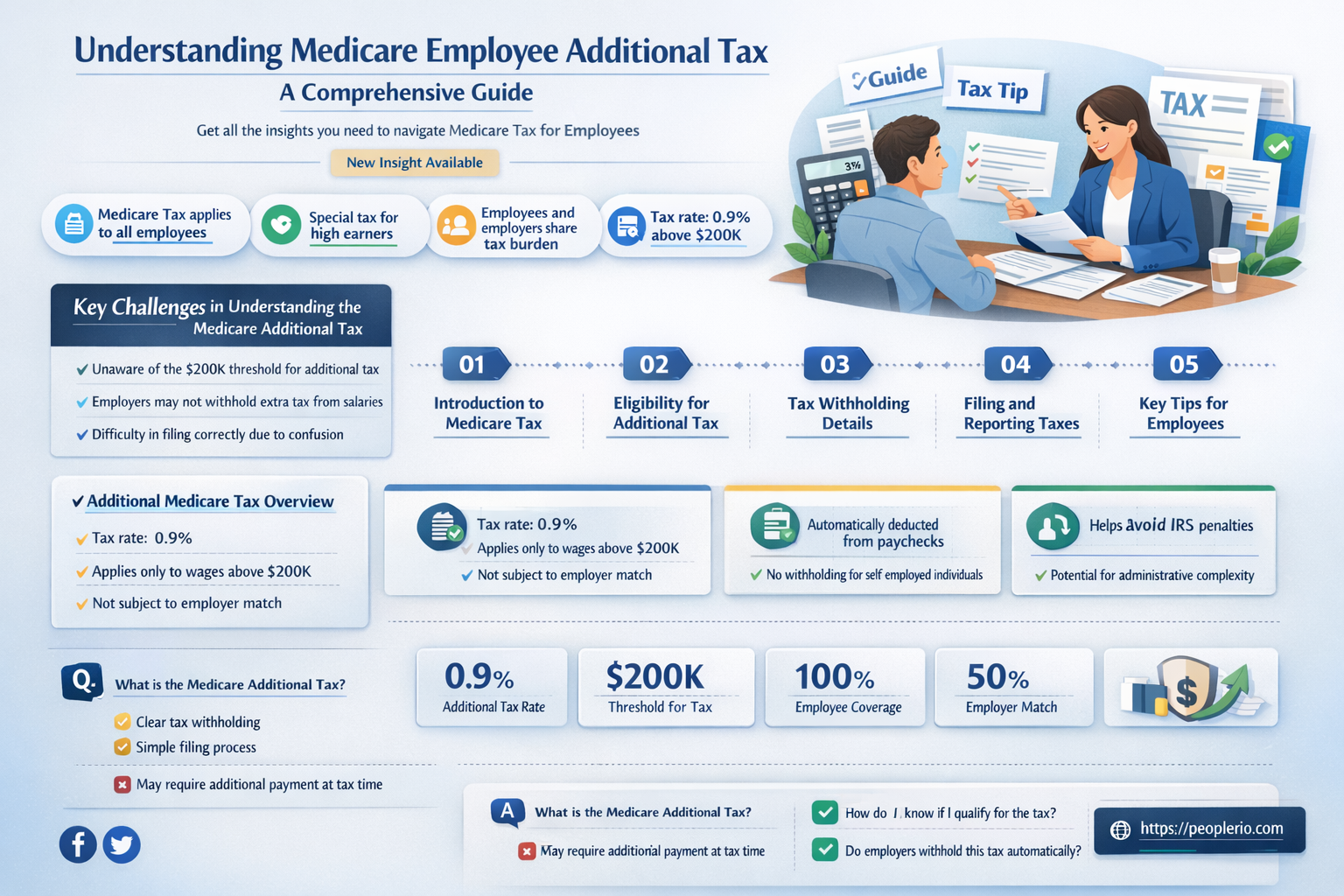

Medicare Employee Additional Tax, often referred to as the Medicare surtax, is a federal tax imposed on higher-income employees in the United States. This tax is designed to help fund Medicare, the federal health insurance program primarily for individuals aged 65 and older, as well as certain younger people with disabilities. The additional tax rate is typically 0.9% of an employee's wages, salaries, and tips that exceed a certain threshold amount. Employers are responsible for withholding this tax from their employees' paychecks and remitting it to the Internal Revenue Service (IRS). Understanding the Medicare Employee Additional Tax is crucial for both employers and employees to ensure compliance with tax laws and to plan for the financial impact it may have on their income.

| Characteristics | Values |

|---|---|

| Tax Type | Additional Medicare Tax |

| Purpose | To fund Medicare services |

| Applicability | Applies to certain high-income earners |

| Tax Rate | Typically 0.9% of wages or self-employment income above a threshold |

| Threshold | $200,000 for individuals, $250,000 for married couples filing jointly |

| Calculation | Tax is withheld from wages or estimated and paid quarterly by self-employed individuals |

| Reporting | Reported on Form 1040, Schedule SE for self-employed individuals |

| Effective Date | January 1, 2013 |

| Legal Reference | Section 1401 of the Affordable Care Act |

Explore related products

What You'll Learn

- Definition: Medicare employee additional tax is a payroll tax that funds Medicare Part A

- Rate: The current tax rate is 1.45% of wages, with an additional 0.9% for high earners

- Wage Base: The tax is applied to all wages, with no cap on the amount subject to taxation

- Employer Responsibility: Employers must withhold the tax from employees' wages and match the amount withheld

- Purpose: The tax helps fund Medicare Part A, which provides hospital insurance for eligible individuals

![]()

Definition: Medicare employee additional tax is a payroll tax that funds Medicare Part A

Medicare employee additional tax, often referred to as the Medicare surtax, is a specific payroll tax that plays a crucial role in funding Medicare Part A. This tax is levied on employees who earn above a certain threshold, which is adjusted annually for inflation. As of the latest data available, the Medicare employee additional tax rate stands at 1.45% for earnings up to $200,000 ($250,000 for married couples filing jointly), and 2.35% for earnings above these thresholds.

The primary purpose of this tax is to ensure the solvency of Medicare Part A, which covers hospital services, skilled nursing facilities, and some home health care. By targeting higher-income earners, the tax aims to distribute the financial burden of Medicare more equitably across different income groups. It's important to note that this tax is separate from the regular Medicare tax that all employees pay, which is currently set at 6.2% of earnings.

Employers are responsible for withholding the Medicare employee additional tax from their employees' wages and submitting it to the IRS. However, employees who are self-employed or have multiple jobs may need to calculate and pay this tax themselves if their combined earnings exceed the threshold. Failure to pay this tax can result in penalties and interest charges from the IRS.

One unique aspect of the Medicare employee additional tax is that it is not subject to the Social Security wage base limit, which means that there is no cap on the amount of earnings that can be taxed. This is in contrast to the regular Medicare tax, which is only applied to earnings up to the Social Security wage base limit.

In summary, the Medicare employee additional tax is a critical component of the Medicare funding system, designed to ensure that higher-income earners contribute more towards the cost of Medicare Part A. Understanding this tax is essential for both employees and employers to comply with tax laws and avoid potential penalties.

Decoding Employee Tax Rates: A Comprehensive Guide for 2023

You may want to see also

Explore related products

![]()

Rate: The current tax rate is 1.45% of wages, with an additional 0.9% for high earners

The Medicare employee additional tax is a crucial component of the U.S. healthcare system, specifically designed to fund Medicare, the federal health insurance program primarily for individuals aged 65 and older. The current tax rate stands at 1.45% of an employee's wages. This rate is applied uniformly across all wage levels, ensuring a broad base of contributors to the Medicare system.

For high earners, defined as individuals with wages exceeding $200,000 annually ($250,000 for married couples filing jointly), an additional tax rate of 0.9% is imposed. This supplementary rate is applied only to the portion of wages that surpass the aforementioned thresholds, thereby targeting higher-income individuals with a slightly higher tax burden. The rationale behind this tiered approach is to distribute the financial responsibility of supporting Medicare more equitably across different income levels.

The implementation of these tax rates is straightforward. Employers are responsible for withholding the Medicare tax from their employees' paychecks and remitting the funds to the Internal Revenue Service (IRS). Employees do not need to take any specific actions regarding this tax, as it is automatically deducted from their wages. However, it is essential for employees to be aware of these tax rates and how they impact their take-home pay, especially for those in higher income brackets.

One notable aspect of the Medicare employee additional tax is its role in addressing the long-term financial sustainability of the Medicare program. As healthcare costs continue to rise and the population ages, ensuring a stable and sufficient funding source is critical. The additional tax rate for high earners is a measure aimed at bolstering Medicare's financial reserves, helping to guarantee that the program remains viable for future generations.

In conclusion, the Medicare employee additional tax, with its current rates of 1.45% for all wages and an extra 0.9% for high earners, plays a vital role in supporting the Medicare program. This tax is an integral part of the U.S. healthcare system, contributing to the financial stability and sustainability of Medicare. Understanding these tax rates and their implications is important for employees and employers alike, as they directly impact wage calculations and overall financial planning.

Understanding the Tax Implications of Non-Employee Compensation

You may want to see also

Explore related products

![]()

Wage Base: The tax is applied to all wages, with no cap on the amount subject to taxation

The Medicare Employee Additional Tax is a crucial component of the U.S. healthcare system, specifically designed to fund Medicare, the federal health insurance program primarily for individuals aged 65 and older. One key aspect of this tax is its wage base, which refers to the total amount of an employee's wages that are subject to taxation. Unlike some other taxes that may have caps or limits on the amount of income taxed, the Medicare Employee Additional Tax is applied to all wages, with no cap on the amount subject to taxation. This means that every dollar earned by an employee is taxed at the applicable rate, currently 1.45% for most workers.

This unlimited wage base ensures a steady and substantial stream of revenue for the Medicare program, which is essential for covering the healthcare costs of millions of beneficiaries. It also reflects the principle of progressive taxation, where higher-income individuals contribute a larger share of their earnings to support public services. For employees, understanding this aspect of the tax is important for accurate tax planning and withholding, as well as for appreciating the role they play in supporting the nation's healthcare infrastructure.

Employers also play a critical role in the administration of the Medicare Employee Additional Tax. They are responsible for withholding the tax from their employees' wages and submitting the collected funds to the Internal Revenue Service (IRS). This involves accurate record-keeping and timely reporting to ensure compliance with tax laws and regulations. Employers must also be aware of any changes to the tax rate or wage base that may occur due to legislative updates or economic adjustments.

In addition to the basic tax rate, there is an additional 0.9% tax on wages above a certain threshold for higher-income workers. This supplemental tax was introduced as part of the Affordable Care Act (ACA) to help fund healthcare reforms and expand coverage to more Americans. The threshold for this additional tax is $200,000 for individuals and $250,000 for married couples filing jointly. This tiered approach to taxation ensures that the burden is distributed more equitably across different income levels.

Overall, the wage base for the Medicare Employee Additional Tax is a fundamental element of the U.S. tax system, providing essential funding for the Medicare program while also promoting fairness and equity in taxation. By understanding this aspect of the tax, both employees and employers can better navigate their tax obligations and contribute to the sustainability of the nation's healthcare system.

Are Employee Pension Contributions Tax Deductible? A Comprehensive Guide

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/61ilSrOeMoL._AC_UY218_.jpg)

![]()

Employer Responsibility: Employers must withhold the tax from employees' wages and match the amount withheld

Employers play a crucial role in the Medicare system by being responsible for withholding the Medicare employee additional tax from their workers' wages. This tax, also known as the Medicare surtax, is an additional 0.9% tax on wages and compensation that exceeds certain thresholds. The responsibility of employers extends beyond mere withholding; they are also required to match the amount withheld, effectively doubling the tax impact on high-income employees.

The Medicare employee additional tax applies to individuals with wages and compensation above $200,000 ($250,000 for married couples filing jointly). Employers must carefully monitor their employees' earnings to ensure accurate withholding once the threshold is surpassed. This involves implementing robust payroll systems and staying updated on any changes to Medicare tax regulations.

Failure to withhold and match the Medicare surtax can result in penalties and interest for employers. Therefore, it is essential for businesses to maintain meticulous records and consult with tax professionals to ensure compliance. Employers should also communicate with their employees about the Medicare surtax, providing transparency regarding the additional tax withholding and its implications.

In summary, employer responsibility for the Medicare employee additional tax is multifaceted, encompassing accurate withholding, matching contributions, and maintaining compliance with regulatory requirements. By fulfilling these obligations, employers contribute to the sustainability of the Medicare program while also promoting transparency and trust with their employees.

Tax-Free Employee Gifts: What Employers Need to Know

You may want to see also

Explore related products

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/61wrmwXah3L._AC_UL320_.jpg)

![]()

Purpose: The tax helps fund Medicare Part A, which provides hospital insurance for eligible individuals

The Medicare Employee Additional Tax serves a critical purpose in the funding of Medicare Part A, which is essential for providing hospital insurance to eligible individuals. This tax is a key component of the financial structure that supports the Medicare program, ensuring that it can continue to offer vital healthcare services to millions of Americans.

One of the primary reasons for the implementation of this tax is to address the growing financial demands of the Medicare program. As the population ages and healthcare costs continue to rise, it has become increasingly important to find sustainable ways to fund Medicare. The additional tax on employees is designed to help bridge the gap between the program's revenue and its expenditures, ensuring that Medicare Part A remains solvent and able to provide the necessary hospital insurance coverage.

The tax is calculated as a percentage of an employee's wages and is typically withheld from their paycheck. This means that employees contribute directly to the funding of Medicare Part A through their payroll taxes. The rate of the Medicare Employee Additional Tax can vary depending on certain factors, such as the employee's income level and the specific provisions of the Medicare program in place at the time.

It is important to note that the Medicare Employee Additional Tax is not a new concept. It has been a part of the Medicare program for several decades, and its purpose has remained consistent throughout that time. The tax has helped to ensure that Medicare Part A has the necessary funds to provide hospital insurance coverage to eligible individuals, including seniors, certain younger people with disabilities, and people with End-Stage Renal Disease (ESRD).

In conclusion, the Medicare Employee Additional Tax plays a vital role in the financial stability of the Medicare program. By contributing to the funding of Medicare Part A, this tax helps to ensure that eligible individuals have access to essential hospital insurance coverage. As the healthcare landscape continues to evolve, it is likely that the importance of this tax will only continue to grow, making it a crucial component of the Medicare program's future.

Maximize Your Take-Home Pay: Tax Reduction Strategies for W2 Employees

You may want to see also

Frequently asked questions

The Medicare Employee Additional Tax is an extra tax withheld from the wages of certain employees to fund Medicare. It applies to employees who earn above a specific threshold.

Employees who earn more than $200,000 per year ($250,000 for married couples filing jointly) are subject to the Medicare Employee Additional Tax.

The tax rate for the Medicare Employee Additional Tax is 0.9% of the employee's wages that exceed the threshold amount.