount that can be cashed in a single transaction. Additionally, banks may charge fees for cashing payroll checks, particularly if the check is drawn on an account with insufficient funds or if the check is returned unpaid.

Employees should be aware of their rights and the banking practices that affect the cashing of their payroll checks. By understanding these practices, employees can better navigate the process of receiving their wages and ensure that they are able to access their funds in a timely and convenient manner. Employers, too, have a responsibility to ensure that their payroll practices comply with legal requirements and that their employees are able to receive their wages without undue delay or inconvenience.

In conclusion, while banks are not universally obligated to cash payroll checks, they do have a responsibility to honor checks drawn on their own accounts. Employees have a right to receive their wages in a timely and accessible manner, and understanding banking practices can help them exercise this right effectively. Employers must also ensure that their payroll practices comply with legal requirements and facilitate the prompt and convenient receipt of wages by their employees.

Can Your Payroll Check Be Cancelled? Understanding Your Rights and Options

You may want to see also

Frequently asked questions

Generally, banks are not legally required to cash payroll checks. However, they may have policies in place to honor certain types of checks, including payroll checks, as a service to their customers.

Factors that might influence a bank's decision to cash a payroll check include the bank's policies, the customer's account history, the size of the check, and the bank's relationship with the employer issuing the check.

Yes, banks can charge a fee for cashing payroll checks. The fee amount may vary depending on the bank's policies and the size of the check.

If a bank refuses to cash a payroll check, alternatives may include depositing the check into the customer's account, using a check cashing service, or contacting the employer to arrange for a different payment method.