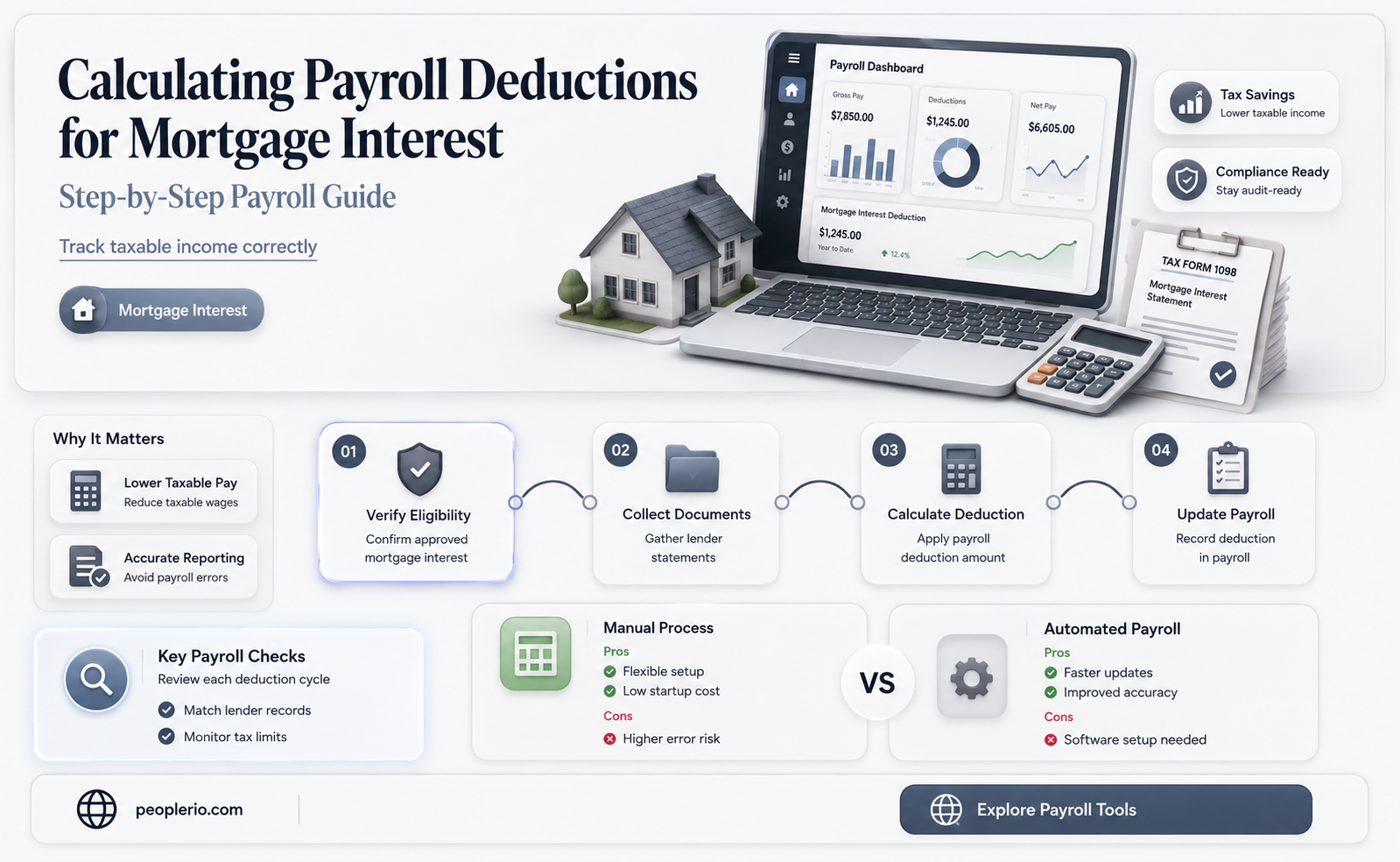

Calculating payroll deductions for mortgage interest involves understanding the specific guidelines and regulations set by tax authorities. Generally, mortgage interest deductions are claimed on tax returns rather than taken directly from payroll. However, some employers may offer a flexible spending account (FSA) or other tax-saving programs that allow employees to set aside pre-tax dollars for mortgage interest expenses. To accurately determine the deduction amount, one must consider factors such as the total mortgage interest paid annually, applicable tax rates, and any limits imposed by tax laws. Consulting with a tax professional or using online tax calculators can help ensure accurate and compliant deductions.

| Characteristics | Values |

|---|---|

| Deduction Type | Payroll deduction for mortgage interest |

| Purpose | To reduce taxable income by the amount paid towards mortgage interest |

| Eligibility | Available to taxpayers who itemize deductions and have a mortgage on a qualified residence |

| Qualified Residence | Primary residence or second home, not rental properties or vacation homes |

| Deduction Limit | No specific limit, but must be for interest paid during the tax year |

| Documentation Required | Mortgage interest statement (Form 1098) from the lender |

| Calculation Method | Total mortgage interest paid during the year, as reported on Form 1098 |

| Tax Form | Reported on Schedule A of Form 1040 |

| Impact on Tax Liability | Reduces adjusted gross income, potentially lowering tax liability |

| Carryover | Unused deductions cannot be carried over to future tax years |

| Interaction with Other Deductions | Must itemize deductions to claim mortgage interest; cannot claim both itemized and standard deductions |

| Changes in Tax Law | Subject to changes in tax legislation; consult current IRS guidelines |

| Record Keeping | Maintain records of mortgage payments and interest statements for at least three years |

| Common Mistakes | Failing to itemize deductions, not keeping proper records, claiming interest on non-qualified residences |

| Professional Advice | Recommended to consult a tax professional for complex situations or changes in tax law |

Explore related products

What You'll Learn

- Gather necessary information: Collect employee's mortgage interest deduction details, including interest paid and property type

- Determine deduction limits: Check the maximum allowable deduction per tax laws and regulations

- Calculate the deduction: Use the provided information to compute the mortgage interest deduction amount

- Fill out the payroll deduction form: Complete the required paperwork to set up the payroll deduction

- Submit the form: Send the completed form to the payroll department for processing the deduction

![]()

Gather necessary information: Collect employee's mortgage interest deduction details, including interest paid and property type

To accurately calculate payroll deductions for mortgage interest, it's crucial to gather all necessary information from employees. This includes details such as the total interest paid on the mortgage and the type of property the mortgage is for. Collecting this information ensures that the deductions are calculated correctly and in compliance with tax regulations.

The first step in gathering this information is to request that employees provide their mortgage interest deduction details in writing. This can be done through a formal request or by distributing a form specifically designed for this purpose. The form should clearly outline the information required, such as the employee's name, social security number, mortgage lender's name, and the address of the property.

Once the information has been collected, it's important to verify its accuracy. This can be done by cross-referencing the information provided by the employee with their pay stubs or other relevant documents. It's also a good idea to have a system in place for regularly updating and reviewing the information to ensure that it remains accurate and up-to-date.

In addition to collecting information from employees, it's also important to stay informed about any changes to tax laws or regulations that may affect mortgage interest deductions. This can be done by regularly reviewing updates from the IRS or consulting with a tax professional. By staying informed, you can ensure that your payroll deductions are calculated correctly and in compliance with the latest regulations.

Finally, it's important to maintain clear and detailed records of all mortgage interest deductions. This includes keeping track of the amount deducted from each employee's paycheck, as well as any changes or updates to the deduction amounts. Maintaining accurate records not only helps with compliance but also makes it easier to troubleshoot any issues that may arise in the future.

Calculating Average Monthly Payroll for PPP Second Draw: A Guide

You may want to see also

Explore related products

![]()

Determine deduction limits: Check the maximum allowable deduction per tax laws and regulations

To determine deduction limits for mortgage interest from payroll deductions, it's essential to consult the latest tax laws and regulations. These limits can vary based on several factors, including the taxpayer's income, filing status, and the amount of mortgage interest paid during the tax year. For instance, the IRS may impose a limit on the total amount of mortgage interest that can be deducted, or it may restrict deductions based on the percentage of the taxpayer's adjusted gross income.

One practical approach is to review the IRS's Publication 936, which provides detailed information on the home mortgage interest deduction. This publication outlines the types of interest that can be deducted, the requirements for the deduction, and the limits on the deduction amount. Additionally, taxpayers can use the IRS's interactive tools and calculators to estimate their potential deductions and ensure they are within the allowable limits.

Another important consideration is the impact of state tax laws, which may have different rules and limits for mortgage interest deductions. Taxpayers should consult their state's tax authority or a tax professional to understand how state laws may affect their deductions. Furthermore, it's crucial to keep accurate records of mortgage interest payments, as these will be necessary to substantiate the deductions claimed on the tax return.

In summary, determining deduction limits for mortgage interest from payroll deductions requires a thorough understanding of federal and state tax laws, as well as careful record-keeping. By consulting the appropriate resources and seeking professional advice when needed, taxpayers can ensure they are maximizing their deductions while staying within the legal limits.

Efficient Payroll Management: Calculating Average Employees per Cycle

You may want to see also

Explore related products

![]()

Calculate the deduction: Use the provided information to compute the mortgage interest deduction amount

To calculate the mortgage interest deduction amount, you'll need to gather specific information from your mortgage statement and tax documents. First, locate the total amount of interest paid on your mortgage for the tax year. This figure is typically found on Form 1098, which your mortgage lender will send you at the beginning of the year. Next, determine your adjusted gross income (AGI) from your tax return. The AGI is a crucial factor in calculating the deduction amount, as it affects the phase-out limits for the mortgage interest deduction.

Once you have the total interest paid and your AGI, you can begin the calculation process. If your AGI is below the phase-out threshold, you can deduct the full amount of mortgage interest paid. However, if your AGI exceeds the threshold, you'll need to calculate the deduction amount using a specific formula. This formula takes into account the excess AGI above the threshold and the applicable phase-out percentage.

For example, let's say you paid $10,000 in mortgage interest for the tax year, and your AGI is $150,000. If the phase-out threshold is $100,000, you would calculate the deduction amount as follows: First, determine the excess AGI above the threshold, which is $50,000 ($150,000 - $100,000). Next, apply the phase-out percentage to the excess AGI. If the phase-out percentage is 10%, you would multiply $50,000 by 0.10, resulting in a phase-out amount of $5,000. Finally, subtract the phase-out amount from the total interest paid to arrive at the deduction amount: $10,000 - $5,000 = $5,000.

It's essential to note that the phase-out thresholds and percentages can vary depending on your tax filing status and the tax year. Therefore, it's crucial to consult the latest tax laws and regulations to ensure accurate calculations. Additionally, consider using tax software or consulting a tax professional to help navigate the complexities of the mortgage interest deduction and ensure you're maximizing your tax savings.

Mastering Payroll in Arizona: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Fill out the payroll deduction form: Complete the required paperwork to set up the payroll deduction

To set up payroll deductions for mortgage interest, you'll need to fill out the appropriate form provided by your employer or payroll department. This form will typically require you to provide your personal information, such as your name, address, and Social Security number. You'll also need to include details about your mortgage, including the lender's name, your account number, and the amount you wish to deduct from each paycheck.

Before filling out the form, it's essential to determine the correct amount to deduct. This will depend on your mortgage interest rate, the principal balance of your loan, and the frequency of your paychecks. You can use an online mortgage interest deduction calculator to help you determine the appropriate amount. Be sure to double-check your calculations to avoid over- or under-deducting.

Once you've completed the form, you'll need to submit it to your employer or payroll department. They will then process the deduction and forward the funds to your mortgage lender. It's important to note that the processing time may vary depending on your employer's payroll schedule and the lender's requirements.

To ensure a smooth process, it's a good idea to follow up with your employer and lender to confirm that the deductions are being made correctly and on time. You should also keep a copy of the completed form for your records, as you may need to refer to it in the future if there are any changes to your mortgage or payroll deductions.

Remember, setting up payroll deductions for mortgage interest can be a convenient way to make your mortgage payments on time and potentially save on interest costs. However, it's crucial to carefully complete the required paperwork and monitor the deduction process to avoid any errors or delays.

PPP Payroll Calculation: A Step-by-Step Guide for Employers

You may want to see also

Explore related products

![TurboTax Deluxe Desktop Edition 2025, Federal & State Tax Return [Win11/Mac14 Download]](https://m.media-amazon.com/images/I/71OcM906MLL._AC_UY218_.jpg)

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UY218_.jpg)

![]()

Submit the form: Send the completed form to the payroll department for processing the deduction

Once you have meticulously filled out the payroll deduction form for your mortgage interest, the next crucial step is to submit it to the payroll department for processing. This involves ensuring that the form is complete, with all necessary fields filled out accurately and legibly. Double-check that you have included all required supporting documents, such as proof of mortgage interest payments, to avoid any delays in processing.

The submission process typically involves either mailing the form to the payroll department or submitting it electronically through an online portal. If mailing, make sure to use a secure and trackable method to ensure that the form is received by the appropriate department. If submitting electronically, follow the instructions provided by your employer to ensure that the form is uploaded correctly and securely.

After submitting the form, it is important to follow up with the payroll department to confirm receipt and processing. This can help to identify any potential issues or errors early on, allowing for prompt resolution. Be prepared to provide any additional information or documentation that may be requested by the payroll department to facilitate the processing of your deduction.

It is also advisable to keep a copy of the submitted form and any supporting documents for your own records. This can be helpful in case of any discrepancies or issues that may arise during the processing of your deduction. By maintaining accurate records, you can ensure that you are able to track the progress of your deduction and address any potential problems efficiently.

In conclusion, submitting the completed form to the payroll department for processing the deduction is a critical step in ensuring that your mortgage interest payments are accurately deducted from your payroll. By following the proper submission procedures and maintaining accurate records, you can help to facilitate a smooth and efficient processing of your deduction.

Mastering Hourly Payroll Calculations: A Step-by-Step Guide for Employers

You may want to see also

Frequently asked questions

The first step is to determine the total mortgage interest paid during the tax year. This information is typically provided by the lender on a Form 1098.

To be eligible for mortgage interest deductions, you must itemize your deductions on Schedule A of your tax return. Additionally, the mortgage must be secured by your primary residence or a second home, and you must have paid the interest during the tax year.

The maximum amount of mortgage interest you can deduct is limited to the interest paid on the first $750,000 of the mortgage ($375,000 if married filing separately).

If you're not the primary borrower but are legally responsible for the mortgage and pay the interest, you may be able to deduct it. However, you should consult with a tax professional to ensure you meet all the necessary criteria.

To calculate the payroll deduction amount, you'll need to estimate your total mortgage interest paid for the year and divide it by the number of pay periods. This will give you the amount to be deducted from each paycheck. You can use IRS Form W-4 to adjust your withholding accordingly.

![TurboTax Premier Desktop Edition 2025, Federal & State Tax Return [Win11/Mac14 Download]](https://m.media-amazon.com/images/I/71ofxs16-9L._AC_UY218_.jpg)

![TurboTax Home & Business Desktop Edition 2025, Federal & State Tax Return [Win11/Mac14 Download]](https://m.media-amazon.com/images/I/71-jbdrZxVL._AC_UY218_.jpg)

![TurboTax Deluxe Desktop Edition 2025, Federal Tax Return [Win11/Mac14 Download]](https://m.media-amazon.com/images/I/71pX8Fh2sNL._AC_UY218_.jpg)

![TurboTax Business Desktop Edition 2025, Federal Tax Return [Win11 Download]](https://m.media-amazon.com/images/I/71iKclcd6ML._AC_UY218_.jpg)

![H&R Block Tax Software Deluxe 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51Mlng5FWYL._AC_UY218_.jpg)

![H&R Block Tax Software Premium 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51dMIAMHkkL._AC_UY218_.jpg)

![H&R Block Tax Software Premium & Business 2025 Win [PC Online code]](https://m.media-amazon.com/images/I/618kxmZlTGL._AC_UY218_.jpg)