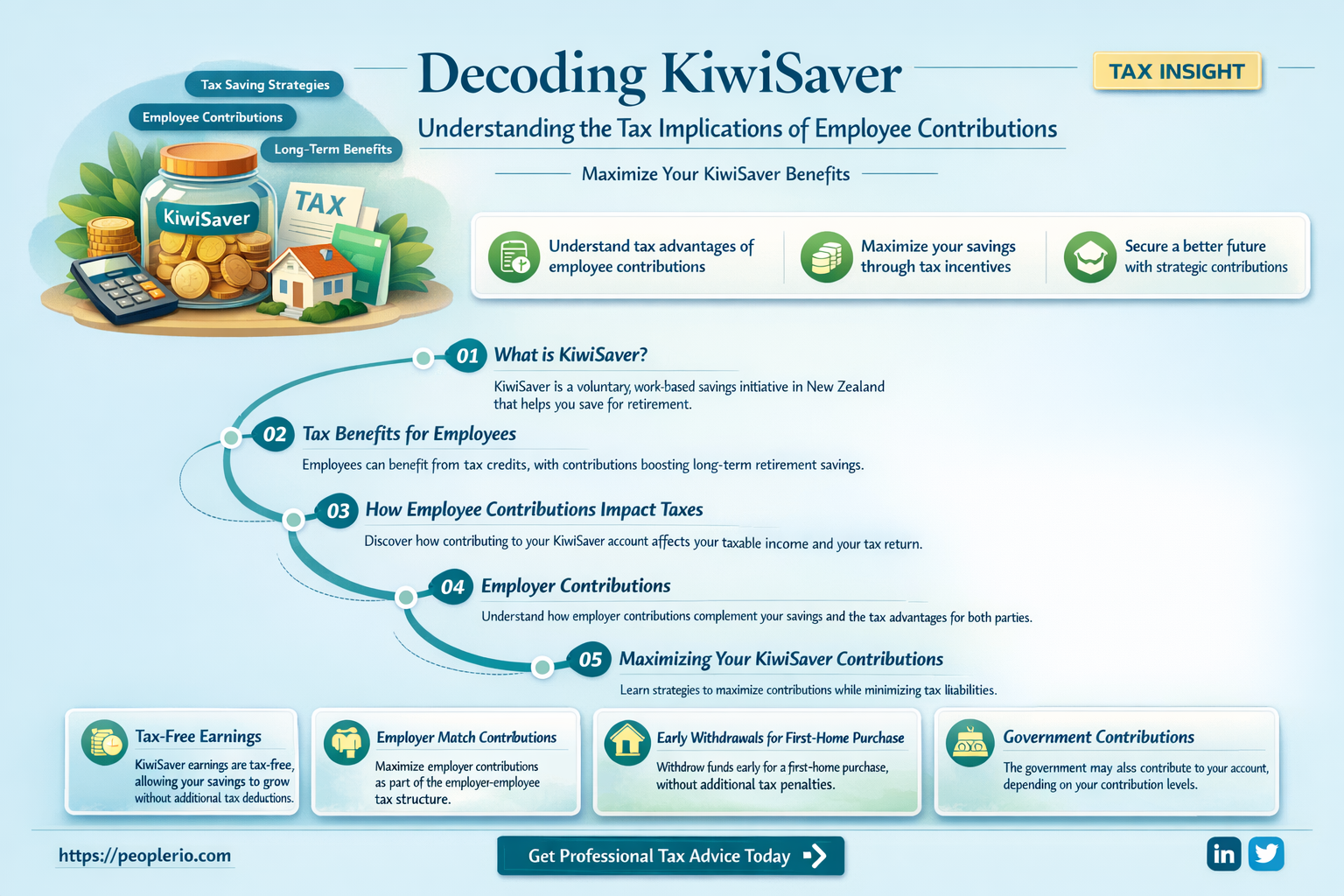

Employee contributions to KiwiSaver are indeed subject to tax. However, the tax treatment is quite favorable, designed to encourage retirement savings. Contributions are taxed at the employee's marginal tax rate, but the government also makes a contribution to the employee's KiwiSaver account, known as the Member Tax Credit. This credit is 50 cents for every dollar contributed by the employee, up to a maximum of $521.43 per year. Additionally, investment earnings within the KiwiSaver account are taxed at a concessional rate of 17.5%, which is lower than the marginal tax rates for most individuals. This combination of tax incentives helps to maximize the growth of retirement savings over time.

| Characteristics | Values |

|---|---|

| Contribution Type | Employee contributions to KiwiSaver |

| Taxation Status | Taxed |

| Tax Rate | Contributions are taxed at the employee's marginal tax rate |

| Tax Deduction | Tax is deducted at source by the employer |

| Net Contribution | The net amount after tax is credited to the employee's KiwiSaver account |

| Employer Contributions | Employers are required to contribute a minimum of 3% of the employee's gross salary |

| Total Contribution Cap | There is a cap on the total contributions an employee can make to KiwiSaver each year |

| Investment Returns | Investment returns on contributions are generally taxed at a lower rate (15%) |

| Withdrawal Rules | Withdrawals from KiwiSaver are taxed as income in the year of withdrawal |

| Exceptions | Certain exceptions apply, such as for first-time home buyers or in cases of financial hardship |

Explore related products

What You'll Learn

- Taxation Basics: Understanding how KiwiSaver contributions are taxed and the implications for employees

- Contribution Limits: Exploring the annual contribution limits and how they affect taxation

- Tax Credits: Discussing the tax credits available for KiwiSaver contributions and how they're applied

- Withdrawal Rules: Outlining the rules for withdrawing KiwiSaver funds and the tax implications

- Investment Returns: Examining how investment returns within KiwiSaver are taxed and reported

![]()

Taxation Basics: Understanding how KiwiSaver contributions are taxed and the implications for employees

KiwiSaver contributions are subject to tax, but the specifics can be complex. Employers are required to deduct tax from employee contributions at the employee's marginal tax rate. This means that the tax rate applied to your KiwiSaver contributions will depend on your total income for the year. For example, if you earn less than $14,000 per year, your KiwiSaver contributions will be taxed at 10.5%. However, if you earn more than $48,000 per year, your contributions will be taxed at 33%.

One important implication of this tax structure is that employees need to be aware of their marginal tax rate and how it affects their KiwiSaver contributions. If you're not sure what your marginal tax rate is, you can use the Inland Revenue Department's (IRD) tax calculator to find out. Additionally, employees should be aware that their KiwiSaver contributions are not tax-deductible, meaning they cannot be used to reduce their taxable income.

Another key aspect of KiwiSaver taxation is the treatment of employer contributions. Employer contributions are not taxed at the time they are made, but they are taxed when the employee withdraws the funds from their KiwiSaver account. This means that employees will need to pay tax on their employer's contributions when they retire or withdraw the funds for another eligible purpose.

It's also important to note that KiwiSaver contributions are not subject to GST. This means that the full amount of your contributions will be invested, without any GST being deducted. Additionally, KiwiSaver funds are not subject to income tax while they are invested, which can help to maximize the growth of your savings over time.

In summary, while KiwiSaver contributions are subject to tax, the specifics can be complex. Employees need to be aware of their marginal tax rate and how it affects their contributions, as well as the treatment of employer contributions and the tax implications of withdrawing funds from their KiwiSaver account. By understanding these basics, employees can make informed decisions about their KiwiSaver contributions and maximize the benefits of this important savings scheme.

Understanding Texas Taxation: Are Andrews Employee Exemptions Taxed?

You may want to see also

Explore related products

$9.99

![]()

Contribution Limits: Exploring the annual contribution limits and how they affect taxation

The annual contribution limits to a KiwiSaver account are a critical factor in determining the tax implications for employees. As of the current tax year, the maximum annual contribution is $52,128.43, which includes both employee and employer contributions. This limit is subject to change, so it's essential to stay informed about any updates.

Exceeding the annual contribution limit can result in additional taxes. The excess contributions are taxed at the employee's marginal tax rate, which can significantly impact the overall tax liability. For example, if an employee contributes $60,000 to their KiwiSaver account in a given year, the excess $7,871.57 will be taxed at their marginal rate. This could potentially push them into a higher tax bracket, further increasing their tax burden.

On the other hand, staying within the contribution limits can provide significant tax benefits. The contributions are deducted from the employee's gross salary, reducing their taxable income. This can lead to a lower tax liability and potentially a tax refund. Additionally, the investment earnings within the KiwiSaver account are taxed at a concessional rate of 15%, which is lower than the marginal tax rates for most individuals.

It's also important to consider the impact of employer contributions on the overall tax situation. Employer contributions are not taxed as income to the employee, but they do count towards the annual contribution limit. This means that employees need to be mindful of their own contributions to avoid exceeding the limit and incurring additional taxes.

In conclusion, understanding the annual contribution limits and their impact on taxation is crucial for employees looking to maximize the benefits of their KiwiSaver accounts. By staying within the limits and taking advantage of the tax deductions and concessional tax rates, employees can minimize their tax liability and grow their retirement savings more effectively.

Understanding Pre-Tax Deductions: A Guide to Employee Benefits

You may want to see also

Explore related products

![]()

Tax Credits: Discussing the tax credits available for KiwiSaver contributions and how they're applied

KiwiSaver contributions are incentivized through tax credits, which are applied directly to the member's account. These tax credits are calculated based on the contributions made by both the employee and their employer. For every dollar contributed by the employee, the government will contribute a tax credit of 50 cents, up to a maximum of $521.43 per year. This means that the more you contribute, the more tax credits you will receive, up to the annual cap.

The tax credits are applied annually, based on the contributions made in the previous year. For example, if you contribute $1,000 in the 2023-2024 financial year, you will receive a tax credit of $500 in the 2024-2025 financial year. It's important to note that the tax credits are not taxable, meaning they do not count towards your taxable income.

To maximize the tax credits, it's advisable to contribute as much as possible to your KiwiSaver account, up to the annual contribution limit. This not only increases the tax credits you receive but also helps you save more for your future. It's also important to ensure that your employer is contributing to your KiwiSaver account, as their contributions will also count towards the tax credits you receive.

In summary, tax credits are a valuable incentive for KiwiSaver contributions, providing a direct boost to your savings. By understanding how they work and maximizing your contributions, you can make the most of this benefit and accelerate your savings growth.

Unleashing Fitness Incentives: The Tax Benefits of Employee Gym Memberships

You may want to see also

Explore related products

![]()

Withdrawal Rules: Outlining the rules for withdrawing KiwiSaver funds and the tax implications

KiwiSaver funds are designed to help New Zealanders save for their retirement, and as such, there are specific rules governing when and how these funds can be withdrawn. Generally, KiwiSaver funds can only be withdrawn after the age of 65, or in the event of significant financial hardship or terminal illness. It's important to note that early withdrawals may incur a penalty, and could also impact an individual's eligibility for certain benefits.

When it comes to the tax implications of withdrawing KiwiSaver funds, it's important to understand that these funds are taxed differently than other forms of income. KiwiSaver funds are taxed at a marginal rate, which means that the tax rate applied to each dollar withdrawn will depend on an individual's total income for the year. Additionally, there is a 15% tax credit applied to all KiwiSaver contributions, which can help to offset the tax liability on withdrawals.

It's also worth noting that KiwiSaver funds can be transferred to an Australian superannuation fund, which may be beneficial for individuals who are planning to retire in Australia. However, it's important to seek professional advice before making any decisions about transferring funds, as there may be additional tax implications and fees involved.

In summary, while KiwiSaver funds are designed to help individuals save for retirement, there are specific rules and tax implications associated with withdrawing these funds. It's important to understand these rules and seek professional advice before making any decisions about withdrawing or transferring KiwiSaver funds.

Understanding Medicare Employee Additional Tax: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Investment Returns: Examining how investment returns within KiwiSaver are taxed and reported

KiwiSaver investment returns are subject to tax, but the specific tax treatment depends on the type of investment and the individual's tax situation. Generally, investment returns are taxed at the individual's marginal tax rate. However, there are some exceptions and nuances to be aware of.

For example, dividends received from shares held within a KiwiSaver account are taxed at the individual's marginal tax rate, but they may also be subject to a 5% withholding tax. This withholding tax is deducted by the company paying the dividend and is credited against the individual's tax liability when they file their tax return.

Interest income from bonds or bank deposits held within a KiwiSaver account is also taxed at the individual's marginal tax rate. However, if the individual is under 18 years old, the first $200 of interest income is tax-free.

Capital gains from the sale of investments held within a KiwiSaver account are generally taxed at the individual's marginal tax rate. However, if the investment was held for more than one year, the capital gain may be eligible for the lower long-term capital gains tax rate of 15%.

It's important to note that the tax treatment of KiwiSaver investment returns can be complex, and individuals should seek advice from a tax professional if they are unsure about their specific situation. Additionally, the tax rules surrounding KiwiSaver are subject to change, so it's important to stay up-to-date with the latest information.

Maximizing Tax Benefits: Employee HSA Contributions Explained

You may want to see also

Frequently asked questions

Yes, employee KiwiSaver contributions are taxed. The tax is deducted at the employee's marginal tax rate before the contribution is made to their KiwiSaver account.

The taxation of KiwiSaver contributions reduces an employee's take-home pay because the tax is deducted from their gross salary before the contribution is made. However, the employee may receive a tax credit from the government to offset some of this tax.

Yes, there are tax benefits for employees who contribute to KiwiSaver. The government provides a tax credit of up to $521.43 per year for eligible employees who contribute to KiwiSaver. This tax credit is paid directly into the employee's KiwiSaver account.

The taxation of KiwiSaver contributions is similar to other retirement savings options, such as superannuation schemes. Contributions to these schemes are also taxed at the employee's marginal tax rate. However, KiwiSaver offers the benefit of government tax credits, which can help to offset the tax paid on contributions.